ECONOMICS COMMENTARY — 23 Apr, 2026

UK growth picks up in April, but inflation and supply disruptions spike amid war impact

The UK economy has gathered some renewed momentum in April after the initial impact of the war in the Middle East caused growth to stall in March, but the upturn comes with a catch. The improved rate of expansion is in part a reflection of a short-term boost from a rush to secure purchases ahead of feared price rises and supply shortages linked to the war.

Prices have spiked higher at a rate not previously seen by the survey outside of the pandemic, suggesting inflation could rise more than many forecasters have been anticipating. Prices are rising not just because of surging energy costs, but also due to increases in charges levied for a wide variety of goods and services, with price hikes often stoked by supply concerns. The number of supply delays reported has jumped to the highest on record if the pandemic is excluded.

Business confidence and employment have also been dragged lower by the ongoing conflict, boding ill for growth to weaken in the coming months just as price pressures intensify.

The survey highlights the difficult choices facing policymakers at the Bank of England. The spike in price pressures will add to calls for rate hikes to dampen inflation, but the Bank will need to carefully assess the degree to which economic growth might weaken. While April’s PMI is indicative of the economy rebounding from a flat picture in March to a 0.2% quarterly growth rate, the details of the survey hint strongly that this pace cannot be sustained should the crisis persist.

Business growth rebounds after initial war hit

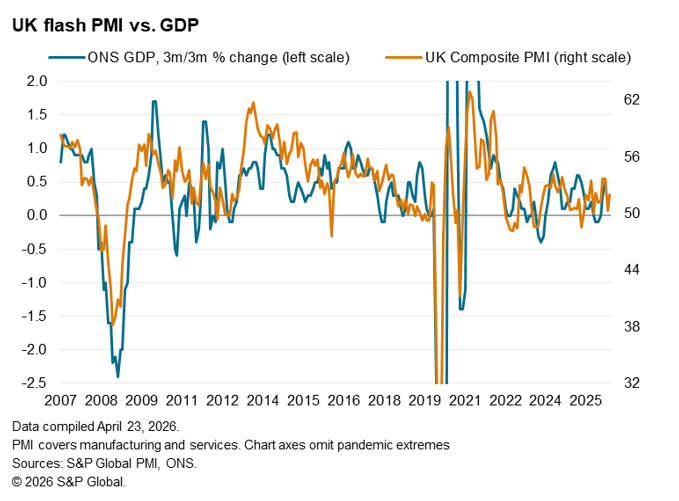

A promising start to the year faded in March as some businesses reported a drop in activity linked to the outbreak of war in the Middle East, but economic growth has rebounded in April. Having slumped from 53.7 in February to just 50.3 in March, the headline Composite PMI Output Index has risen to 52.0 in April, according to the preliminary ‘flash’ reading.

The data suggest that, after the economy stalled in March, April has seen the pace of economic growth (or GDP) accelerate to a 0.2% quarterly rate.

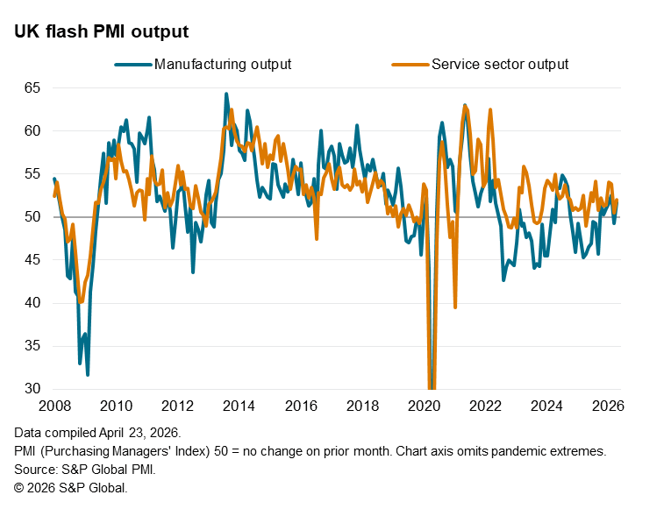

Manufacturing output rebounded after having fallen in March for the first time in six months. Service sector growth likewise recovered, having come close to stalling in March. However, on both counts, April’s expansion has failed to match the growth seen in February, before the US-Israeli attacks on Iran and subsequent closure of the Strait of Hormuz.

Further economic stress likely lies ahead. While the impact of the war on output has so far been relatively benign, other indicators point to a far more worrying hit to the economy via higher inflation, supply chain disruption and falling business confidence.

Inflation shock

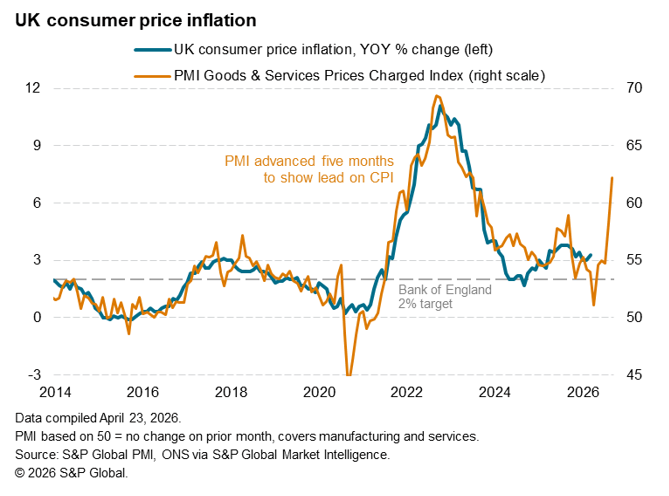

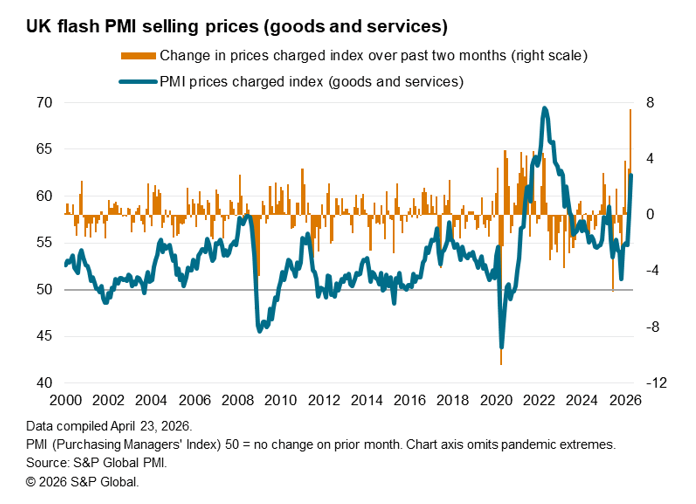

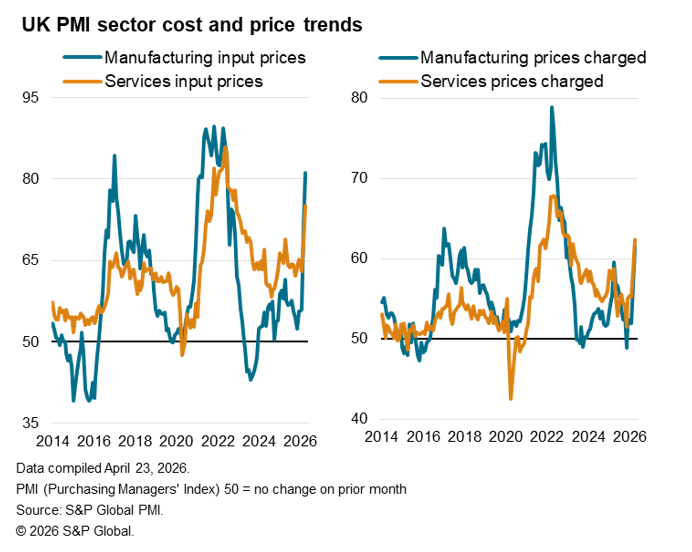

The survey data point to a sharp acceleration of inflation. The increase in the survey’s gauge of selling price inflation has risen over the past two months, reaching its highest since February 2023. At this level, the PMI gauge is indicative of consumer price inflation spiking sharply higher in the coming months from the current 3.3% rate.

To underscore the inflation shock, the rise in the PMI selling price index since February has been the largest recorded since comparable data were available in 2000.

Higher selling prices reflected higher costs. Service sector input cost inflation jumped to the greatest extent on record for the survey, reaching its highest since November 2022, while factory input cost inflation also accelerated sharply, building further on the spike seen in March (which marked the sharpest rise in the index since 1992). That took manufacturing input cost inflation to its highest since June 2022.

Much of the increase in prices was attributed to the Middle East conflict, notably via higher energy costs, though with suppliers of many goods and services widely reported to have been raising prices, often associated with a war-related supply squeeze. Higher staffing costs, commonly linked to April’s larger than usual rise in the minimum wage, was a secondary factor, exacerbating the war-related price rises.

Supply squeeze

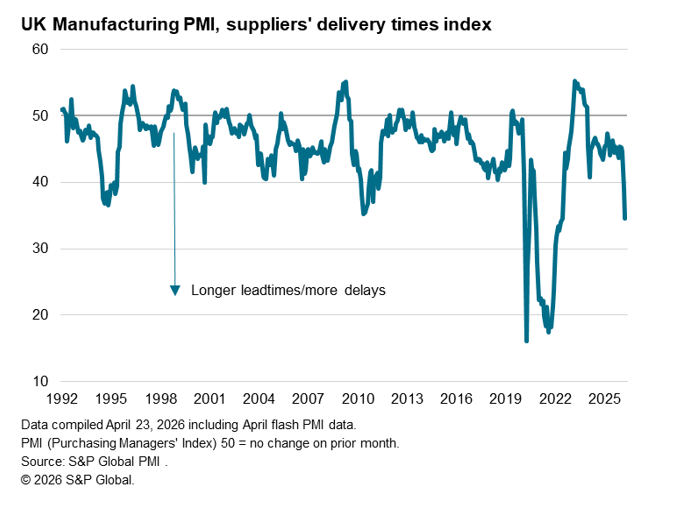

A further major impact on the economy from the war is evident through a spike in the number of supply chain delays. Manufacturers reported the greatest lengthening of supplier delivery times since June 2022. Barring the pandemic, the lengthening of lead times seen in April was the highest since data were first available in 1992, and was overwhelmingly blamed by survey participants on disruptions caused by the conflict in the Middle East.

Safety stock build flatters demand picture

Fears of further price hikes and supply shortages have already prompted a wave of inventory building among companies. This buying has provided a short-term boost to demand for goods and certain services which are supply dependent. For example, manufacturing input buying showed the second-largest gain seen for nearly four years in April, with around two-fifths of all companies reporting higher purchases directly linking that increase in buying to war-related price or supply worries. In some cases, customers also brought forward some activities such as travel through fear of future cancellations.

This pulling-forward of demand and safety stock building warns of a temporary nature to some of the business activity growth reported in April.

Confidence slips further

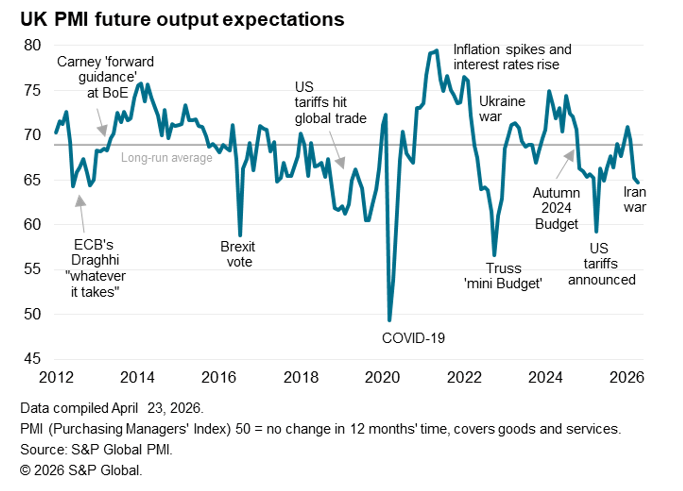

A further sign of stress in the economy was provided by another downturn in business confidence about the outlook for the coming 12 months. Future output expectations sank to their lowest since last April, when confidence had been hit by fresh news of additional US tariffs, descending further below the survey’s long-run average.

The deterioration in confidence over the past two months marks a sharp reversal of the recovery of confidence seen at the start of the year. However, the index remains well above some of the lows seen over the survey history to hint at some encouraging ‘resilience’ of business sentiment, albeit potentially buoyed by current demand proving stronger than many had anticipated due to the precautionary spending ahead of further price or supply issues in the coming months.

Job losses persist

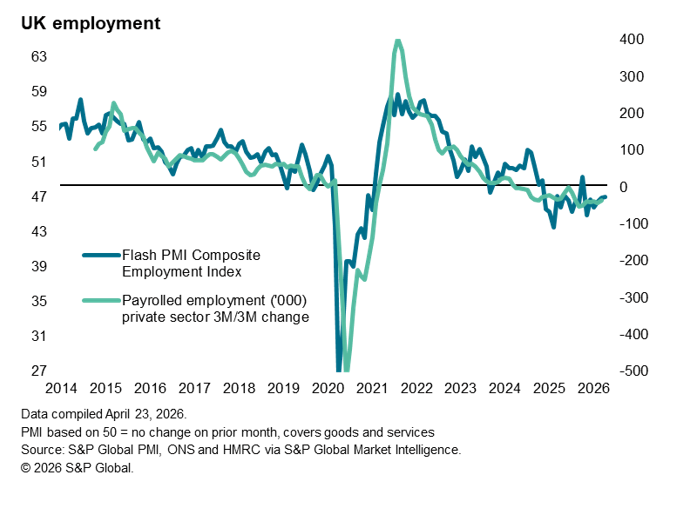

The combination of low confidence and high input costs led to further job losses in April. As well as high raw material and energy prices, companies again cited government policies such as the rise in the minimum wage as having deterred hiring. The survey’s gauge of employment has signalled falling staffing levels continually since the autumn Budget of 2024.

While the rate of job losses eased slightly in April, it remained high by historical standards of the survey due primarily to steepening job cuts in the service sector. Manufacturing jobs showed a surprise upturn, rising for the first time since October 2024. However, this improvement partly reflected the hiring of staff to meet the recent increase in demand, which in turn was linked to short-term inventory building, to suggest the hiring upturn may prove short-lived.

Read the press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings