Research — May 28, 2026

BYD set for Q2 rebound as analysts expect volumes and earnings to recover

By Nitin Mirajkar

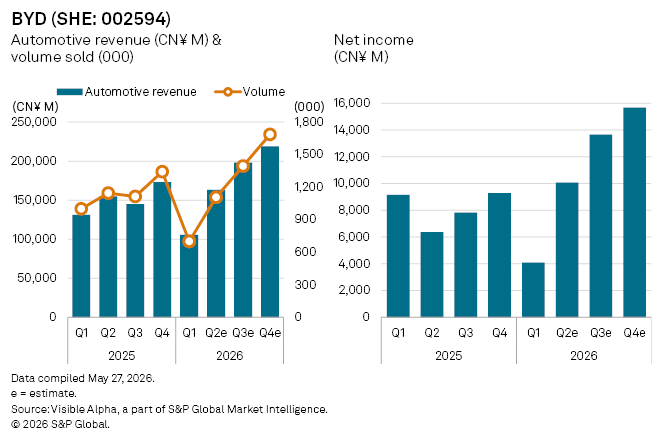

BYD (SHE: 002594) reported a sharp first-quarter earnings decline, as a combination of policy changes and seasonal weakness weighed on demand in the world’s largest new energy vehicle (NEV) market.

The downturn follows a shift in China’s incentive framework. In 2024 and 2025, NEVs were exempted from purchase tax, with a cap of CN¥30,000 per vehicle. However, for 2026 and 2027, the tax break is to be halved from the standard 10% rate, with a reduced cap of CN¥15,000 per vehicle. This policy shift caused a significant amount of demand to be brought forward to the fourth quarter of 2025, exacerbating the slump in the first quarter of 2026.

In Q1, BYD’s net income fell 55% year-on-year to CN¥4.09 billion, as automotive revenue declined 20% and vehicle volumes dropped 30% to 700,463 units.

For Q2, however, Visible Alpha consensus expectations point to a rebound, supported by new model launches and an increasingly aggressive push into overseas markets, a key strategic priority for BYD as domestic growth moderates and competition intensifies. Visible Alpha estimates suggest volumes are expected to recover to around 1.1 million units, although down 3% year-on-year. Automotive revenues, however, are projected to rise 5% to CN¥163 billion.

Profitability is expected to improve more markedly, with net income forecast to climb 59% year-on-year to CN¥10.1 billion. Average selling prices, which rose 14% in the first quarter, are expected to increase by a more modest 9% in Q2 to CN¥149,210, implying some easing from the previous quarter’s peak levels.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment