Research — April 23, 2026

Insurers' FHLB advances hit new high as spread investing flourishes

US insurance companies in 2025 broadened and deepened their participation in the federal home loan bank system, increasing the magnitude of their advances to a new all-time period-end high.

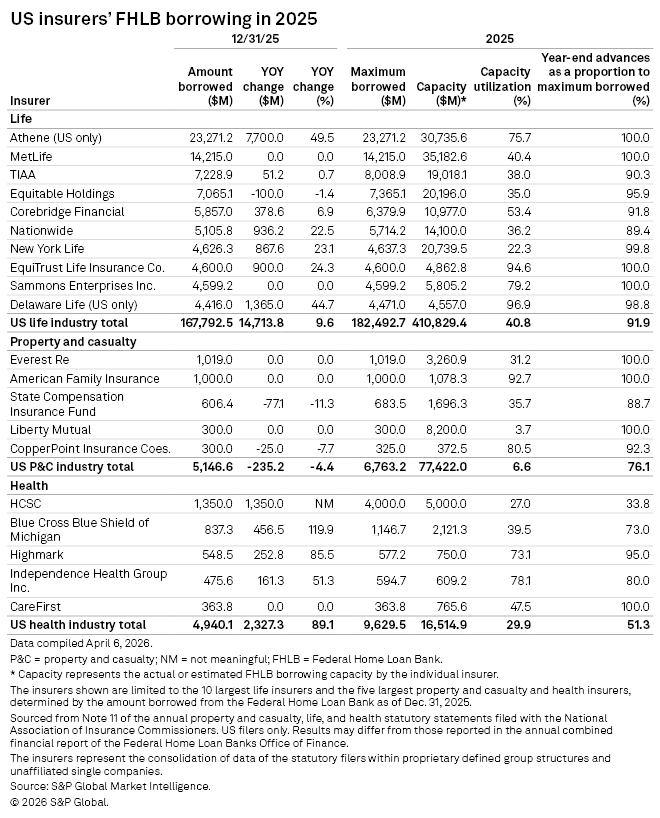

➤ Advances to US insurance companies increased by 10.4% to $177.85 billion as of Dec. 31, 2025, according to data reported by the FHLBanks Office of Finance, marking a second consecutive year and third time in four years of double-digit growth. Life insurers utilizing FHLB funding agreements in connection with spread lending strategies that pair relatively low-cost borrowings with the opportunity to reinvest proceeds in higher-yielding assets fueled the 2025 expansion. Health insurers stepping up their borrowing at a time of rising claims costs also contributed.

➤ The heightened FHLB funding agreement activity comes amid a broader surge in deposit-type contracts as life insurers and annuity writers continued to emphasize the generation of incremental yield from their general account investment portfolios. The US life industry's deposit-type contract balance before reinsurance soared net of surrenders and withdrawals by 18.3% in 2025, which represents the largest rate of expansion in at least the last 24 years. We estimate that FHLB funding agreements accounted for $130.63 billion of the $684.50 billion balance of deposit-type contracts in life insurers' general accounts as compared with $121.68 billion of the $578.49 billion at year-end 2024.

➤ Insurers maintain material capacity for increased borrowing, particularly in the property and casualty sector. A generationally strong year for underwriting profitability and, aside from the January 2025 Los Angeles wildfires, a light year for natural catastrophes contributed to a 4.4% year-over-year decline in aggregate borrowings across the sector. Our analysis finds that P&C insurers utilized only 6.6% of their available capacity, which in addition to backup liquidity and cash management may also be used in connection with spread lending.

Events in 2025 demonstrated the value of FHLB membership to US insurance companies. From a Maryland managed care company with a need for contingent liquidity to a Virginia P&C insurer seeking acquisition financing and annuity writers increasing the size of their spread lending programs, FHLBs offer an array of collateralized products that demonstrate their utility in a range of scenarios.

US insurance companies accounted for 26.3% of FHLB advances across all borrower types, including banks, thrifts and credit unions, up from 21.8% at the end of 2024 and only 10.0%, excluding captive insurers, as recently as 2016. Life insurers and fraternal benefit societies accounted for $167.79 billion, or 94.3%, of total US insurer FHLB advances, with the vast majority of that amount consisting of funding agreements used as part of spread investing programs.

The US life subsidiaries of Athene Holding Ltd. ranked second only to Truist Financial Corp. among the FHLB system's largest advance-holding borrowers at year-end 2025 with general and separate accounts advances totaling $23.27 billion. Truist held $31.50 billion in advances at that date with JPMorgan Chase & Co.'s $18.17 billion tally ranking third, followed by Wells Fargo & Co., U.S. Bancorp and MetLife, Inc. With the proposed merger of Corebridge Financial Inc. and Equitable Holdings Inc., the combined entity would have ranked as the eighth-largest FHLB borrower behind PNC Financial Services Group Inc. based on aggregate outstanding funding agreement liabilities of $12.92 billion. The number of insurance company members increased for 10 of the 11 FHLBs in 2025.

Athene utilizes FHLB advances from the Federal Home Loan Bank of Des Moines as part of a broader funding agreements business, which also includes a large funding agreement-backed notes program and funding agreement-backed repurchase agreements as well as funding agreements issued to an affiliate and third parties. Since Athene's primary US life subsidiary allocates all but $568.8 million of its FHLB funding agreements to its separate account, its 58.5% year-over-year increase in its deposit-type contracts balance was largely attributable to those other initiatives.

From a general account standpoint, two US life insurance groups posted year-over-year growth in FHLB funding agreements in excess of $1 billion: the group led by Delaware Life Insurance Co. and Tokio Marine Holdings Inc. through Reliance Standard Life Insurance Co. The Delaware Life group, which ended 2025 with $4.42 billion in FHLB funding agreements as compared with $3.05 billion at the end of 2024, also took a $50 million short-term advance that it repaid in full prior to year's end. Reliance Standard's liability for FHLB funding agreements rose to $4.00 billion from $2.45 billion year over year as its issuance and repayment volumes surged relative to 2024. Notably, the Tokio Marine subsidiary has been ceding a portion of its FHLB funding agreement liabilities to Oceanview Life & Annuity Co. on a coinsurance with funds withheld basis. Oceanview more than doubled its own FHLB funding agreement liabilities to $1.80 billion from $820 million in 2025.

New FHLB advance-takers among US life insurers included Aspida Life Insurance Co., Wilton Re Ltd.'s Texas Life Insurance Co. and United Heritage Life Insurance Co.

P&C insurers utilized FHLB borrowings for a broader array of purposes with traditional advances constituting all $5.15 billion of the sector's outstanding FHLB-related liabilities, an amount that marked a decrease of 4.4% on a year-over-year basis. The US subsidiaries of Everest Group Ltd. and American Family Mutual Insurance Co. SI remained the largest two P&C borrowers with outstanding advances of $1.02 billion and $1.00 billion, respectively, at year's end, unchanged from 2024.

New P&C sector advance-takers Odyssey Reinsurance Co., Employers Insurance Co. of Nevada, Northern Neck Insurance Co. and Midwest Family Mutual Insurance Co. demonstrated several of the rationale we have seen employed by peer companies over the years. This included liquidity management for the Fairfax Financial Holdings Limited and Employers Holdings Inc. subsidiaries, financing for Northern Neck's purchase of 49.99% of Frederick Mutual Insurance Co. and spread investing at Midwest Family Mutual.

Liquidity management was paramount in the managed care space in 2025 amid elevated medical utilization rates, contributing to an 89.1% surge in FHLB advances during the year to a tally of $4.94 billion. Health Care Service Corp. added $1.35 billion in advances in 2025, at one point borrowing as much as $4.00 billion. The groups led by Blue Cross Blue Shield of Michigan Inc. and Highmark Inc. dramatically increased their advances on a year-over-year basis to respective totals of $837.3 million and $548.5 million. Highmark said that its board approved an increase in FHLB borrowing capacity during 2025 so as to bolster business growth, ensure financial flexibility and maintain adequate liquidity.

Despite increasing membership rolls across sectors there remains considerable room for growth in advances. We counted 49 active P&C borrowers among the approximately 274 P&C groups and stand-alone entities with membership in a FHLB as of Dec. 31, 2025. Greater use of spread lending programs by P&C insurers represents one opportunity for expansion in a sector where FHLB membership primarily serves as cash management resource and source of standby liquidity. The managed care market also offers significant growth potential as there were just 13 groups and stand-alone entities with advances outstanding at year-end 2025.

All told, existing US insurance company FHLB members reported aggregate borrowing capacity of $504.76 billion as of Dec. 31, 2025, with their outstanding advances indicating a utilization rate of 35.2%.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.