Research — May 28, 2026

Samsung postQ snapshot: Memory drives Q1 beat; outlook raised on AI cycle

By Sunny Rupani

Samsung Electronics Co. Ltd. (KRX: 005930) delivered a strong Q1 2026 print on 30 April, with earnings materially ahead of Visible Alpha consensus expectations across revenue, EPS and operating profit, driven by continued strength in AI-linked memory demand. The results reinforced Samsung’s position as a key beneficiary of hyperscaler-led AI infrastructure investment, even as pockets of weakness persisted in high-bandwidth memory (HBM), displays, and certain consumer-facing segments.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

Revenue of KRW 133.9 trillion came in 5.4% above Visible Alpha consensus expectations, while diluted EPS of KRW 7,056 exceeded expectations by 14%. Operating profit reached KRW 57.2 trillion, beating consensus by 11.3%, with margins expanding to 42.8%, around 262 bps above expectations. The key driver was once again the Device Solutions (DS) division, where revenue of KRW 81.7 trillion beat expectations by 9.5% and surged 225% year-on-year, reflecting the depth of the ongoing memory upcycle.

Within DS, the memory business delivered strong momentum:

- Memory revenue of KRW 74.8 trillion beat consensus by 7.1% and rose 292% YOY

- DRAM revenue of KRW 52.1 trillion rose 313% YOY, beating expectations by 10.1%

- NAND revenue of KRW 22.7 trillion beat by 12.5%, up 220% YOY

- However, HBM revenue (KRW 3.3 trillion) disappointed, coming in 8.6% below expectations.

The Device eXperience (DX) segment delivered revenue of KRW 52.4 trillion, exceeding consensus by 5.3%.

Samsung continued to lean into the AI and semiconductor investment cycle. CapEx of KRW 17.1 trillion exceeded expectations, driven by expansion in advanced memory and semiconductor capacity. R&D spend of KRW 11.3 trillion came in slightly above expectations, focused on AI memory, next-gen nodes, and advanced device architecture.

Guidance

Management did not provide explicit numerical guidance, but commentary reinforced a constructive structural backdrop for AI-driven memory demand through 2026.

Management expects AI-driven memory demand to remain strong through 2026, supported by hyperscaler AI infrastructure buildout and enterprise LLM adoption. HBM4E sample shipments targeted for Q2, while expanding sales in high-value products including DDR5, SOCAMM2, and PCIe Gen6 SSDs.

In Foundry, advanced-node utilization remains high, supported by AI/HPC demand. 1.4nm roadmap remains on track. Second-generation 2nm mobile production expected in 2H 2026.

Within Mobile, management expects Q2 smartphone revenue expected to grow on flagship and A-series demand. Profitability likely to moderate sequentially due to launch cycle normalization and cost pressures.

Lastly, Display conditions expected to remain weak, though focus remains on premium OLED. Harman growth supported by rising automotive electronics volumes.

Importantly, CapEx is expected to increase significantly in FY2026, reinforcing Samsung’s commitment to maintaining technology leadership in AI-linked semiconductor infrastructure.

Management also reiterated its commitment to annual regular dividend payouts of KRW 9.8 trillion through quarterly dividends of approximately KRW 2.5 trillion.

Analyst Q&A highlights

Management commentary during the call added further nuance:

- HBM profitability: conventional DRAM margins remain stronger near term, but management expects the HBM margin gap to narrow in 2027 as AI demand deepens

- Geopolitics: no material supply chain disruption from Middle East tensions, supported by inventory buffers and logistics diversification

- Foundry pipeline: 2nm AI/HPC engagements are progressing, with growing traction in advanced-node AI workloads

- AI adjacency expansion: Management highlighted growing AI opportunities beyond memory, including NAND-based AI storage, data center cooling solutions (post-FlaktGroup acquisition), and early-stage humanoid robotics initiatives as optionality drivers

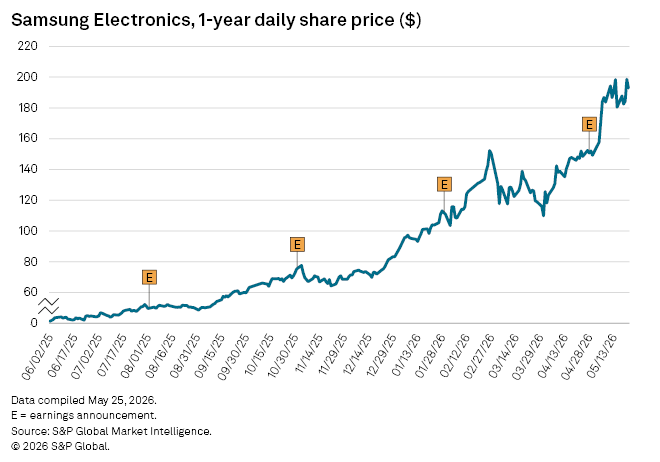

Share price reaction

Shares rose modestly following the release, reflecting investor relief that strong semiconductor profitability and AI-driven demand outweighed concerns around softer-than-expected HBM execution, rising CapEx intensity, and ongoing weakness in display markets.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment