Research — February 25, 2026

Nissan 2026 forecasts show broad declines as sales and profits slip

By Hardik Savla

Nissan Motor Co. Ltd. (TSE: 7201) is navigating a challenging year as it grapples with falling sales and rising costs. The Japanese carmaker recently reported its third-quarter earnings with revenues falling 5.1% year-on-year to JP¥3 trillion, while operating income fell 43.6% to JP¥17.5 billion.

The decline reflects a broad slowdown in global retail and wholesale unit sales, particularly in Asia and Europe, where Chinese competitors have eroded Nissan’s market share. At the same time, the company is undertaking a major restructuring plan to cut costs and restore profitability. Heavy investment in electric vehicles (EVs) has also pushed up operating expenses in the short term.

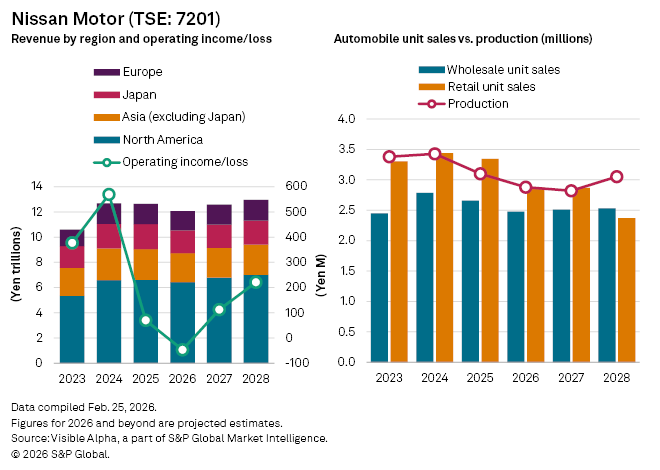

Visible Alpha consensus shows analysts expect full-year revenues to decline 4.6% year-on-year to JP¥12 trillion in fiscal 2026, following a modest 0.4% drop in 2025. North America, Nissan’s largest market, is projected to generate JP¥6.4 trillion in revenue, down 2.6%, reflecting softer demand and the impact of tariffs.

Elsewhere, the outlook is more subdued. Revenues in Asia excluding Japan are forecast to fall 6.9% to JP¥2.3 trillion. Domestic sales are expected to decline 7.7% to JP¥1.8 trillion, while Europe is seen dropping 5.1% to JP¥1.5 trillion.

Volume metrics tell a similar story. Retail unit sales, reflecting cars sold to end customers, are projected to drop 14% year-on-year to 2.9 million in fiscal 2026. Wholesale volumes or cars shipped to dealerships, are projected to fall 7% to 2.5 million units, while production is forecast to decline 5% to 2.9 million vehicles.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment