Research — April 16, 2026

IBM Q1 revenue seen at $15.7B as software strength persists but growth eases

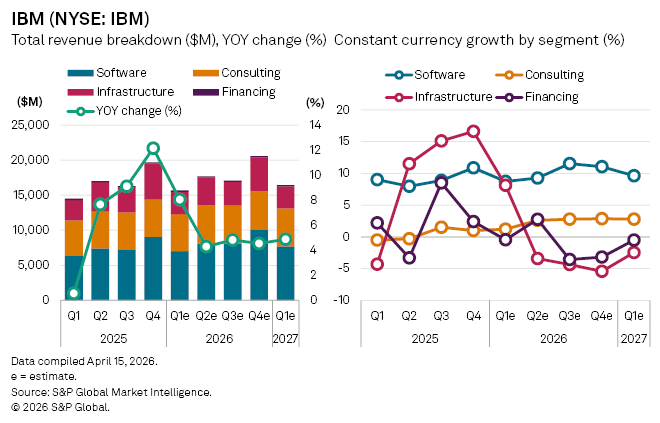

International Business Machines Corp. (NYSE: IBM) is expected to deliver a steady start to 2026, with first-quarter revenue forecast to rise 7.8% year-on-year to $15.7 billion, driven largely by continued strength in its software division. On a constant currency basis, growth is projected at 5.44%, slowing from 8.96% in the final quarter of 2025, suggesting some loss of momentum as macro headwinds and currency effects weigh.

The company’s software division remains a key engine for growth. Analysts’ consensus points to software revenues increasing 11% to $7 billion in Q1, supported by the earlier-than-expected closing of IBM’s $11 billion acquisition of Confluent Inc., a data-streaming platform central to enterprise AI deployments. The deal, completed in March rather than the anticipated second half of 2026, is expected to reinforce IBM’s push to embed real-time data capabilities into its hybrid cloud and AI stack.

Outside software, IBM’s consulting arm is expected to post growth of 4% to $5.3 billion. Infrastructure revenues are forecast to rise 9.9% to $3.2 billion in the quarter, though analysts expect this to turn negative in the second quarter as product cycle dynamics weigh on performance. Financing remains a marginal contributor, with revenues seen edging up 0.7% to $192 million.

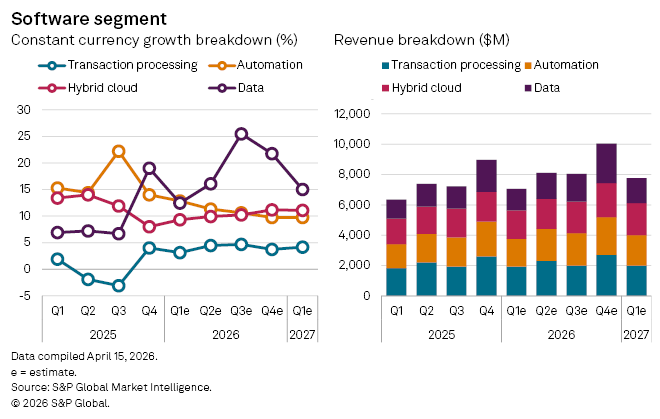

Within software, growth is expected to remain broad-based across key segments. Hybrid cloud revenue is expected to rise 12% year-on-year to $1.89 billion, reflecting continued enterprise demand for cloud-modernization tools.

Automation is projected to increase 15% to $1.82 billion, supported by workflow and AI-driven process software. Data stands out, with 14% growth to $1.4 billion, as enterprises scale data platforms to support AI deployments. Transaction processing remains more mature but stable, growing 5% to $1.92 billion.

Constant-currency growth estimates suggest slightly softer momentum, with overall software growth of ~8.7%, indicating some FX tailwinds.

IBM’s shares are currently down about 21% year-to-date, reflecting the wider technology sell-off. The company is scheduled to report earnings on Wednesday, April 22.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment