Research — March 3, 2026

GE Vernova to ride electrification wave as AI power demand accelerates

Energy infrastructure company, GE Vernova (NYSE: GEV) is poised for a strong fiscal 2026 as surging electricity demand from AI and data centers drives investment in power generation and grid infrastructure.

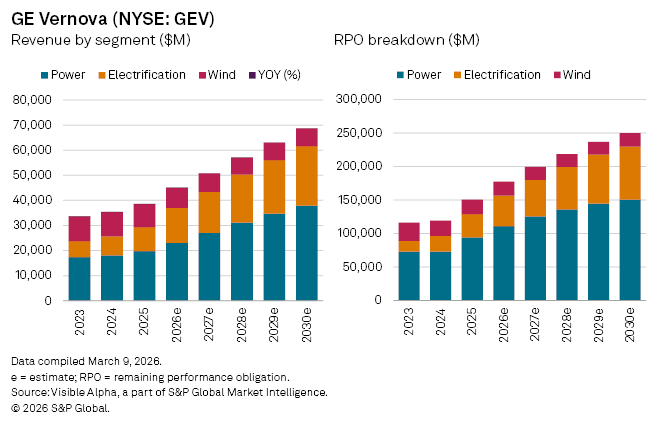

After a strong 2025, Visible Alpha consensus forecasts show revenue rising 17.2% year-on-year to about $44.6 billion in 2026. The growth reflects a sharp acceleration in electrification spending as utilities and hyperscale technology groups expand capacity to support energy-intensive computing workloads.

The company’s Electrification and Power divisions are expected to account for most of the expansion. Electrification revenue is projected to surge 44% to $13.9 billion in 2026, overtaking the Wind business to become GE Vernova’s second-largest segment. The Power division, anchored by gas turbines and long-term service agreements, is forecast to grow 16.9% to roughly $23 billion.

Orders tied to data-center electrification are expected to climb 29% year-on-year to $24.8 billion in 2026, while backlog in the Electrification segment is projected to rise 31% to about $45.3 billion. Demand for grid equipment such as transformers, switchgear and substations has been particularly strong as operators upgrade networks to accommodate higher loads and maintain grid stability.

On the generation side, orders are forecast to increase 21% to $39.8 billion, with remaining performance obligations, a key measure of future revenue visibility, rising 18% to $111.3 billion. Across the group, total RPO is expected to reach roughly $174 billion in 2026, up 16% from the prior year.

The Wind division remains the outlier. Offshore project delays and permitting hurdles continue to weigh on the business, and policy uncertainty in several markets has slowed the pace of new installations.

Even so, GE Vernova’s positioning in the energy value chain sets it apart from many peers. Exploration and production companies are more directly exposed to commodity price swings and benefit immediately from higher power or fuel prices. By contrast, GE Vernova generates a larger share of its earnings from equipment sales and long-term service contracts tied to generation and grid infrastructure.

That structure offers greater revenue visibility. As utilities, governments and technology companies race to secure electricity capacity for AI-driven computing; the company is monetizing a growing backlog that in many cases extends several years into the future.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment