Research — May 5, 2026

Urban Company revenue to triple by 2030 as take rates and platform monetization rise

By Gourav Prasad and Lovey Mangal

India’s on-demand consumer services market continues to evolve rapidly as urban consumers increasingly prioritize convenience and immediacy. Within this shift, Urban Company Ltd. (NSE: URBANCO) is emerging as a scaled platform beneficiary, with Visible Alpha consensus pointing to a multi-year compounding growth and improving monetization profile.

Urban Company is a popular on-demand home services platform that connects users with trained professionals for everyday needs including salon services, spa services, home cleaning, repairs, appliance installation/maintenance, and pest control while also having a direct-to-consumer offering in products such as water purifiers and smart home devices.

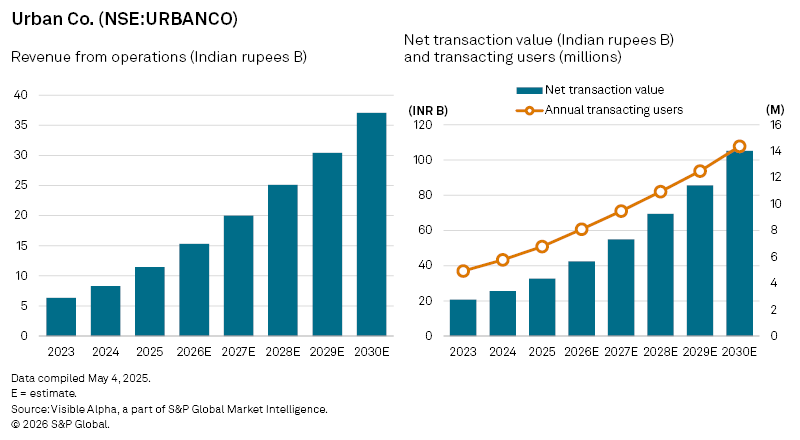

Consensus estimates project revenues rising from ₹6.4 billion in 2023 to ₹15.3 billion in 2026 and ₹37.1 billion by 2030, reflecting sustained double-digit growth alongside expanding platform efficiency. Importantly, growth is increasingly supported by improving unit economics rather than demand alone.

Net transaction value, a key indicator of platform activity, is projected to scale sharply, rising from ₹20.8 billion in 2023 to ₹42.5 billion in 2026 and ₹105 billion by 2030. This growth is supported by rising transacting users, from 4.9 million in 2023 to 8.1 million in 2026 and 14.4 million by 2030, alongside rising spend per user and greater order frequency, particularly in tier 1 and tier 2 cities.

At the same time, take rates in the core India Consumer Services (ICS) business are forecast to expand from 30.6% in 2023 to around 36% in 2026, a sign of improving pricing power.

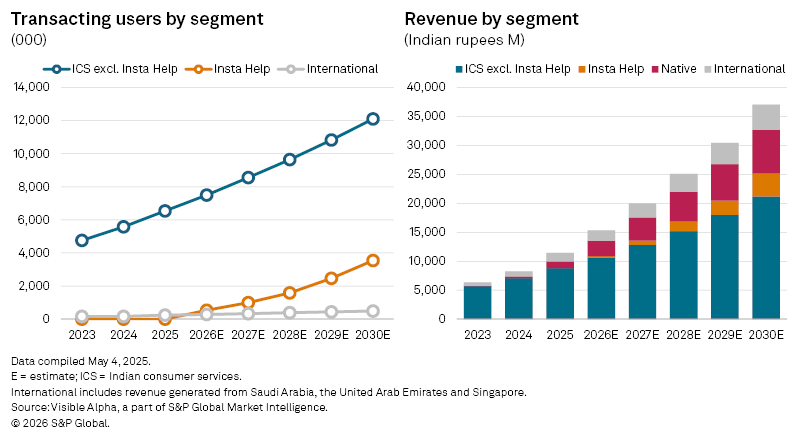

The ICS segment remains the primary growth engine. Revenues in this division are expected to rise 23% year-on-year to ₹10.9 billion in 2026. Analysts anticipate that annual transacting users will grow from 6.5 million last year to 7.5 million in 2026, reaching 12.1 million by 2030, while spend per user increases from ₹4.2K to ₹5.1K over the same period. Net transaction value in ICS is projected to nearly double from ₹31.4 billion in 2026 to ₹61.5 billion by 2030.

A notable addition within ICS is “Insta Help”, Urban Company’s push into high-frequency, near-instant housekeeping services. While first-year revenues are expected to be relatively modest at ₹195 million, the service is designed to build habitual usage. Transacting users are projected to rise from 543K in 2026 to 3.5 million by 2030, with net transaction value expanding from ₹858 million to ₹17.4 billion. Take rates are expected to remain deliberately conservative at 22–23%, reflecting a strategy focused on market penetration over margin expansion in the near term.

Beyond services, Urban Company’s “Native” D2C segment is forecast to deliver the fastest growth, with revenues rising 131% year-on-year to ₹2.7 billion in 2026. The segment benefits from a structurally higher revenue capture, with revenue accounting for 75–85% of transaction value due to the absence of partner revenue sharing. Growth has been driven by an expanding product portfolio, as well as deeper integration within the platform’s ecosystem.

International operations, spanning Saudi Arabia, the UAE and Singapore, are expected to grow more steadily, with revenues rising 20% to ₹1.8 billion in 2026. Saudi Arabia remains the dominant market, contributing roughly 77% of international sales.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment