ECONOMICS COMMENTARY — 01 Apr, 2026

US manufacturers show resilience on outbreak of war despite rising prices and supply delays

US manufacturers reported faster growth of output and order books in March, pointing to encouraging resilience in the face of the outbreak of war in the Middle East. However, key areas of concern at the moment are prices and supply chains. A sharp rise in prices and delivery delays has cast a cloud over the outlook, threatening to drive inflation higher, dampen demand and throttle supply chains.

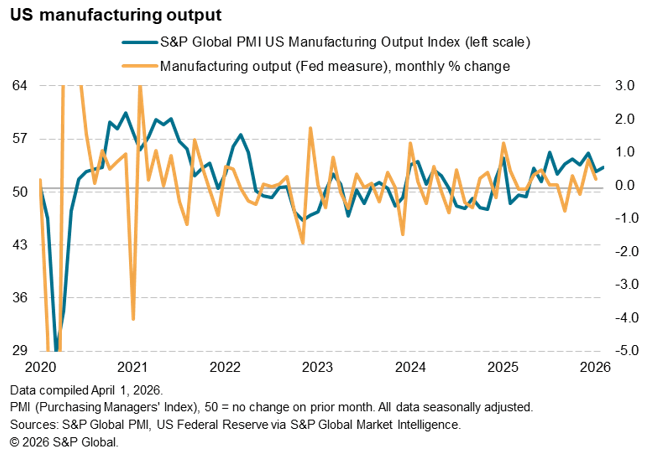

Robust output growth persists

S&P Global’s manufacturing PMI surveys indicated rising output among manufacturers in March, the rate of growth ticking higher to round off a solid first quarter. Production has now risen for eight straight months, with the March PMI reading consistent with a monthly rise in industrial production of approximately 0.5%.

Demand was reportedly supported principally by improved domestic sales, in part linked to protection from tariffs and some inventory building, offsetting a further drop in exports. Export sales have dropped continually over the past nine months, but total order book volumes have risen in all of the past 15 months bar December, rising at an increased rate in March.

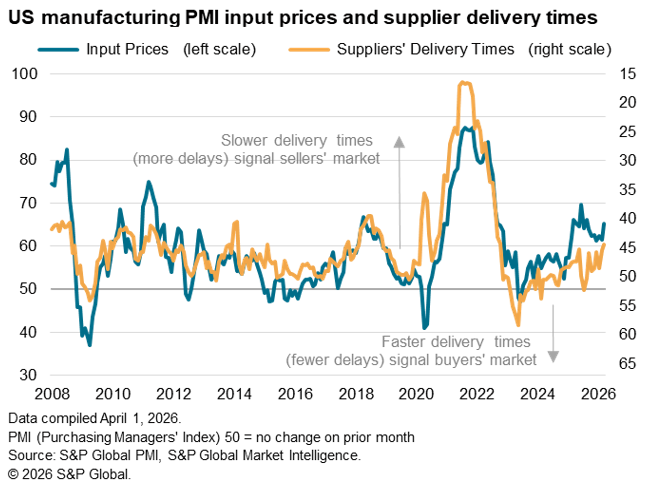

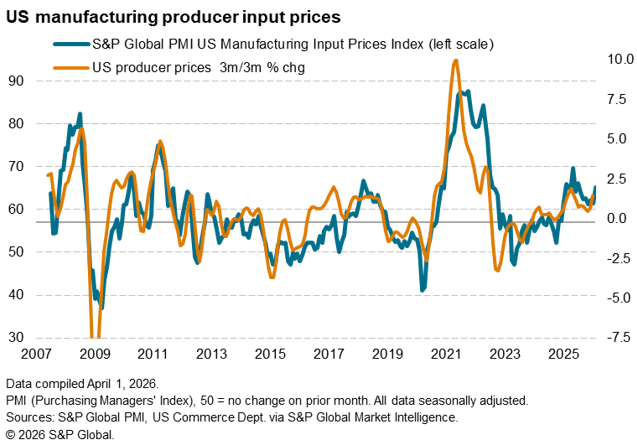

Price and supply worries

Few instances were reported of the war in the Middle East having so far directly affecting either production or order books, although March saw some cases of manufacturers and their customers building stocks as a precaution against future price rises or supply shortages.

Prices paid for inputs have jumped higher thanks primarily to the impact of higher oil prices, with the rate of inflation accelerating to the highest since last August, while supplier delays have become more widely reported than at any time since October 2022, linked to the war exacerbating existing shipping, haulage and port delays.

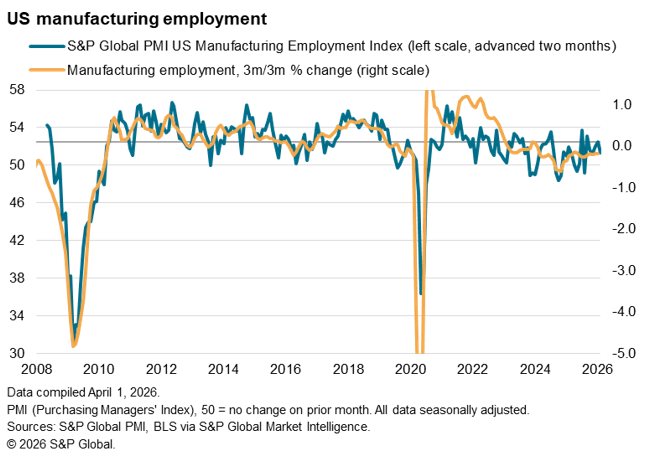

Hiring on hold

March also saw a worrying lack of hiring, with manufacturing payrolls instead remaining under pressure as factories sought to reduce staffing costs in the face of rising energy and raw material prices. Only a marginal increase in employment was reported by the survey panel, representing the smallest increase since last July and suggestive of a further fall in official manufacturing payroll numbers according to historical comparisons.

Outlook steady, for now

If price pressures and supply delays persist, demand, employment and production capabilities will inevitably start to be more seriously affected. However, business confidence regarding output in the year ahead has so far held up well, especially in relation to manufacturers in other economies, notably in Europe. Expectations for output in the year ahead cooled only marginally in March among US producers, running at one of the highest levels seen over the past year.

Sustained optimism in part reflecting reduced concerns over government policies such as tariffs, but also indicated that producers anticipate only a short-term and modest impact from the war. Much therefore hinges on the duration of the war and its related energy market disruption.

There may also be a delay by which the rise in energy prices (and related pull-back in interest rate cut expectations) feeds through to order books, as customers start to feel the pinch more in April. Supply chain delays will also take a while to feed through. Upcoming PMI data will therefore be important to monitor.

Access the latest PMI press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings