Research — May 28, 2026

Cisco postQ snapshot: AI demand powers networking rebound and lifts outlook

By Sweta Patra

Cisco Systems Inc. (NASDAQ: CSCO) delivered a stronger-than-expected Q3 2026 performance on May 13, with upside driven by a sharp acceleration in networking demand tied to AI infrastructure buildout. The beat on revenue, margins and earnings was accompanied by upgraded Q4 and full-year guidance, reinforcing management’s confidence in sustained enterprise and hyperscaler investment cycles.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

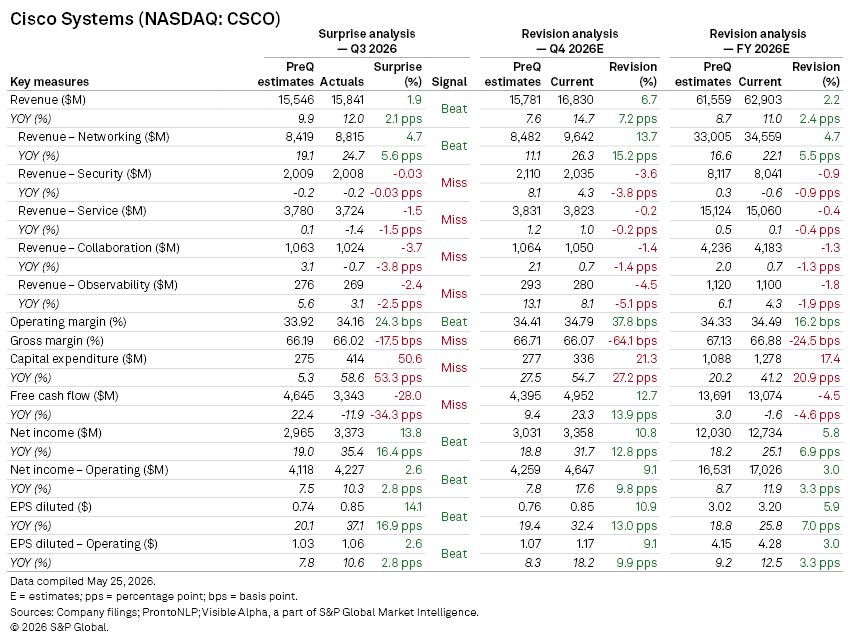

Revenue of $15.8 billion came in ahead of Visible Alpha consensus, with non-GAAP EPS of $1.06 beating expectations by 2.6%. Operating margin of 34.2% also edged above analyst forecasts.

The core networking segment was the key driver. Revenue of $8.8 billion rose 25% year-on-year and beat expectations by 4.7%, supported by enterprise infrastructure refresh cycles, early-stage AI networking deployments, and easier prior-year comparisons. Management highlighted accelerating demand linked to AI inference workloads and data center scale-out requirements.

Security revenue of $2 billion was broadly in line with expectations. However, Service and Collaboration tools remained under pressure, with revenue missing expectations amid persistent weakness in hybrid-work-related spend. Observability also slightly underwhelmed at $269 million, despite modest year-on-year growth.

Gross margin of 66% came in marginally below expectations, reflecting higher memory costs and an evolving product mix skewed toward AI-heavy hardware. Despite this, net income rose 35% year-on-year to $3.4 billion, with EPS of $0.85 materially ahead of consensus, helped by lower-than-expected operating expenses.

Free cash flow was a notable weak spot, falling 12% year-on-year to $3.3 billion and missing expectations by 28%. The shortfall was primarily driven by a sharp increase in capital expenditure, which rose 59% year-on-year to $414 million as Cisco stepped up investment in AI-related infrastructure and supply chain capacity.

Guidance

Management raised both near-term and full-year guidance, signaling confidence that AI-driven networking demand is becoming a more durable growth lever.

For Q4 2026, Cisco guided:

- Revenue: $16.7–$16.9 billion, ahead of preQ consensus of $15.8 billion

- Non-GAAP diluted EPS: $1.16–$1.18, ahead of consensus expectations of $1.07

- GAAP diluted EPS: $0.80–$0.85, above consensus expectations of $0.76

- Gross margin: 65.5–66.5% (broadly in line)

- Operating margin: 34–35% (broadly in line)

For FY2026, guidance was also lifted:

- Revenue: $62.8–$63 billion

- Non-GAAP diluted EPS: $4.27–$4.29

- GAAP diluted EPS: $3.16–$3.21

While gross margin expectations remain anchored around current levels, management signaled that operating leverage and stronger networking demand should offset ongoing mix and pricing pressure.

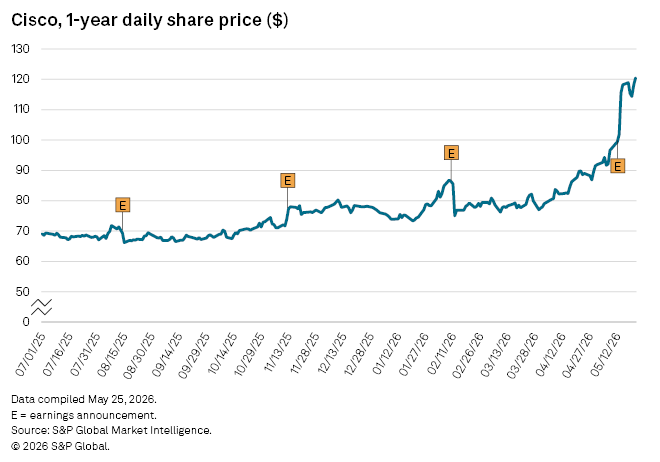

Share price reaction

Shares of Cisco rallied following the results, as investors responded to the combination of earnings beats, upgraded guidance and accelerating AI-related networking demand.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment