Research — May 5, 2026

UnitedHealth postQ snapshot: Cost discipline, Optum drive beat, guidance mixed

By Mohd Naim

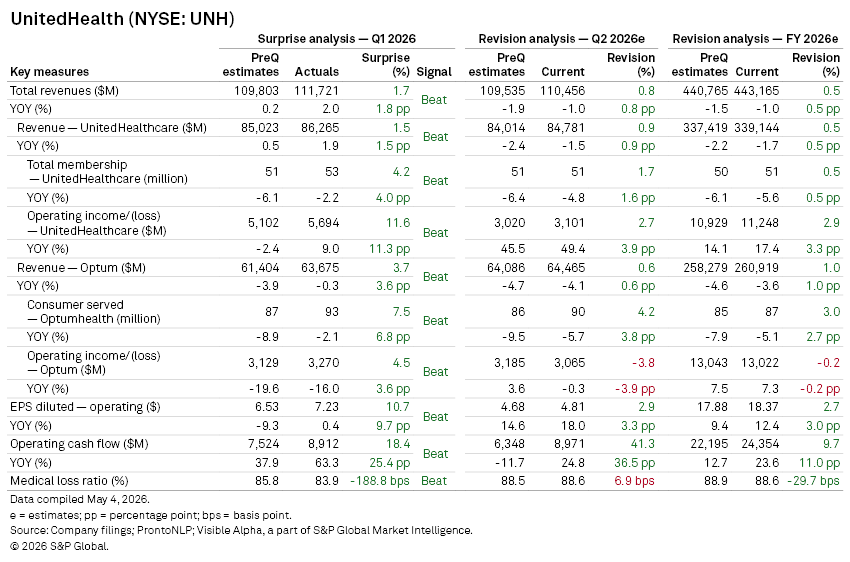

UnitedHealth Group Inc. (NYSE: UNH) reported a strong Q1 2026, with earnings comfortably ahead of Visible Alpha consensus expectations as lower medical costs and operational improvements across its platforms offset a more modest top-line beat.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha consensus pre-quarter expectations and revised outlook, here are some key takeaways.

Key takeaways

- Revenue of $111.7 billion in Q1 rose 2% year-on-year and came in slightly ahead of Visible Alpha consensus expectations, while diluted EPS (operating) of $7.23 exceeded expectations by a wide margin.

- Performance across segments was solid. UnitedHealthcare delivered revenue of $86.3 billion, modestly ahead of consensus expectations, while segment operating income beat analyst expectations by double digits as margins expanded on repricing actions and a more favorable membership mix.

- Optum continued to be a key growth driver, with revenue of $63.7 billion surpassing consensus expectations, supported by stronger consumer growth and operational improvements, particularly within Optum Insight following its financial services realignment.

- A key positive was medical cost performance. The medical loss ratio (MLR) came in at 83.9%, well below expectations and improving from 84.8% a year ago, signaling lower-than-anticipated utilization and effective pricing actions.

- Membership trends were also more resilient than expected, with total UnitedHealthcare membership reaching 53 million despite strategic exits, and the anticipated contraction moderating meaningfully.

- Cash generation was a standout. Operating cash flow of $8.9 billion (1.4x net income) exceeded expectations and grew sharply year-on-year, pointing to strong earnings quality and balance sheet flexibility.

- Capital allocation remained balanced, with continued shareholder returns alongside ongoing investment in technology and AI capabilities.

Guidance

- Guidance, however, was more nuanced. The company raised its full-year EPS outlook to above $18.25, now ahead of Visible Alpha preQ consensus.

- By contrast, revenue guidance of over $439 billion came in slightly below expectations, and operating cash flow guidance was reduced relative to prior consensus, suggesting a more deliberate trade-off between growth and profitability.

Analyst Q&A highlights

- Medical cost ratios are expected to be lower in the first half before rising in the second, reflecting regulatory changes in Medicare Part D, while Optum Health earnings are set to build progressively through the year.

- Longer term, the company reiterated its target to move Medicare margins toward the upper end of the 2–4% range by 2027, supported by repricing and a more favourable rate backdrop.

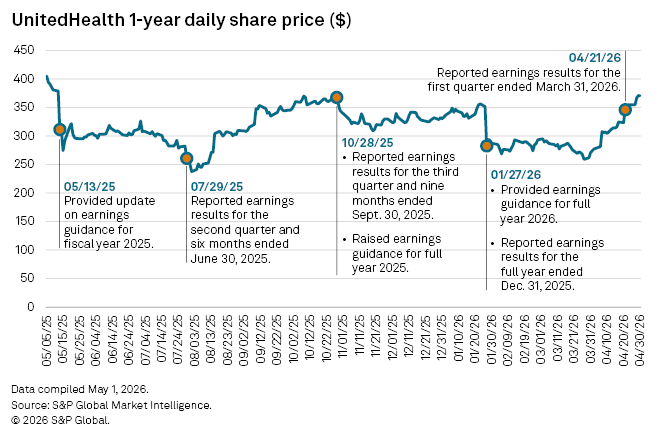

Share price reaction

- Investor reaction was positive. Shares rose sharply following the earnings release, as the market focused on the earnings beat, improved cost management, and increased EPS guidance, suggesting renewed confidence in execution after a period of uncertainty.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment