Research — March 12, 2026

Maersk faces a tougher 2026 as container overcapacity pressures freight rates

By Yash Gupta

Danish shipping group A.P. Møller - Mærsk A/S (CPH: MAERSK-B) is expected to face a challenging 2026 as the container shipping market swings from the tight conditions of recent years toward structural overcapacity.

Analysts expect that a gradual reopening of Red Sea routes, which would allow vessels to resume shorter transits via the Suez Canal, could release a significant amount of effective capacity back into the global fleet. During the crisis, ships were forced to detour around the Cape of Good Hope, absorbing supply and pushing up freight rates. A return to normal routes would reverse that effect, intensifying competition among carriers.

At the same time, the industry is contending with a wave of new vessel deliveries and softer demand growth.

Against this backdrop, analysts expect revenue to decline 7.2% year-on-year to about $50.1 billion in 2026, reflecting a sharp slowdown in Maersk’s core container shipping business.

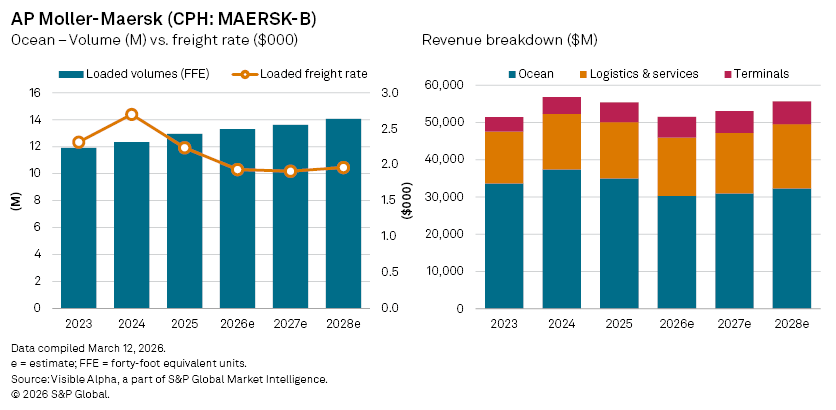

The pressure is most visible in the company’s Ocean segment, which accounts for the bulk of group earnings. Ocean revenue is projected to fall 13.4% to $30.3 billion, as freight rates retreat from the elevated levels seen during recent supply chain disruptions.

Segment profitability is expected to deteriorate even more sharply. Ocean EBITDA is forecast to plunge nearly 60% to $2.6 billion, highlighting the operational leverage of container shipping when freight prices weaken.

Operational metrics underline the imbalance emerging in the market. Analysts expect loaded volumes in the Ocean division to rise modestly by 2.7% to 13.29 million forty-foot equivalent units (FFE) in 2026, suggesting demand growth remains positive but subdued. However, the average loaded freight rate is projected to fall 13.7% to $1,932, reflecting the growing gap between available capacity and cargo demand.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment