Research — February 20, 2026

Microsoft and Meta earnings review and outlook

By Melissa Otto, CFA

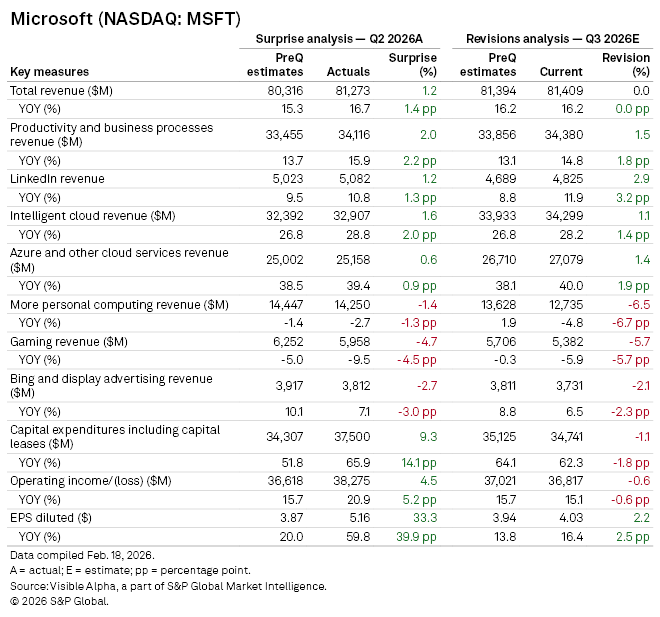

Microsoft (NASDAQ: MSFT) reported its second quarter fiscal 2026 earnings on Wednesday, January 28, delivering a beat on both revenue and profit versus Visible Alpha consensus expectations.

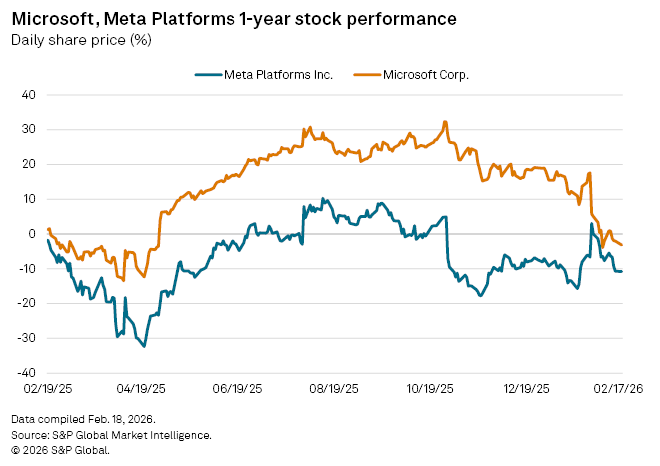

The company’s shares, however, have since fallen nearly 18%, amid concerns around signs that AI may disrupt the present software business models. In addition, the scale of Microsoft’s AI-related capex has increased to a projected $106.9 billion for FY 2026

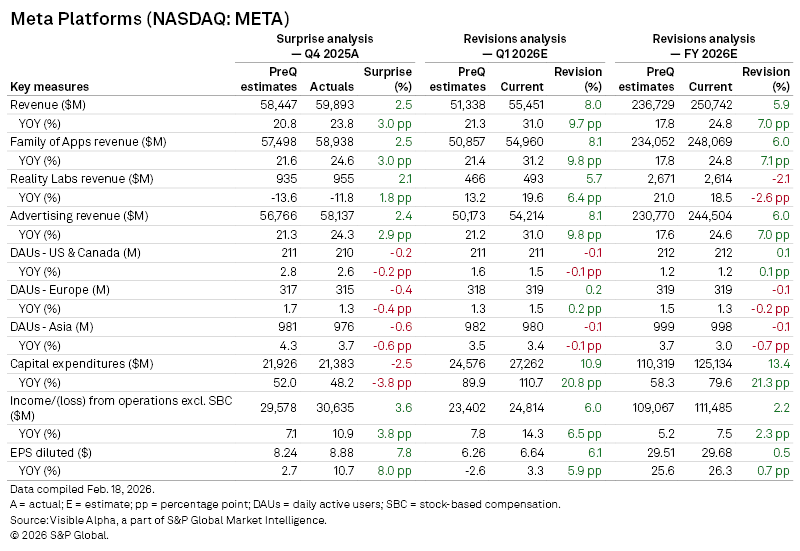

Meta Platforms (NASDAQ: META) reported its fourth-quarter fiscal 2025 earnings on the same day, also surpassing consensus expectations. While the company’s stock jumped in after-hours trading after the earnings release, Meta shares have since traded lower.

Microsoft: Q2 2025 review and outlook

Microsoft posted revenue of $81.3 billion in Q2, up 16.7% year-on-year, slowing slightly from 18.4% growth in Q1, but still ahead of consensus expectations of $80.3 billion.

Earnings also came in well above expectations, with diluted EPS of $5.16, topping the $3.87 analysts had anticipated, due to the $10 billion gain from OpenAI.

Microsoft’s Productivity and Business Processes segment, which includes revenue from Microsoft 365 Commercial, and Consumer Cloud, generated $34.1 billion in revenue, exceeding consensus forecasts of $33.5 billion.

Meanwhile, Intelligent Cloud, home to Azure and server products, delivered revenue of $32.9 billion, ahead of estimates of $32.4 billion.

Microsoft’s investment cycle remains a central focus for investors. Capital expenditure surged to $37.5 billion in Q2, up from $22.6 billion a year earlier and above consensus expectations of $34.3 billion.

Consensus revisions following the quarter were modest at the headline level but more meaningful within segment detail. Total revenue expectations for fiscal 3Q 2026 have been revised only marginally, from $81.39 billion to $81.41 billion.

Revisions are strongest in Microsoft’s key growth pillars:

- Productivity and Business Processes expectations raised +1.5% vs. preQ

- Intelligent Cloud raised +1.1%, with Azure revenue lifted +1.4%, with implied growth moving up to 40%

Offsetting these increases were sharp downward revisions in consumer segments:

- Bing/More Personal Computing expectations cut -6.5%

- Gaming revised down -5.7%

- Bing and advertising revised down -2.1%

Despite Q2 margin upside, analyst expectations of Q3 operating income have edged down slightly (-0.6% vs. preQ), implying expectations for higher expenses. Still, EPS estimates have moved higher by +2.2%.

Meta Platforms: Q4 2025 review and outlook

Meta delivered a strong Q4 2025 earnings, with results coming in ahead of Visible Alpha consensus expectations across revenue, profitability, and earnings per share.

The quarter reinforced continued momentum in the company’s advertising business. The forward revisions pointed to a solid outlook heading into 2026. However, DAU trends were mixed in Q4 2025 and for Q1 2026.

CapEx expectations continued to rise sharply with FY 2026 revised up significantly after the Q4 2025 earnings release.

Meta reported revenues of $59.9 billion, ahead of Visible Alpha consensus expectations of $58.4 billion. The company reported diluted EPS of $8.88, which also surpassed Visible Alpha expectations of $8.24.

The outperformance was largely driven by the Family of Apps segment, which generated $58.9 billion in Q4, vs consensus expectations of $57.5 billion.

Reality Labs revenue came in slightly ahead of expectations but remains a smaller contributor with less visibility relative to the core advertising engine. Advertising revenue grew 24.3% year-on-year in Q4 to $58.1 billion, ahead of the $56.8 billion expected preQ.

Daily active user (DAU) trends were slightly below expectations:

- US & Canada DAUs: 210 million vs. 211 million expected (slight miss)

- Europe DAUs: 315 million vs. 317 million expected (slight miss)

- Asia DAUs: 970 million vs. 981 million expected (largest shortfall)

One of the most notable takeaways post-earnings for Meta has been the sharp upward revisions we’re seeing in analyst expectations for early 2026.

For Q1 2026, consensus revenue estimates have been revised materially higher:

- Revenue expectation raised from $51.3 billion to $55.5 billion

- EPS estimates revised higher by 6.1%, signaling continued earnings strength near term

- Q1 capex revised up 10.9%

Full-year expectations have also moved up:

- FY2026 revenue revised from $236.7 billion to $250.7 billion

- Full-year EPS revisions have been modest (+0.5%), suggesting that rising costs may offset some of the topline upside longer term

- FY2026 capex revised up 13.4%

Overall, Meta exited 2025 with solid fundamentals, but there seems to be an increasing focus on whether elevated CapEx would translate into sustained monetization and margin durability through 2026.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment