Research — March 9, 2026

Dow Jones Industrial Average Monitor update – A look at 30 US large-caps

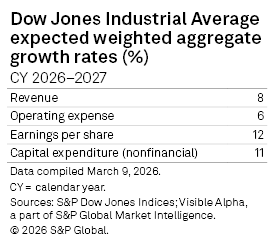

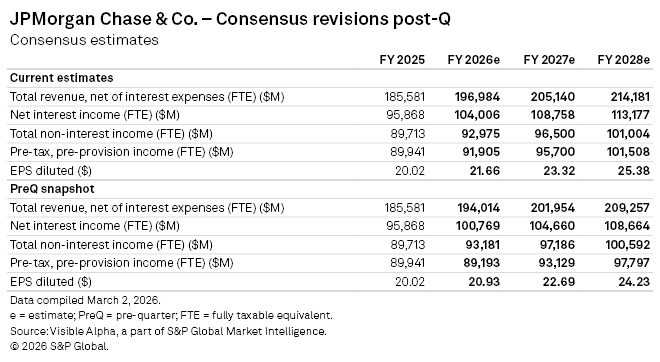

Looking at the direction of Visible Alpha consensus, post-earnings season of the thirty companies in the Dow Jones Industrial Average (DJIA), the data points to the potential for further surprises. The macroeconomic and sector-specific issues vary significantly. Despite increased complexity around geopolitics, tariffs and trade, markets, until recently, have been reaching new highs. Even with a fragile macro backdrop through 2025 and into 2026, companies seem to be navigating the challenges. While the full impact of the Middle East tensions on trade and the global macro environment remains an open question, many companies currently show a relatively stable annual earnings outlook, which may or may not be the case going into the second half of the year.

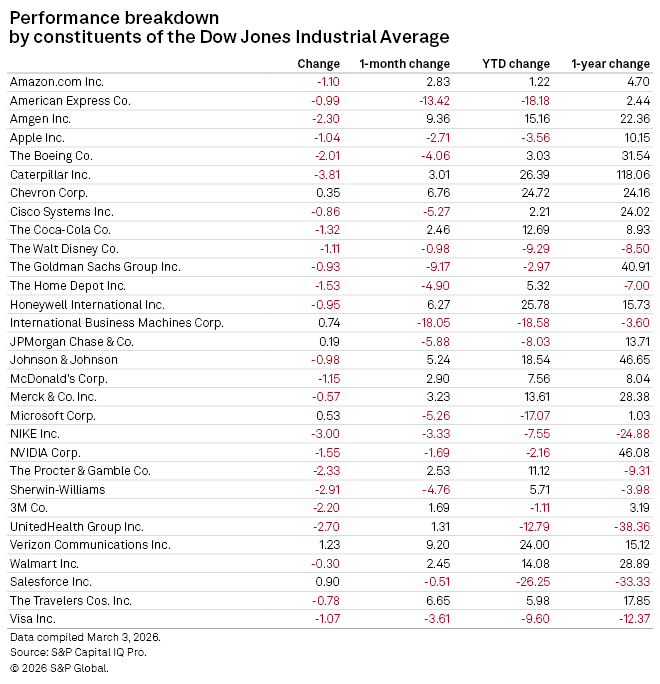

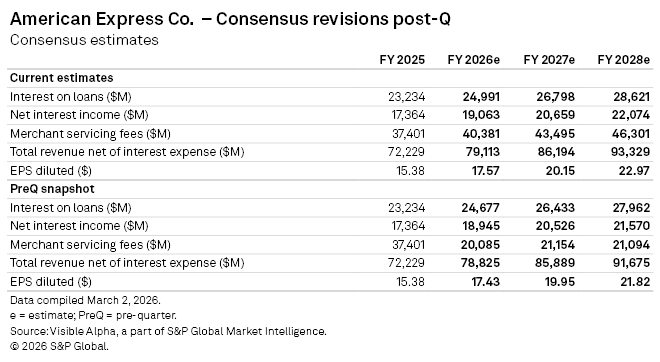

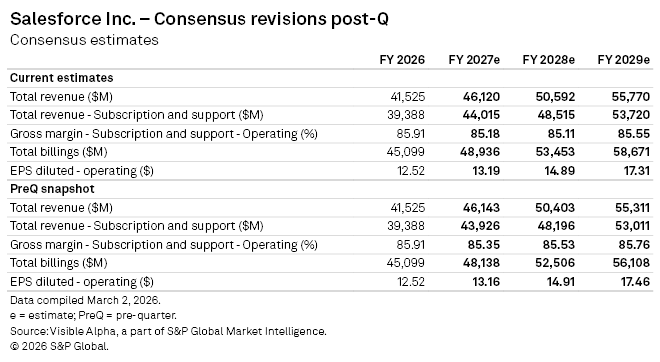

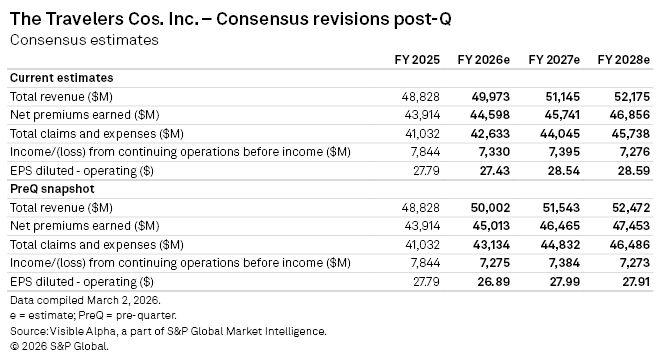

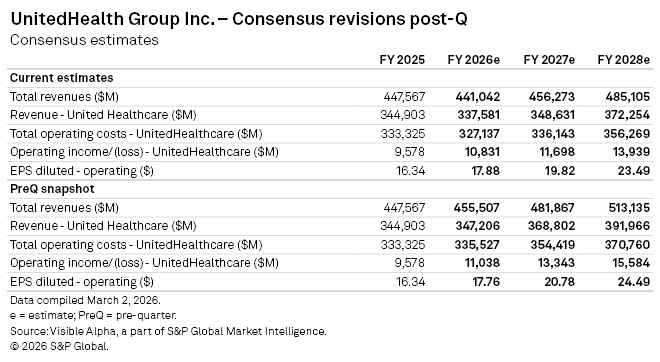

UnitedHealth Group Inc. remains a drag on the DJIA year-to-date and is the worst performer in the index in the past 12 months, due to the tragedy involving its former CEO and the downward revisions, especially to its profitability. However, a close second is Salesforce, which has seen its performance deteriorate -26% year-to-date, outpacing United Health’s -12%.

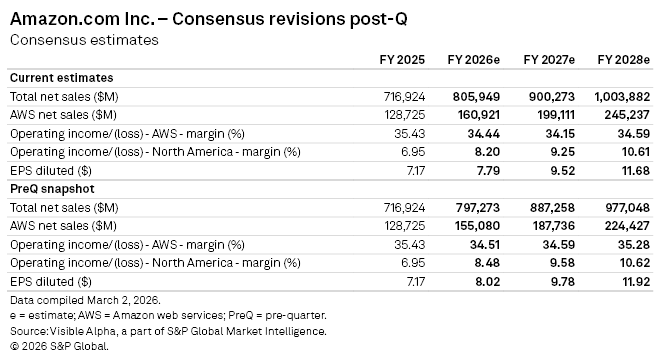

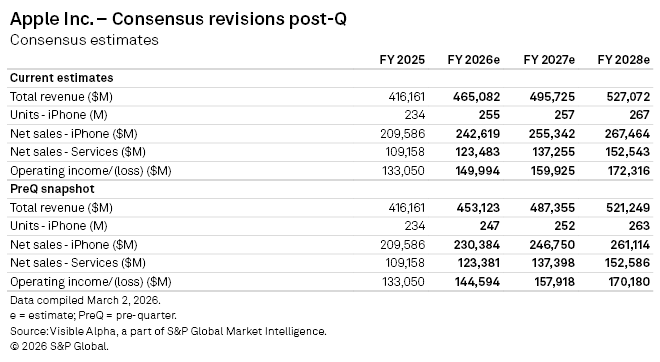

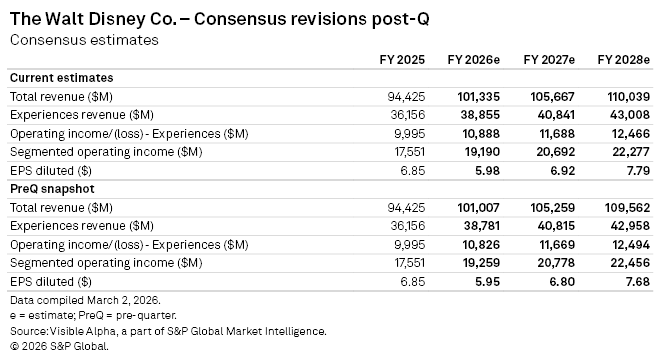

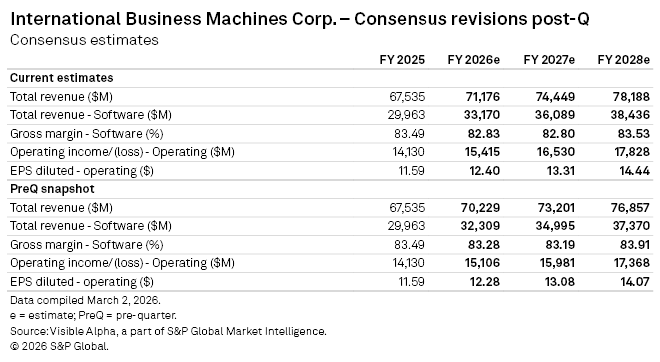

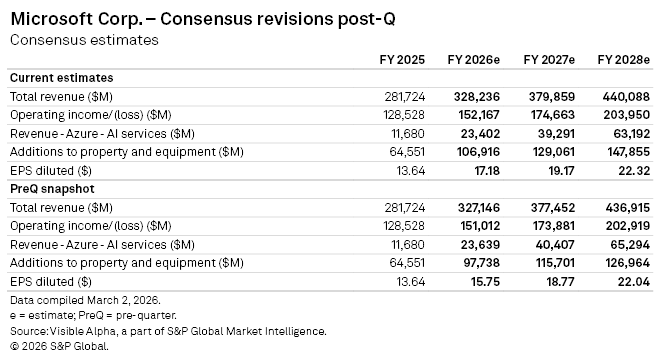

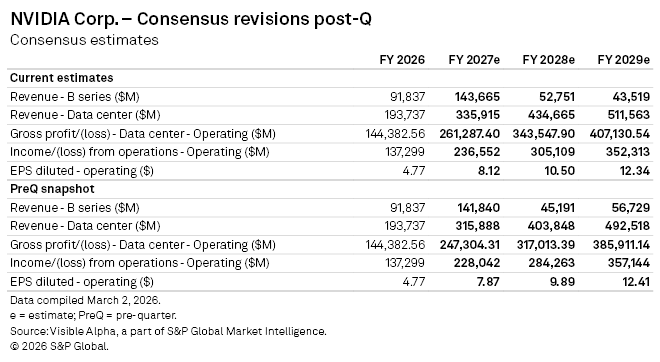

The technology sector has been a drag on the index so far year. In addition to the weakness at Salesforce Inc., Apple Inc., Amazon.com Inc., International Business Machines Corp., and Microsoft Corp. have also weighed on the DJIA, due to concerns about the outlook for AI. The increasing levels of CapEx for AI investment by many technology companies have not yet seen equal increases in revenues or returns. In addition, software company subscription business models have been called into question as AI starts to advance and gain greater adoption. Even though CapEx for AI infrastructure continues to increase substantially this year this year, CapEx beneficiary, NVIDIA Corp., also has been underperforming year-to-date around concerns that CapEx levels may have to come down, and profit expectations are becoming too high for the company to exceed this year and next. Amazon, too, has seen its margin and EPS expectations decline post-Q.

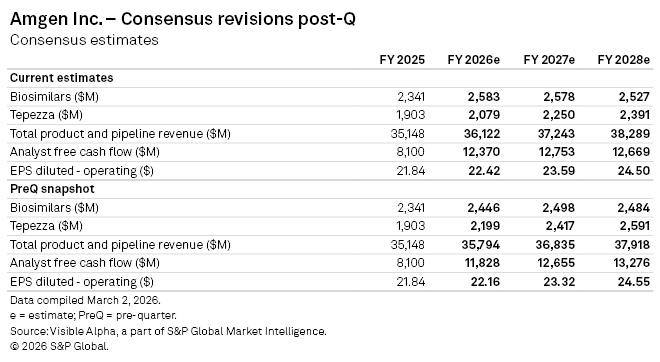

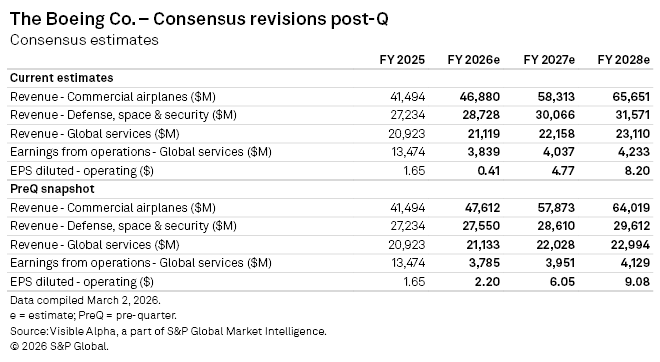

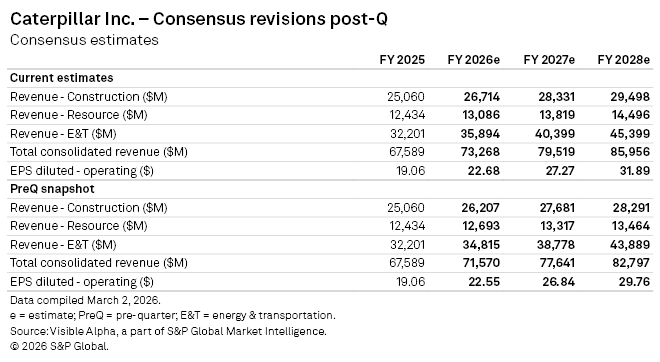

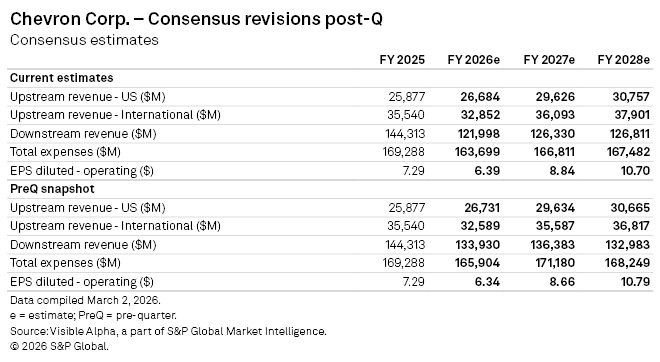

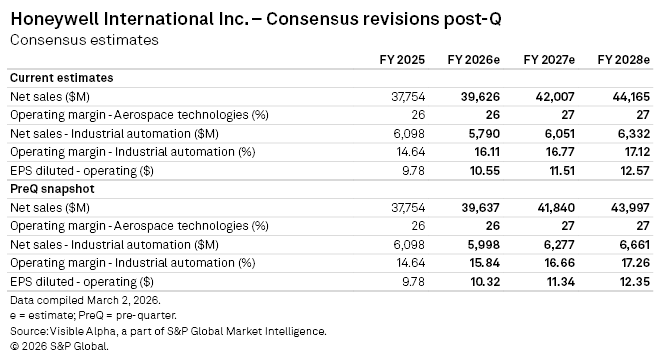

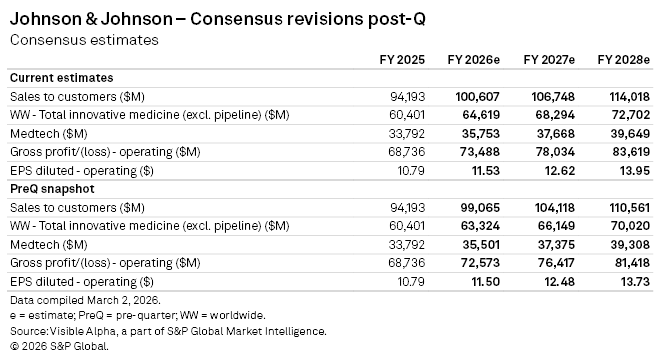

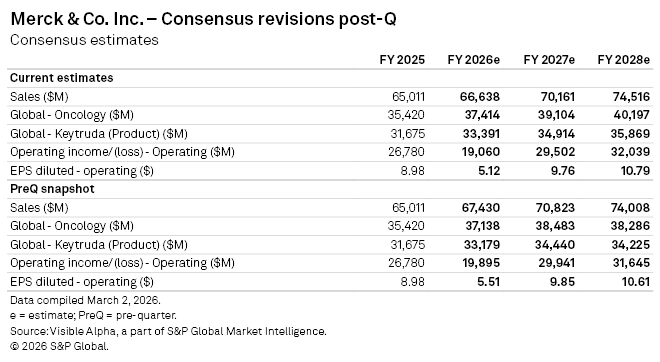

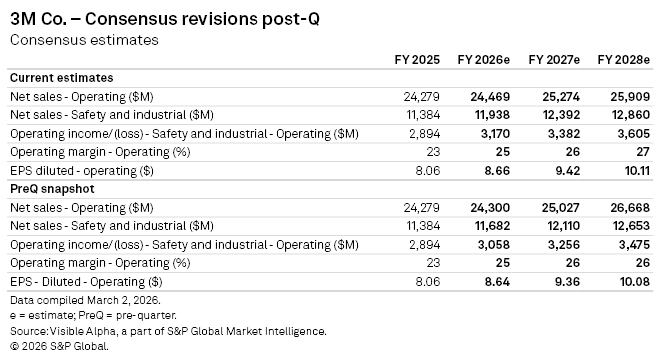

While technology has been underperforming, industrial and energy companies, Caterpillar Inc., Honeywell International Inc., and Chevron Corp., have been notable outperformers year-to-date on upward revisions to consensus. The Boeing Co., too, has shown strength in tandem with the industrials theme as the company’s backlog exceeded expectations. Healthcare companies Johnson & Johnson, Amgen Inc., and Merck & Co. Inc. have collectively driven increases in the index year-to-date, due to increases to consensus. There appears to be a rotation happening supported by more optimistic expectations in non-technology areas of the market.

As the market moves further into 2026, a prolonged increase in energy prices, due to the conflict in the Middle East, may lead to lower growth and higher prices. While S&P Global Market Intelligence projects no cuts in the first half and for rate cuts to resume in the second half of 2026, the sustained level of energy prices may be a key factor. With both the US dollar and oil spiking on the back of the Middle East situation, inflation may be a trickier issue this year for the new Fed Chair. The outlook for the second half may support a broader set of sectors, depending on the severity and sustainability of the Middle East conflict on the macro backdrop.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings