ECONOMICS COMMENTARY — 23 Apr, 2026

Japan flash PMI signals record price rise and fading growth amid ongoing war in the Middle East

The S&P Global Flash PMI® for Japan indicated the largest rise in selling prices recorded since comparable data were first available in 2007. Price hikes were often linked to the war in the Middle East, notably via energy prices and supply shortages. Supplier lead times lengthened in April to a degree nearly matching the extremes seen during the COVID-19 pandemic.

Some encouragement came from news of the fastest rise in Japanese manufacturing output for over 12 years in April. However, this good news was tainted by a cooling in service sector activity growth, as well as indications that the manufacturing upturn was in part a reflection of safety stock building as producers and their customers grew increasingly concerned over the price rises and supply shortages emanating from the war, hinting at weaker growth in the coming months. Business expectations worsened accordingly, pointing to the gloomiest outlook since 2020.

Growth fades further

The headline S&P Global Japan PMI Composite Output Index slipped from 53.0 at the end of the first quarter to 52.4 in April, according to the ‘flash’ reading. Although the survey indicates that business activity across Japan has now expanded in each of the past 13 months, accelerating to one of the fastest rates yet recorded by the survey in February, the expansion has slowed over the past two months since the outbreak of war in the Middle East.

While the growth rate remains encouragingly resilient at first glance, the sector details present a more concerning picture.

Resilience buoyed by stock building

Business activity across the service sector rose at only a modest pace that was the slowest in 11 months. That left the manufacturing sector as the main driver of the expansion. However, although factory output growth accelerated sharply to the highest since February 2014, anecdotal evidence provided by survey respondents indicated that manufacturers often raised output due to concerns over future supply shortages, or raw material input price hikes, due to the war in the Middle East.

Signs of the war impacting supply chains and purchasing behaviour were provided by several of the PMI’s sub-indices.

Suppliers’ delivery times lengthened in April to the greatest extent since May 2022, almost matching the worst readings seen at the height of the pandemic as shipping delays and shortages became more widely reported.

Meanwhile, in a rare development, inventories of raw material purchases were allowed to rise in April, up for the first time since last June and rising at a rate not exceeded for close to two years.

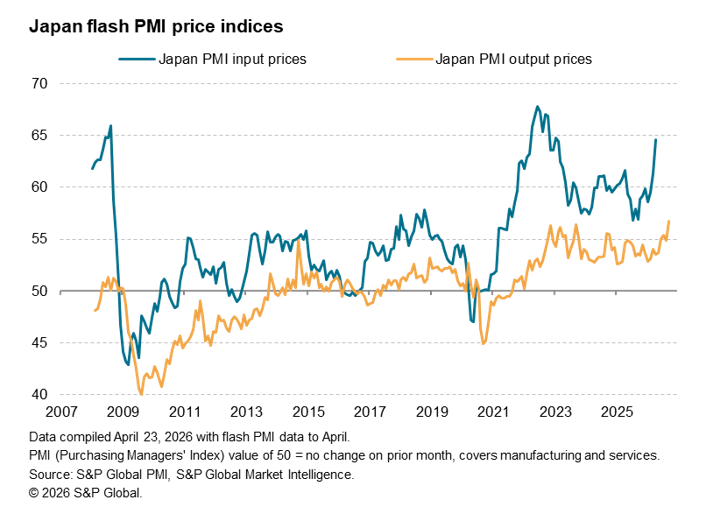

Record price surge

This additional purchasing, alongside spiking energy prices, drove input costs higher across both manufacturing and services. Average input costs faced by Japanese firms increased at the sharpest rate since January 2023 in April, while average output charges (or selling prices) rose at the quickest rate since data covering both goods and services were first available in late 2007. This points to a marked rise in consumer price inflation in the coming months.

Business confidence at lowest since pandemic

In this environment, business confidence regarding future output deteriorated for a second successive month in April, with overall optimism the lowest recorded since August 2020 during the COVID-19 pandemic (albeit well off the lows seen during the pandemic). Uncertainty and disruption to markets due to the war in the Middle East were the principal causes of dampened forecasts.

Access the press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings