Research — April 1, 2026

Deere looks to construction and compact equipment for 2026 rebound

By Manali Baua

Analysts expect Deere & Co. (NYSE: DE) to return to modest growth in 2026, with strength in construction and smaller-scale agricultural equipment helping offset continued weakness in large farm machinery.

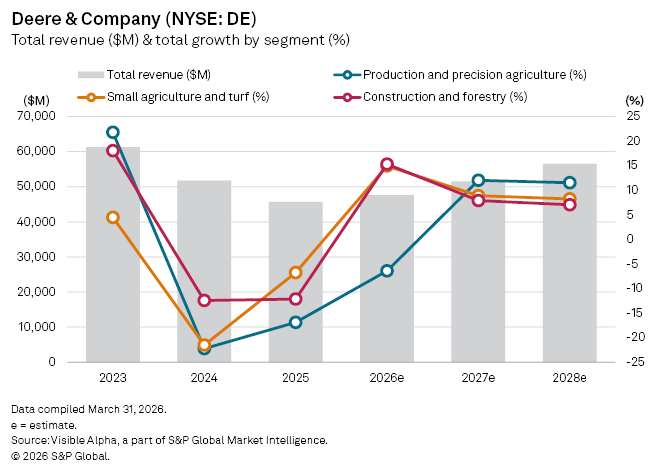

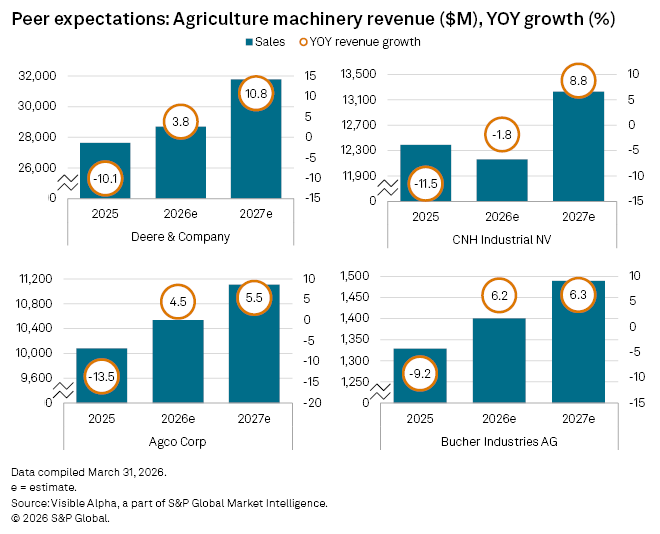

Visible Alpha consensus points to group revenue rising about 4% to $47.6 billion, marking a tentative recovery after two consecutive years of decline. The improvement reflects a shift in demand rather than a broad-based upturn in the farm economy, which remains under pressure from low crop prices, high input costs, and elevated borrowing rates.

Within Deere’s portfolio, the small agriculture and turf division, which includes compact tractors, turf equipment and dairy and livestock machinery, is expected to grow 14.9% year-on-year to $11.7 billion in 2026, reversing a 7% decline in 2025.

A similar recovery is forecast in construction and forestry, where revenues are expected to rise 15.2% to $13.1 billion after a 12% fall last year, supported by infrastructure spending and a rebound in equipment utilization. Deere itself has highlighted improving demand in both segments, with first-quarter sales up 13% year-on-year and management signaling that 2026 could represent the trough of the current cycle.

By contrast, the production and precision agriculture division, Deere’s largest unit, is expected to remain a drag, with sales falling a further 6% to $16.2 billion, albeit a smaller decline than the 17% contraction seen in 2025. Large-scale farmers continue to defer purchases of high-value machinery amid squeezed incomes and uncertain trade dynamics.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment