Research — February 12, 2026

Panasonic to see fiscal 2026 revenue slide amid restructuring efforts

By Cristalina Pinto

Panasonic (TSE: 6752) shares have risen 17% since the Japanese electronics group delivered a somewhat better-than-expected set of third-quarter fiscal 2026 results on Wednesday, February 4, offering a bright spot in what remains a difficult year for the industrial conglomerate.

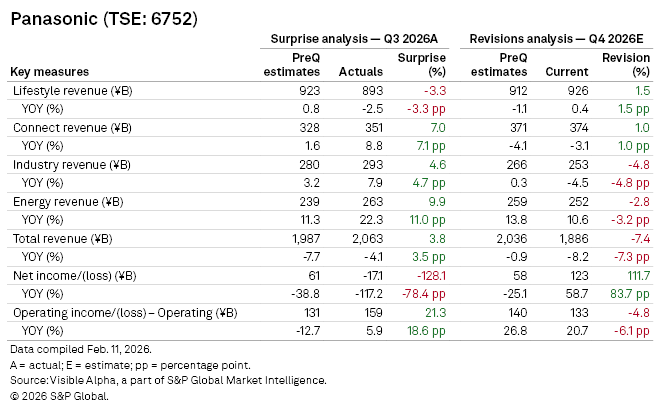

Operating income came in at JP¥159 billion, comfortably ahead of Visible Alpha pre-quarter estimates of JP¥131 billion. Revenue fell 4.1% year-on-year to JP¥2.1 trillion, but still topped the JP¥1.9 trillion analysts had penciled in. Net income, however, fell short of analyst expectations with the company reporting a net loss of JP¥17.1 billion in Q3, compared with expectations for a modest profit of JP¥61 million.

Operating income came in at JP¥159 billion, comfortably ahead of Visible Alpha pre-quarter estimates of JP¥131 billion. Revenue fell 4.1% year-on-year to JP¥2.1 trillion, but still topped the JP¥1.9 trillion analysts had penciled in. Net income, however, fell short of analyst expectations with the company reporting a net loss of JP¥17.1 billion in Q3, compared with expectations for a modest profit of JP¥61 million.

Segment performance was broadly encouraging. Lifestyle, which includes the company’s home appliances and consumer-facing products, was the only unit to miss expectations, falling short by 3.3%. By contrast, Connect, Industry and Energy all exceeded consensus forecasts, beating estimates by 7.0%, 4.6%, and 9.9% respectively. The Energy outperformance is notable given Panasonic’s heavy exposure to electric vehicle batteries, an area facing slowing momentum as global EV adoption cools.

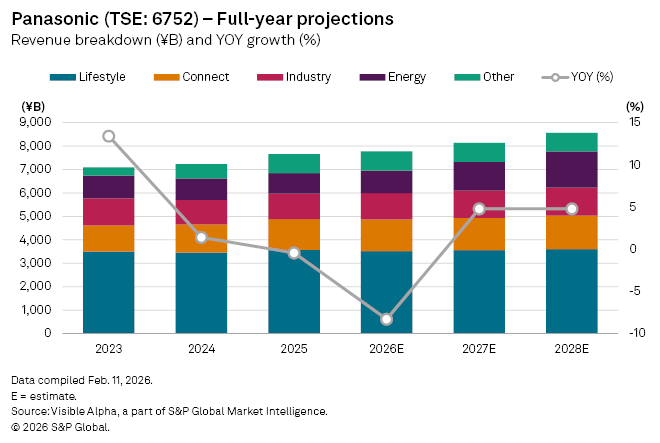

Despite the better-than-expected quarterly results, full year projections still look bleak. Consensus projections point to a challenging full year, with fiscal 2026 revenue expected to decline 8.3% to JP¥7.8 trillion, following a modest 0.5% drop in 2025. Net income is forecast to fall 31% to JP¥254 billion.

The downturn highlights the structural challenges Panasonic continues to navigate: a softer EV market weighing on its battery business, the deconsolidation of Panasonic Automotive Systems, weaker volumes in key overseas markets, and the added uncertainty of US tariffs. The group is also in the midst of restructuring efforts, which may support profitability longer term but are weighing on results today.

Analysts, however, increasingly see fiscal 2026 as the low point of the cycle. A recovery is expected in 2027, with revenue projected to grow 4.8% to JP¥8.1 trillion and net income forecast to rebound sharply, rising 72% to JP¥446 billion.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment