Research — March 18, 2026

K Line faces softer 2026 as freight rates and bulk markets retreat

By Aman Gupta

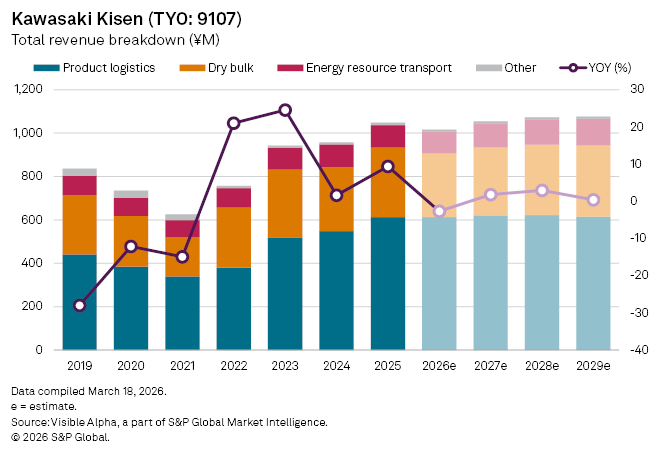

Japanese shipping company, Kawasaki Kisen Kaisha Ltd. (TYO: 9107), also known as K Line is bracing for a modest top-line contraction in fiscal 2026, with revenues forecast to fall 2.7% year-on-year to around JP¥1 billion, as cyclical pressures weigh on key shipping segments after the post-pandemic boom.

The weakness is most evident in product logistics, where revenues are expected to remain broadly flat, rising just 0.1% to JP¥613 million in 2026. Analysts point to a normalization in container freight rates, which have retreated sharply from their pandemic-era highs, alongside softer demand in finished vehicle transport.

In dry bulk, conditions appear more challenging. Revenues are projected to decline 9% to JP¥293 million, reflecting subdued commodity demand, particularly from China, and an oversupplied vessel market that continues to pressure charter rates. The imbalance between fleet growth and cargo volumes has kept earnings under strain across the sector.

Energy resource transport, a relatively more stable earnings pillar for K Line, is expected to see a milder 1.4% decline to JP¥100 million, improving from a 4% drop in 2025. Long-term contracts in liquefied natural gas and tanker shipping have helped cushion volatility, even as spot markets remain uneven.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment