Research — April 2, 2026

Water, energy pressures are driving up Chile's mining costs

By Monica Ramirez and Jason Holden

Chile is the world's copper capital; the country produces about 27% of global copper output. It is also a pivotal player in battery metals, with the world's fifth‑largest lithium reserves and resources. For mining companies, few places offer greater opportunity. However, these advantages are increasingly offset by rising operational challenges, as water scarcity, escalating energy costs and declining ore quality add sustained pressure on margins.

➤ Water scarcity has evolved from a concern to a production-limiting factor for Chile's mining sector.

➤ Lower ore grades mean that miners must process significantly more material, escalating both water use and energy consumption.

➤ Desalination provides water security but requires higher energy intensity and substantial infrastructure investment.

➤ Production forecasts are being trimmed as operational cost pressures from water, energy and declining grades converge.

The most immediate crisis is water. Chile's Atacama Desert, one of the driest places in the world, is a center for copper and lithium mining. It is currently experiencing a prolonged drought, now in its 14th year, which has cut reservoir capacity to about 30%. Water is not a secondary concern for miners; it is a critical operational input used in ore processing, dust suppression and equipment cooling. Falling ore grades have compounded the problem: Lower-quality ores require more water to process the same amount of metal, driving up costs. The consequences have already hit production.

At BHP Group Ltd.s Cerro Colorado operation, output declined significantly following regulatory restrictions on groundwater extraction aimed at protecting nearby wetlands, while production at Anglo American PLC's Los Bronces mine has fallen by as much as 44%, linked directly to reduced water availability during the prolonged drought. Antofagasta PLC announced in late 2025 that its production would only reach the lower end of its forecast due to rising input costs for diesel and ongoing water shortages in northern Chile. The company's pivot to desalination — now the industry's primary long-term response — clearly illustrates the cost implications. Desalinating seawater is highly energy-intensive, 10 times more costly than extracting groundwater. Transporting it to remote, high-altitude mines via long pipeline systems is itself enormously energy-intensive, with about 70% of pipeline operating costs attributable to energy use alone.

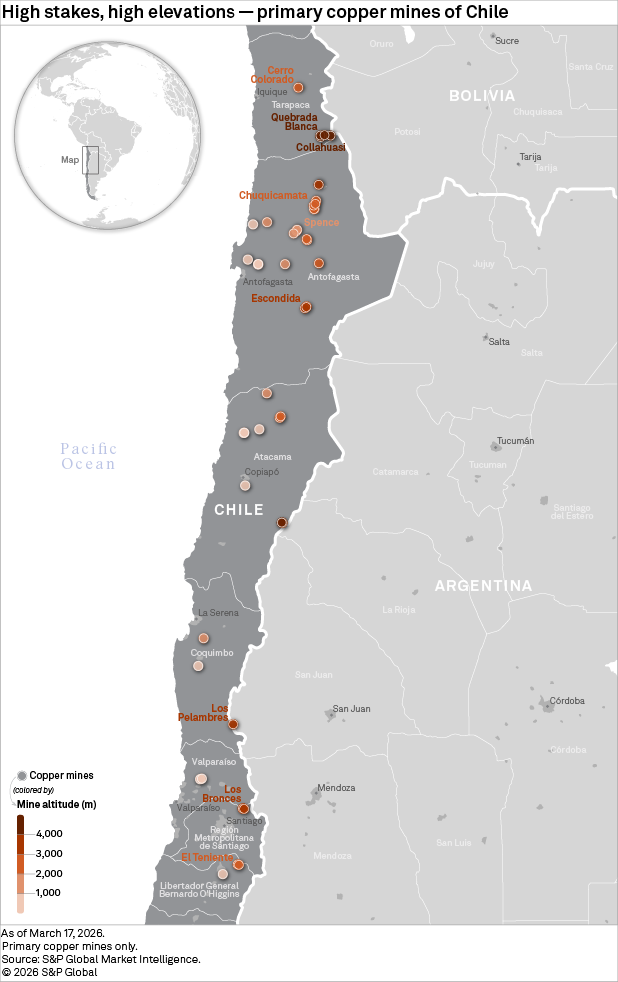

A critical factor shaping these operational challenges is altitude. Chile's copper mines span a vast range, from coastal operations below 400 meters to extreme elevations above 4,500 meters at world-class assets such as Collahuasi and Quebrada Blanca. Our statistical analysis shows that after controlling for ore grade and production scale, higher altitude is associated with lower all-in sustaining costs (AISC), contrary to expectations. This is not because high-altitude operations are inherently cheaper; rather, it reflects a powerful selection bias. The immense capital required to build and operate infrastructure at such elevations — like the 170-kilometer water pipeline to the Escondida mine at 3,200 meters — means that only the most economically robust, high-grade ore bodies are developed. This finding underscores the article's central theme: While the geology of these high-altitude deposits can lead to lower unit costs, the structural hurdles of water and energy supply demand massive, long-term capital investment that raises the barrier to entry.

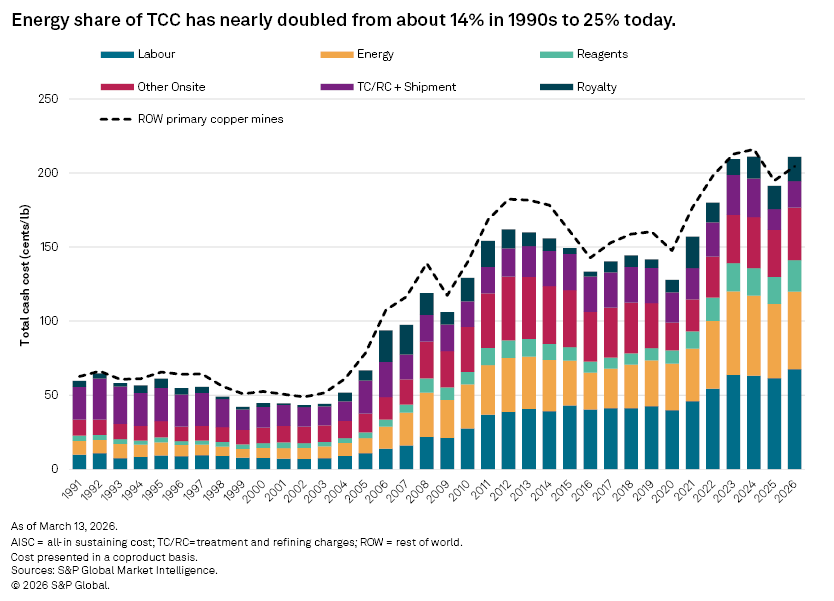

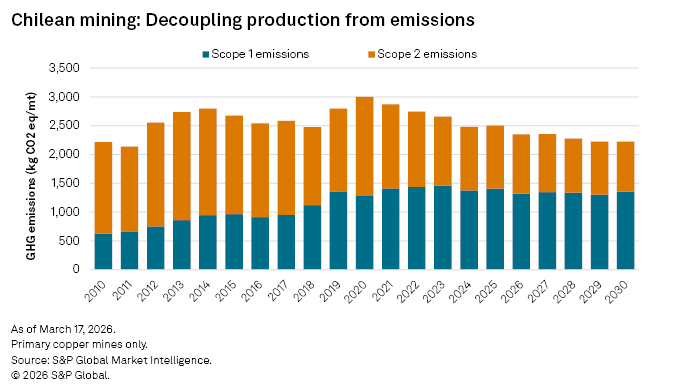

Energy is the second major pressure point. Modern Chilean copper mines face declining ore grades, increasing operational depths and high energy requirements simultaneously — a triple burden that compounds costs at every stage of extraction and processing. The sector's reliance on diesel exposes it to volatile global energy markets, with recent tensions around the Strait of Hormuz driving higher global fuel prices and highlighting the vulnerability of fuel‑intensive operations, particularly those in remote locations with limited grid access. Between 1990 and 2020, emissions from copper and other mining activities in Chile tripled, driven in part by greater diesel consumption as operations scaled up to compensate for falling ore quality. However, since 2020, the sector has begun abating emissions as major mines transition to renewable electricity and implement decarbonization commitments.

The industry is responding on multiple fronts. On energy, the transition away from diesel and coal toward renewables is accelerating. By late 2024, non‑conventional renewables (NCRE) accounted for about 50% of installed capacity, while renewables supplied approximately 68%-70% of total electricity over the year, with wind and solar contributing 33% annually. This has been one of the fastest energy transitions globally, providing a strong foundation for miners seeking to reduce their power costs. Several of the largest copper operations in northern Chile, including Collahuasi and Antofagasta Minerals' flagship assets, now meet their daytime electricity demand entirely from renewable sources during peak solar‑generation hours.

Water supply is also being fundamentally restructured. Seventeen of Chile's 24 desalination plants now serve the mining sector, and by 2034, an estimated 71.5% of mining water is projected to come from seawater rather than continental sources.

Innovation in water recycling is also helping. Closed-loop systems now achieve 76% water reuse across mining operations, and if permitting and technology scale as planned, the sector could reduce fresh water use to just 5% by 2040. Chile's National Mining Policy 2050 had already set an ambitious target of limiting continental water use to 10% by 2025, though industry projections suggest the transition toward seawater will occur more gradually.

Water constraints in northern Chile extend beyond copper. The Salar de Atacama hosts some of the world's largest lithium brine operations, operated primarily by Sociedad Química y Minera de Chile SA and Albemarle Corp. Pressure on local water resources is intensifying as Chile seeks to expand lithium production under its national battery materials strategy. The government has introduced a new lithium framework that positions Codelco and Empresa Nacional de Minería as partners alongside private operators. The framework encompasses adjustments to existing operating areas in the Salar de Atacama and contemplates new developments such as the Salares Altoandinos project. The cost and margin implications of these developments, particularly for brine operations, are examined in our recent lithium margin analysis.

Water scarcity is therefore emerging as a basin-scale constraint that affects multiple mineral supply chains. At the same time, the environmental profile, which is now central to supporting expansion in both copper and lithium, depends heavily on energy sourcing and brine discharge management. Strong integration of renewable energy and robust environmental monitoring is becoming critical to minimize long-term impacts. These factors highlight structural cost pressures facing the industry. Declining ore grades and new water infrastructure raise the long-term cost base, while cyclical operating costs fluctuate with exchange rates, input prices and by-product credits.

The structural challenges are unlikely to resolve quickly, as they are permanent. Ore grades will continue to fall, and the Atacama's arid climate will not fundamentally change. The cost of building, powering and maintaining desalination and pipeline infrastructure will remain a significant burden on balance sheets for years to come. For the companies that can absorb those structural costs, Chile remains an indispensable cornerstone of global supply. For those that cannot, the world's copper capital is becoming an increasingly expensive place to do business.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.