ECONOMICS COMMENTARY — 24 Apr, 2026

Week Ahead Economic Preview: Week of 27 April 2026

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

Central banks to weigh stagflation risks amid GDP, PMI and inflation updates

Central bank policy meetings for all the major developed economies, plus GDP, PMI surveys and key inflation data, make for an unusually busy week as far as the economic diary is concerned.

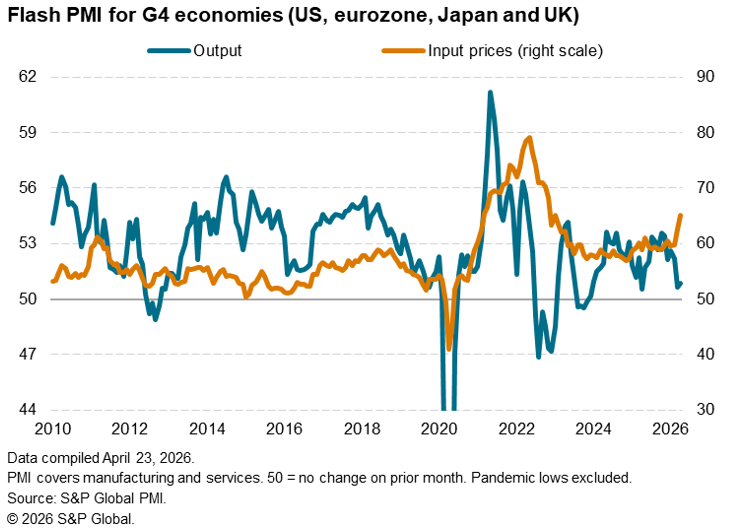

Rate setters gather to determine monetary policy in the US, Canada, the eurozone, Japan and the UK, as well as in Brazil and Mexico. The meetings follow increasing signs of “stagflationary” forces starting to take hold around the world, most recently through the flash PMI surveys for April. These surveys, which are closely watched by central banks, showed prices surging higher amid the energy price spike and supply shortages emanating from the conflict in the Middle East. Meanwhile, any signs of robust growth were largely limited to stockpiling ahead of further possible supply shortages and price hikes.

This makes for a policy dilemma, as any interest hikes to fight inflation could drive economies into downturns, whereas lower rates could turn any short-term, or transitory, price spike into a more prolonged inflation problem. It would be understandable at this stage if no immediate policy decisions were made, but how each central bank weighs these risks will be eagerly assessed through the communications surrounding the meetings.

The broader global manufacturing PMI survey releases at the end of the week will provide additional insights into economic trends beyond those already seen in the flash PMIs, notably widening the coverage of April’s data to mainland China and the host of Asian economies that are especially vulnerable to the closure of the Strait of Hormuz.

We will also see first quarter GDP estimates for the US, eurozone, Taiwan, Mexico and Sweden, albeit with these backward-looking data looking somewhat stale in comparison to the April survey data that have become available since the war broke out. Note also that these early estimates generally include very little hard data for the final month of the quarter, which in this case was the month after war broke out on 28 February.

However, some further data release that reflect conditions after the outbreak of war will be of particular interest, with core PCE inflation – the Fed’s preferred price gauge – and eurozone CPI inflation for April both updated on Thursday.

Chart of the week: Flash PMIs highlight growing stagflation risk

S&P Global’s flash PMI data showed output growth continuing to run at only a very modest rate across the major developed economies in April, as the war in the Middle East dampened demand.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings