Research — May 18, 2026

SQM seen posting 58% revenue growth in 2026 as lithium prices rebound

By Sonam Sidana

Sociedad Química y Minera de Chile SA (NYSE: SQM) is poised for significant growth in its first-quarter 2026 earnings, as a rebound in lithium prices lifts profitability after three difficult years for the battery materials sector.

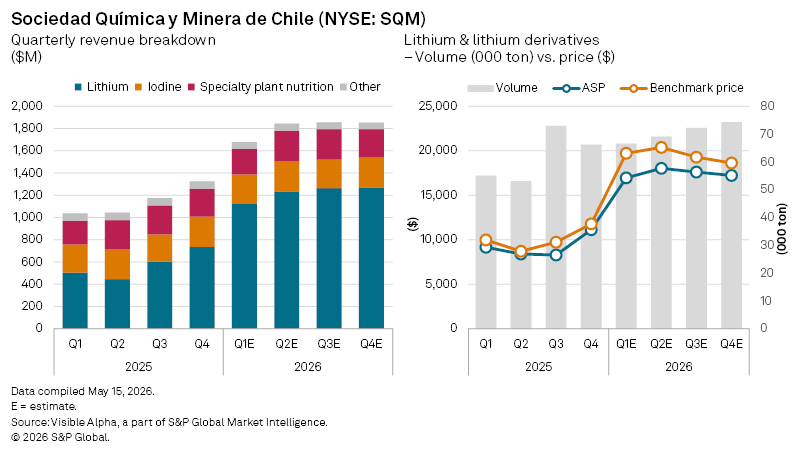

Visible Alpha consensus estimates point to SQM’s Q1 revenue rising 62% year-on-year to $1.7 billion, driven by a recovery in the company’s lithium business, which remains the dominant earnings engine for the Chilean producer. Revenue from lithium and lithium derivatives is forecast to surge 123% to $1.1 billion for the quarter, and account for more than 60% of group sales in fiscal 2026, as improving pricing conditions begin to reverse the steep declines seen across the global lithium market since late 2022. By contrast, SQM’s non-lithium businesses are expected to deliver more muted growth.

The recovery comes as lithium markets stabilize following a prolonged period of oversupply that pressured prices and margins across the industry, affecting producers. Spot lithium carbonate prices have recovered materially in 2026, supported by significant supply deficits, surging demand for EVs, and energy storage.

Analysts expect SQM’s average realized lithium price in Q1 to rise 85% year-on-year to $16,940 per ton, up from $11,125 in the previous quarter and $9,144 a year earlier. Lithium and derivative sales volumes, meanwhile, are expected to increase only modestly sequentially, to 67,000 tons from 66,000 tons in the fourth quarter, and 55,000 tons a year ago, highlighting the improvement in lithium earnings is being driven primarily by price rather than volume.

The sharper pricing environment is expected to feed directly into the bottom line. Analysts forecast first-quarter net income to climb 182% year-on-year to $388 million, while diluted EPS is projected to reach $1.36, reflecting stronger lithium profitability and improved operating leverage as pricing recovers.

The company is scheduled to report Q1 2026 earnings on May 27.

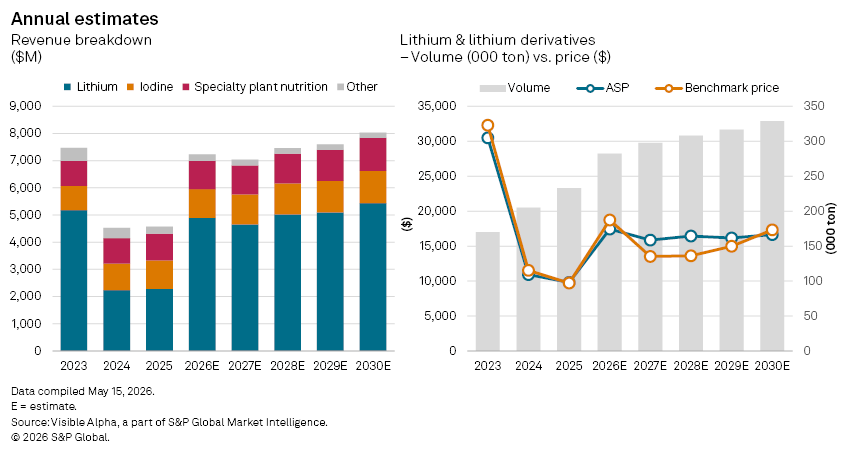

Looking beyond the quarter, analysts expect SQM’s recovery to strengthen through 2026. Consensus estimates forecast full-year revenue rising 58% to $7.3 billion, accelerating sharply from roughly 1% growth last year.

Lithium and lithium derivatives are expected to remain the key growth engine, with segment revenue projected to surge 114% to $4.9 billion. Analysts also expect average realized lithium carbonate equivalent prices to rebound 78% to $17,438 per ton in 2026, reversing last year’s 10% decline.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings