Research — April 10, 2026

Visible Alpha breakdown of US banks’ first-quarter 2026 earnings expectations

By Jigar Saiya

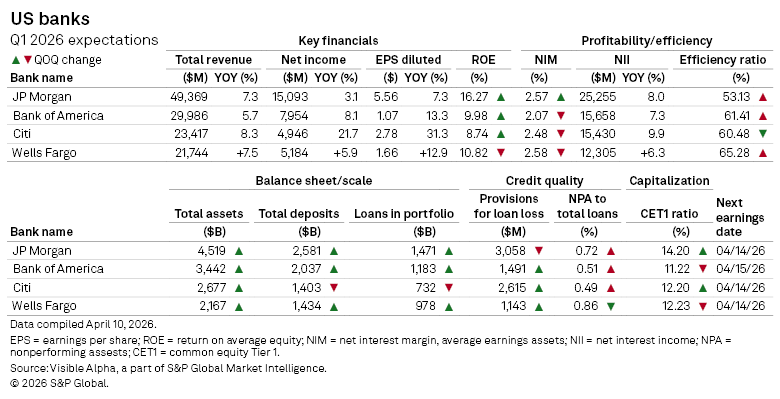

US large-cap banks kick off first-quarter earnings season on Tuesday, April 14, with JPMorgan Chase & Co. (NYSE: JPM) Citigroup Inc. (NYSE: C), and Wells Fargo & Co. (NYSE: WFC) reporting first, followed by Bank of America Corp. (NYSE: BAC) on Wednesday.

The big four entered 2026 with strong momentum following a record 2025, supported by resilient economic activity, moderating inflation, and still-elevated interest rates. Markets have remained constructive but volatile, with rate-cut expectations shifting and capital markets activity gradually improving from late-2025 lows. Against this backdrop, Visible Alpha consensus expectations point to steady top-line growth, modest profitability gains, and early signs of normalization in credit costs.

Across the group, revenues are expected to grow in the mid-to-high single digits year-over-year, led by JP Morgan (+7.3%), Citi (+8.3%), Wells Fargo (+7.5%), and Bank of America (+5.7%). This growth is driven by continued strength in trading and investment banking pipelines, which began recovering in Q4 2025, stable loan growth, particularly in consumer and commercial segments, and elevated (though plateauing) net interest income (NII) levels.

Profitability is expected to improve, with EPS growth ranging from 7% at JP Morgan to over 30% at Citi, the latter benefiting from restructuring progress and operating leverage. ROE trends are expected to be mixed, improving at JP Morgan, Bank of America, and Citi, but declining at Wells Fargo. While efficiency ratios show improvement at JP Morgan and Bank of America, and deterioration at Citi and Wells Fargo, reflecting ongoing investment spend and restructuring costs.

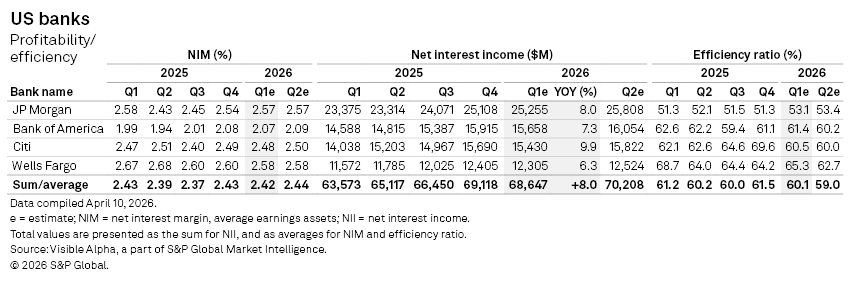

Net interest margins face incremental pressure

Despite solid revenue growth, net interest margins (NIMs) are expected to show mixed-to-declining trends. Bank of America, Citi, and Wells Fargo are all expected to see sequential NIM compression, while JP Morgan stands out with a modest NIM uptick. Banks have flagged that the peak benefit from higher rates is behind them, and Q1 expectations reinforce that trend. Still, NII remains resilient, growing across all banks.

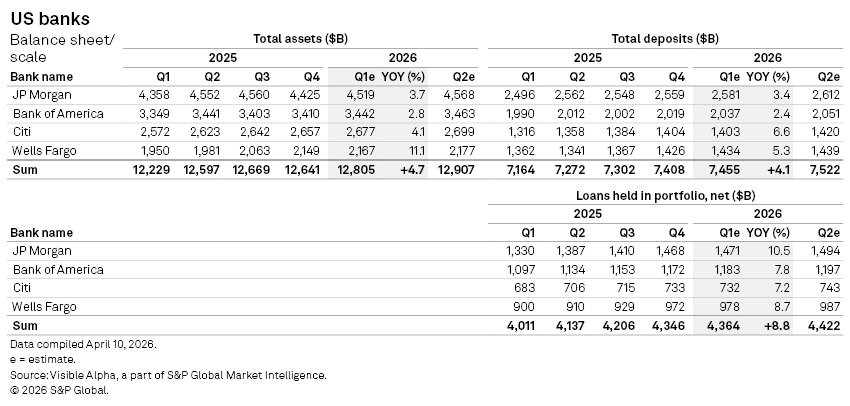

Balance sheet growth remains intact

Loan and deposit growth is expected to remain broadly positive in Q1. Total assets, deposits, and loans are seen increasing across banks. The most notable trend into Q1 is continued strength in loan growth. This builds on Q4 momentum, where banks pointed to healthy consumer balance sheets and steady borrowing activity, alongside improving corporate demand tied to a rebound in dealmaking and investment banking pipelines.

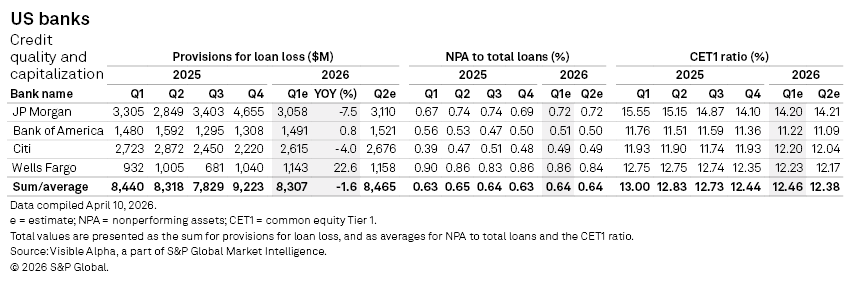

Stable fundamentals support cautious normalization

A key area of focus this quarter will be credit normalization. On aggregate level, provisions for loan losses are expected to decline modestly driven primarily by reductions at JP Morgan (-7.5% YOY) and Citi (-4%), partially offset by a notable increase at Wells Fargo (+22.6%) and a broadly flat trend at Bank of America (+0.8%).

Importantly, non-performing asset (NPA) ratios remain low, generally below 1%. So, while some banks are building reserves cautiously, actual credit deterioration remains contained.

Capital ratios show a mixed picture. JP Morgan and Citi are expected to strengthen CET1 ratios in Q1, while Bank of America and Wells Fargo are expected to see slight declines. This comes amid continued uncertainty around Basel III endgame regulations, which banks have been preparing for since late 2025. Capital return expectations (buybacks/dividends) will remain a key discussion point on earnings calls.

Overall, Q1 2026 is expected to shape up to be a solid quarter for large US banks. Revenue growth is projected to remain supported by resilient lending activity and improving market conditions, while margin pressures and elevated costs continue to weigh on operating leverage. At the same time, credit quality is seen remaining stable and capital levels strong, providing a solid foundation as banks navigate an evolving macro and regulatory environment.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings