Research — April 28, 2026

Ford heads into Q1 with modest revenue growth and deepening EV losses

By Nitin Mirajkar

Ford Motor Co. (NYSE: F) is set to report first-quarter 2026 earnings on April 29, with Visible Alpha consensus estimates pointing to modest revenue growth alongside flat volumes and a sharp pullback in electric vehicles.

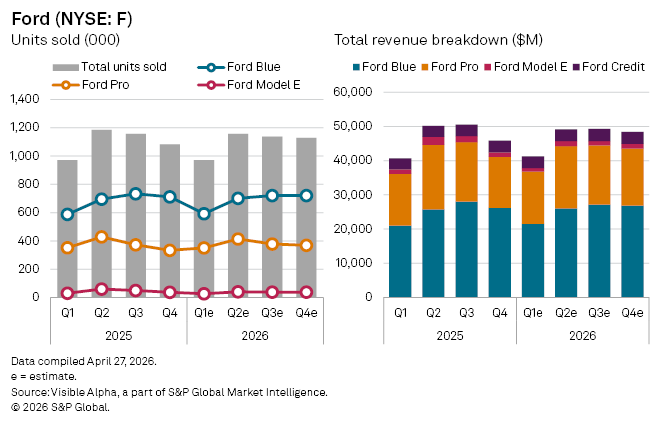

Consensus expectations show automotive revenue to rise 2.3% year-on-year to $38.3 billion in Q1, even as unit sales are expected to hold broadly flat at around 972,000 vehicles. The muted growth reflects a wider cooling in the US auto market, where high borrowing costs and elevated vehicle prices continue to constrain demand.

Within Ford’s divisional structure, the contrast is increasingly stark. The traditional internal combustion business, Ford Blue, is expected to deliver ~593,000 units, with revenue edging up 2.2% to $21.5 billion. Segment operating income is expected to climb sharply to $493 million from $96 million a year earlier, helped by easing supply chain constraints following disruption from the 2025 fire at the Novelis aluminum plant, which significantly disrupted production, along with a stronger focus on high-margin products, and reduced manufacturing costs.

Ford Pro, the group’s commercial vehicle arm and a key profit driver, is forecast to generate $15.4 billion in revenue, up 1.1%. However, operating profit is seen slipping marginally to $1.3 bn, down 1% from the prior year, indicating some normalization after a period of strong post-pandemic demand.

By contrast, the electric vehicle unit, Model e, continues to retrench. Analysts expect volumes to fall 12% year-on-year to just 27,000 units, with revenue dropping 19% to roughly $1 billion. Operating loss is also projected to widen sharply by 14% to $968 million. The decline mirrors a broader reversal in US EV demand following the expiry of federal tax credits and high price points, which have pushed many consumers back towards cheaper combustion and hybrid models. Ford is already recalibrating its EV strategy, scaling back investment and shifting focus towards more profitable segments.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment