ECONOMICS COMMENTARY — 09 Apr, 2026

Global PMI highlights stagflation risks as output growth slumps amid surge in prices

March’s PMI surveys produced by S&P Global provided the first indication of changing economic conditions since the outbreak of war in the Middle East, and signalled an unwelcome combination of markedly slower growth and accelerating inflation.

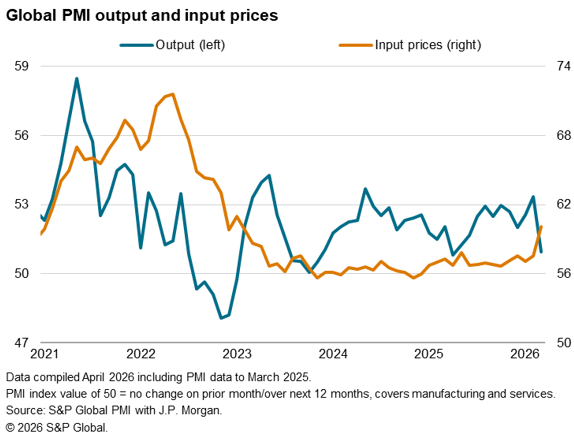

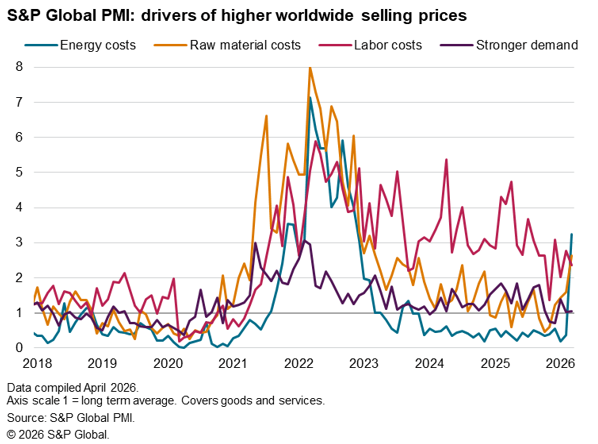

Output growth moderated worldwide to one of the greatest extents seen since the global financial crisis of 2008-9, cooling to its weakest since last April. Firms’ input costs meanwhile rose sharply for both goods and services thanks principally to surging energy and other raw material costs, rising globally at the fastest rate since January 2023.

The data therefore signal a worrying trend toward ‘stagflation’, presenting policymakers with a challenge in seeking to support economic growth and employment while curbing any signs of persistent inflation.

Global PMI slumps lower on outbreak of war

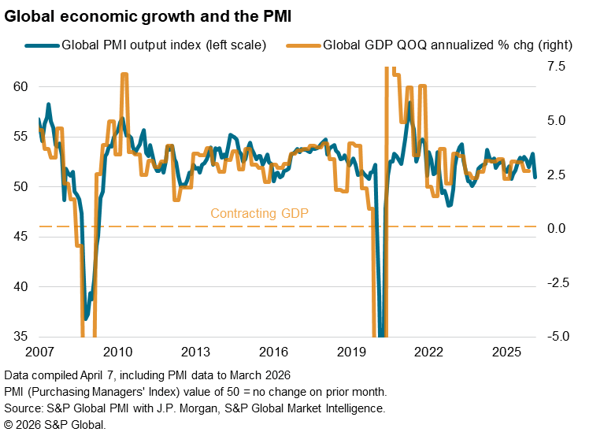

Global economic growth slumped in March following the outbreak of war in the Middle East. The J.P.Morgan Global Composite PMI Output Index, compiled by S&P Global, fell from February’s 21-month high of 53.3 to 51.0 in March, the lowest since last April (when the US announced far-reaching tariffs) and second-lowest since 2023.

The 2.4-point drop in the global output index was the largest since July 2022. Barring the pandemic, the drop was the largest since November 2008, underscoring the scale of the initial economic impact from the conflict in the Middle East.

The survey data therefore suggest that global economic growth has already taken a material negative hit from the outbreak of war in the Middle East on 28 February, which has derailed gathering upturn seen in the lead up to the conflict. The lower PMI reading signals a deceleration of global economic growth from 3.0% in February to an annualized quarterly rate of 2.0% in March.

Broad-based deterioration of growth

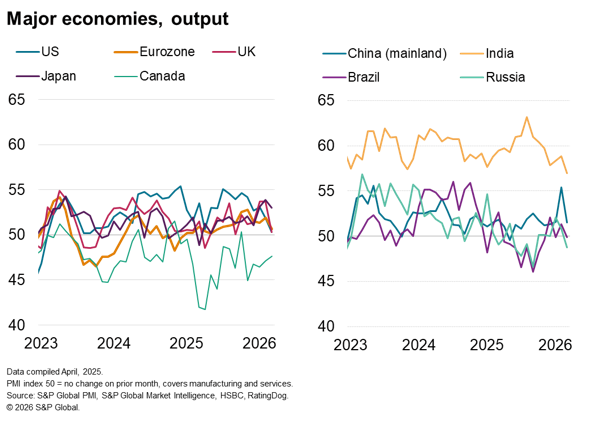

Growth rates slowed across the board among the major economies. Downturns were seen in both Canada and Australia while activity came close to stalling in the US, UK and eurozone. That left Japan as the best-performing advanced economy, though even here growth softened. In the major emerging markets, slower growth rates in India and mainland China were accompanied by downturns in Russia and Brazil.

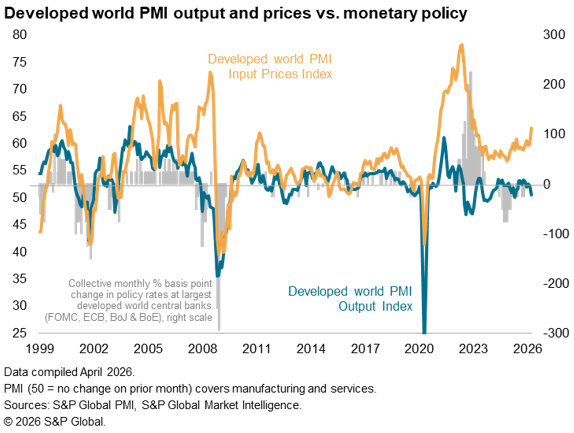

Inflation spikes higher

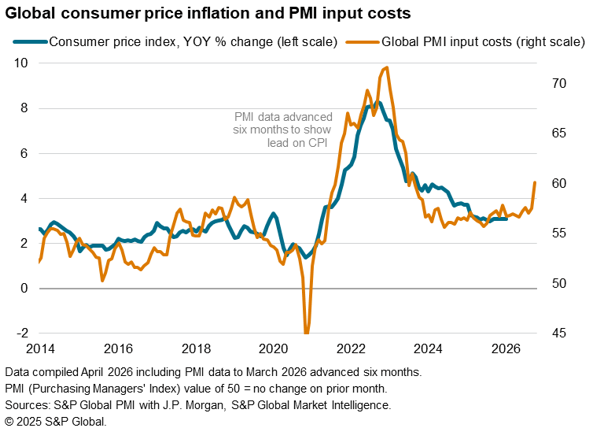

Measured across both goods and services, average input prices meanwhile rose worldwide in March at the fastest pace since January 2023. This points to global consumer price inflation accelerating close to 5% in the coming months, up from 3.1% in January.

Average prices charged for goods and services also rose sharply as companies started to pass through the higher costs – notably for energy – on to customers, with the rate of inflation at a three-year high.

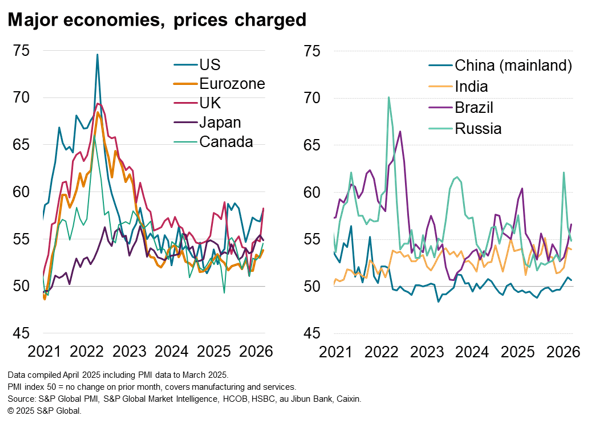

An especially steep jump in prices was recorded in the UK, where the overall rate of selling price increase rose to the highest since June 2023. US price growth also remained steep, accelerating to a seven-month high, while a 13-month high was seen in Brazil and a 31-month high reported In Australia. Inflation across the eurozone remained relatively muted but nonetheless prices rose at a rate not seen since February 2024, led by Spain and Italy.

In Asia, selling in prices across mainland China meanwhile rose only modestly, but the rise was notable in being the third monthly increase in a row after 13 months of decline. Although Japan’s selling price inflation cooled slightly, it remained among the highest recorded by the PMI.

Business optimism slumps

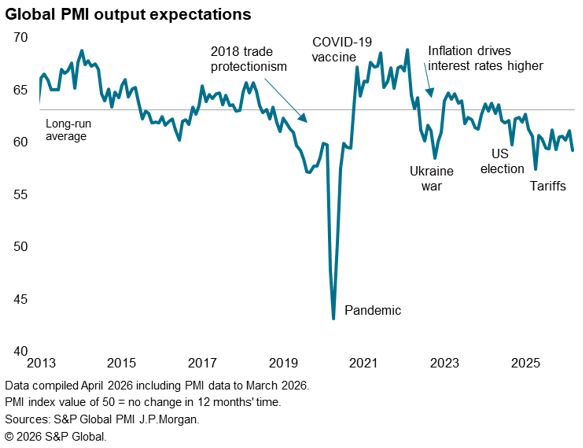

The war also hit business growth expectations, reflecting the direct effect on confidence via heightened uncertainty but also reflecting the demand-sapping impact of higher prices. New orders rose globally at the slowest rate since November 2023, helping pull global output expectations for the year ahead to the lowest since October 2022 barring only the drop seen in response to the US tariff announcements in April 2025.

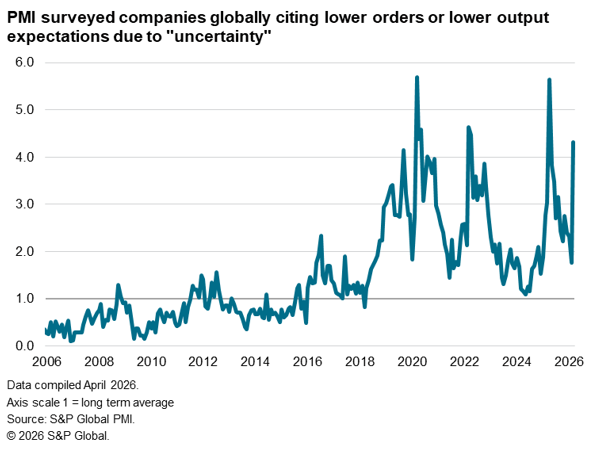

Reports of ‘uncertainty’ having adversely affected business order books and growth expectations for the year ahead have spiked to one of the highest levels seen over more than two decades of comparable survey history. Only the COVID-19 lockdowns and the April 2025 US tariff announcements have seen higher levels of damaging business uncertainty than reported in March since data were first available in 2005.

Policy outlook

The combination of slowing economic growth and rising prices raises the spectre of ‘stagflation’, which presents a challenge to policymakers, most notably in the developed world. Whereas rising inflation calls for higher interest rates, any increase in borrowing costs threatens to tip stalling economies into deeper slowdowns, or even deeper downturns.

Access the press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings