ECONOMICS COMMENTARY — 02 Apr, 2026

Global PMI shows European manufacturing taking heavy toll from Middle East war

Global manufacturing PMI survey data illustrate the varying degrees to which the economic impact of the war in the Middle East has spread worldwide, with production typically hit hardest in various European economies geographically closest to the war and those Asian economies that have a high dependency on supply lines through the Strait of Hormuz. However, the greatest overall impact on supply chains and input costs so far has clearly been in Europe.

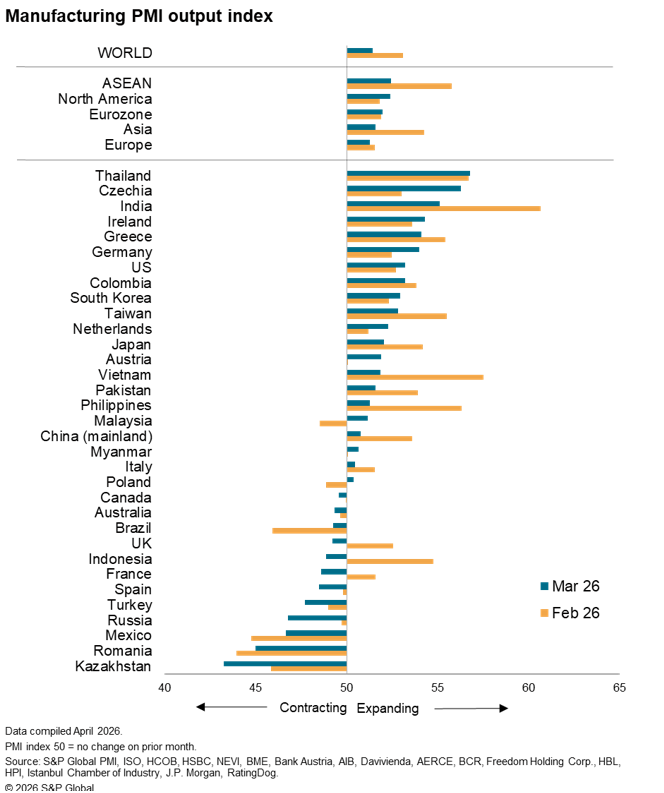

Manufacturing output trends worsen in 19 out of 33 economies

The headline global manufacturing Purchasing Managers’ Index (PMI), sponsored by J.P. Morgan and compiled by S&P Global Market Intelligence, fell from 51.8 in February to 51.3 in March.

The deterioration of the PMI was fuelled by factory output trends worsening in 19 of the 33 economies covered by the S&P Global manufacturing surveys, with outright falls in production recorded in 12 economies. However, it should be noted that manufacturing-specific PMI data are not available for the Middle East and North African economies, as these are covered by S&P Global ‘whole economy’ PMI surveys.

The steepest downturns were seen in Kazakhstan, Romania, Mexico, Russia and Turkey. However, when compared to February, performances worsened most significantly in Indonesia, Vietnam, India and the Philippines.

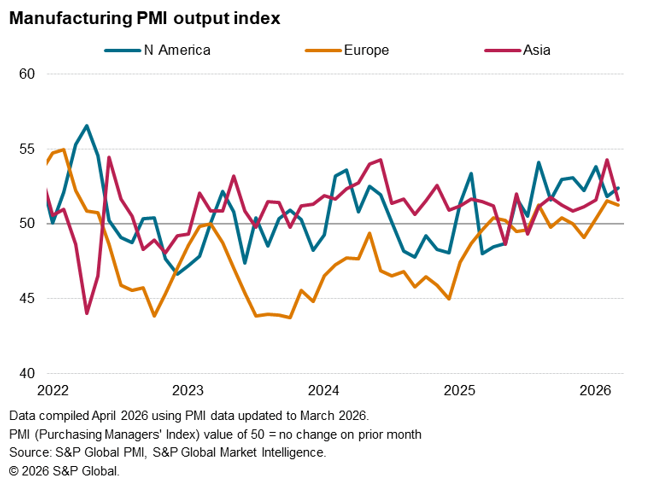

Output growth in fact weakened especially sharply across Asia, particularly in the ASEAN region, though Europe saw the weakest expansion overall. North America as a whole meanwhile saw growth tick higher.

Growth in Europe and America was mixed, however. Expansions in Germany, the Netherlands, Austria and Greece, for example, offset downturns in the UK, France and Spain, as well as the reductions seen over much of eastern Europe. Concurrently, US manufacturing growth accelerated to record a robust expansion that was the sixth strongest of all countries surveyed, offsetting contractions in Canada and Mexico.

Europe sees biggest supply shock

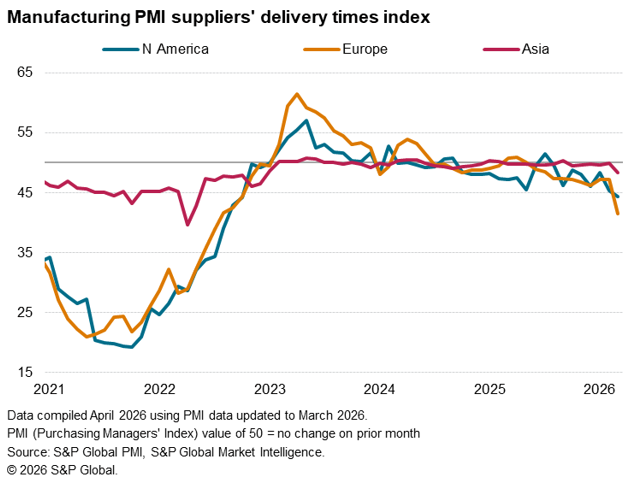

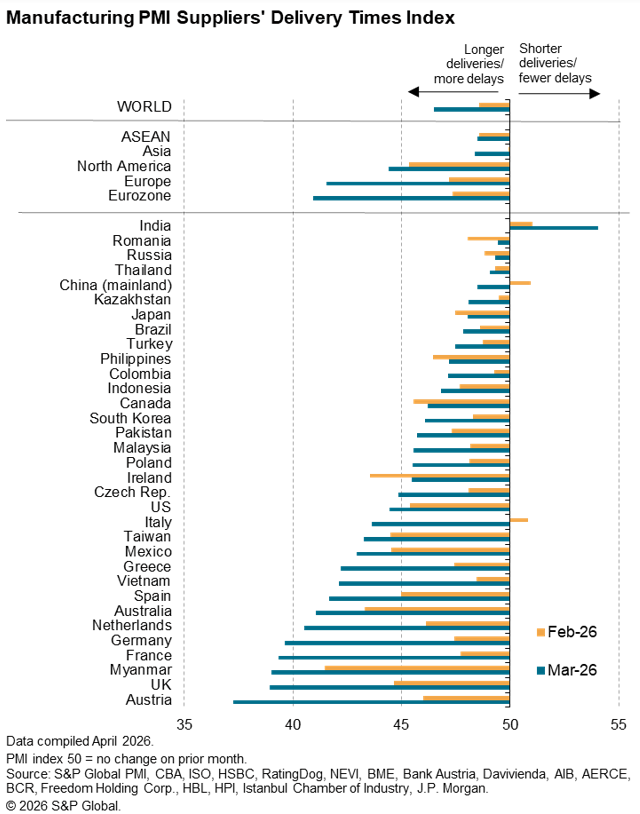

Europe’s underperformance was linked in part to the region also seeing the most severe supply shock from the war so far. As measured by the PMI’s Suppliers’ Delivery Times Index, supply chain delays in Europe and the eurozone spiked in March to the highest since July 2022 and August 2022 respectively, led by a worsening supply situation in Austria, followed by France, Germany and the Netherlands. However, the UK also reported especially severe supply delays, with delivery times lengthening to a degree not seen since July 2022.

Supply chain pressure was nonetheless also widely reported across North America, with the war in the Middle East exacerbating supply delays arising from US tariffs to lead to the longest lengthening of lead times since October 2022.

By comparison to Europe and North America, supply delays in Asia were relatively mild, though notably still rose to the highest since December 2022.

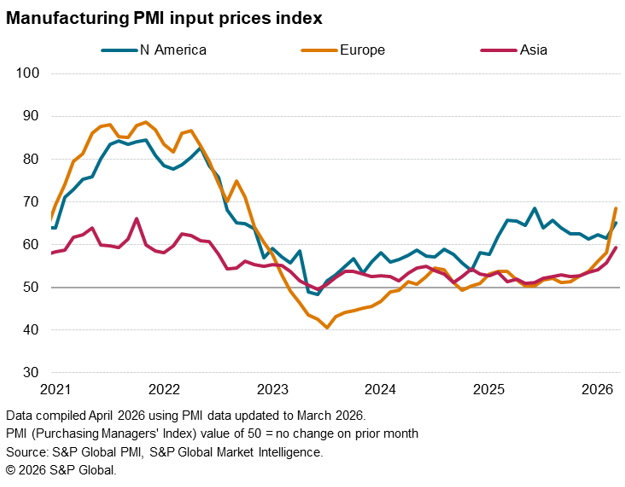

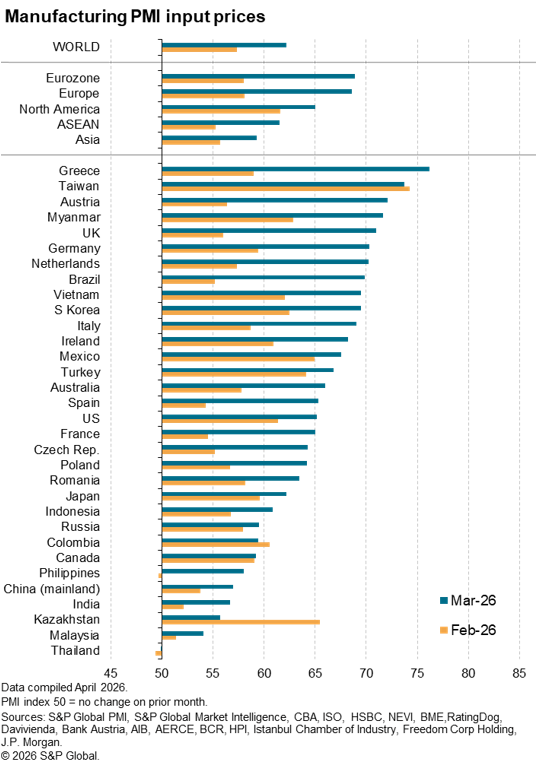

Price surge led by Europe

With supply delays typically being accompanied by rising prices, Europe also reported especially steep input cost inflation in March. Eurozone input costs rose at the sharpest rate since June 2022, led by Greece, while UK prices jumped at a rate not seen since October 2022. The increase in the rate of inflation in the UK was the largest recorded since sterling was ejected from the ERM in 1992, while the acceleration in the eurozone was the steepest since comparable data were first available in 1997.

Input prices also rose at a markedly increased rate in the US, as higher energy prices compounded the impact of US tariffs to cause the strongest upturn in costs since last August, while prices rose across Asia at a rate not seen since June 2022.

Access the latest global PMI press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings