Research — May 5, 2026

US restaurant industry 2026 expectations breakdown

By Hardik Savla

The US restaurant industry is navigating a challenging environment with a macroeconomic landscape marked by persistent inflation and a consumer that is pressured by rising prices. While consensus expectations show sales are still growing across key players in the industry supported by resilient consumer spending, the momentum is increasingly fragile beneath the surface. Operators are grappling with structurally higher labor and food costs, while facing growing resistance to further price hikes from value-conscious diners.

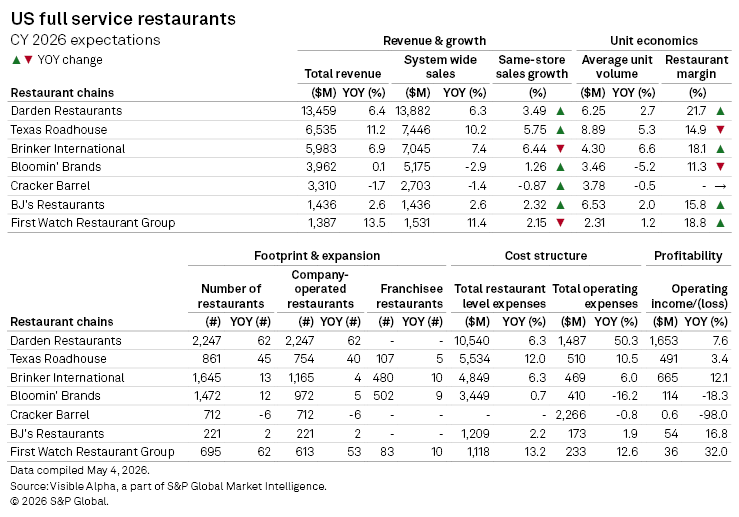

Here’s a look at Visible Alpha consensus expectations for leading US full-service restaurant chains in 2026.

Analysts expect sales to remain steady across much of the industry, while rising cost pressures and uneven demand increasingly influence earnings. Recent reports from the United States Department of Commerce show US retail and food services sales for March 2026 were up 1.7% from the previous month, and up 4% from March 2025. This aligns with what analyst expectations are showing: consumer demand has not weakened significantly, but it has become more selective.

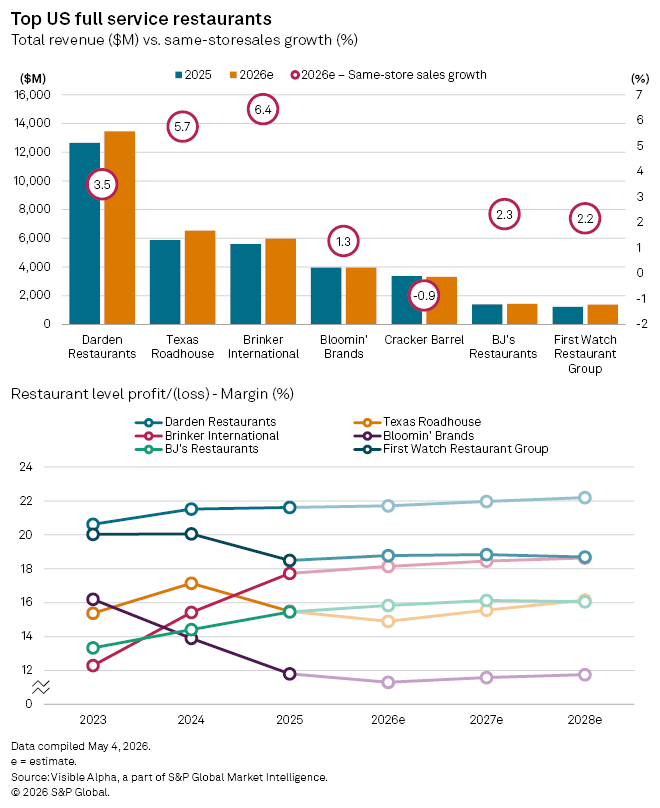

At the top end, analysts expect continued outperformance from scale leaders and premium casual concepts. Darden Restaurants Inc. (NYSE: DRI) is projected to deliver steady mid-single-digit revenue growth (~6%) with positive same-store sales and margin expansion, with strong growth expectations for its brands Olive Garden and LongHorn Steakhouse in 2026. Historically high labor and food costs along with restructuring costs from the Bahama Breeze exit, which will involve one-time closure and conversion costs, is expected to see operating expenses rise significantly in 2026. Recent earnings commentary highlights stable traffic and easing commodity inflation, which are contributing to a significant increase in operating income. This suggests that analysts expect operating leverage to activate following a period of high costs.

Similarly, Texas Roadhouse Inc. (NASDAQ: TXRH) is expected to remain one of the strongest performers, with double-digit top-line growth (~11%) and strong same-store sales relative to peers (~5.75%). This aligns with management’s recent emphasis on traffic-driven growth and continued unit expansion. However, analysts expect a slight dip of 58 bps year-on-year in restaurant margins to 14.91% in 2026, due to ongoing commodity pressures (specifically beef) and labor costs, even as volumes remain robust.

In the mid-tier, Brinker International Inc. (NYSE: EAT) is expected to see same-store sales growth normalize in 2026, following an exceptionally strong prior year that set a high base for comparison. Recent results from its core Chili’s brand came in below pre-quarter consensus expectations, with management pointing to softer January trading due to adverse weather and calendar shifts. At the same time, analysts expect continued weakness at Maggiano’s Little Italy to weigh on overall performance. Even so, the margin outlook is more constructive. Consensus forecasts point to an improvement in restaurant-level profitability, as the company continues to drive recent initiatives around menu simplification, pricing architecture, and operational efficiency.

By contrast, Bloomin' Brands Inc. (NASDAQ: BLMN) and Cracker Barrel Old Country Store Inc. (NASDAQ: CBRL) are expected to lag. Bloomin’ expectations show flat revenue and declining system-wide sales, with meaningful drops in operating income, due to ongoing traffic softness and international exposure challenges, which the company highlighted in recent earnings. The company is currently focused on a turnaround strategy aimed at stabilizing its core brands, specifically Outback Steakhouse. Cracker Barrel’s outlook is more severe, with negative revenue growth, same-store sales, unit contraction, and near-zero profitability, as analysts expect continued turnaround challenges tied to brand positioning and cost structure.

Smaller growth-oriented players present a more mixed but generally positive picture. First Watch Restaurant Group Inc. (NASDAQ: FWRG) is expected to deliver strong revenue growth (~13%) driven by aggressive unit expansion, though slightly lower same-store sales expectations compared to last year suggest new unit growth is doing the heavy lifting. Meanwhile, BJ's Restaurants Inc. (NASDAQ: BJRI) is seen as a steady recovery story, with modest sales growth but improving margins and strong operating income growth (~17%), as the company continues to focus on cost discipline and menu pricing actions.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment