Research — February 6, 2026

Endeavour’s price push to lift sales outlook in 2026, squeeze margins

By Mandar Ambhore

Australian retail drinks and hospitality company, Endeavour Group (ASX: EDV) signaled improving momentum in its core drinks retail business, in a preliminary earnings report released in January, as price reductions and targeted promotions helped draw customers back. The management, however, cautioned that a sharper pricing strategy is likely to come at a cost, putting pressure on margins across its largest division.

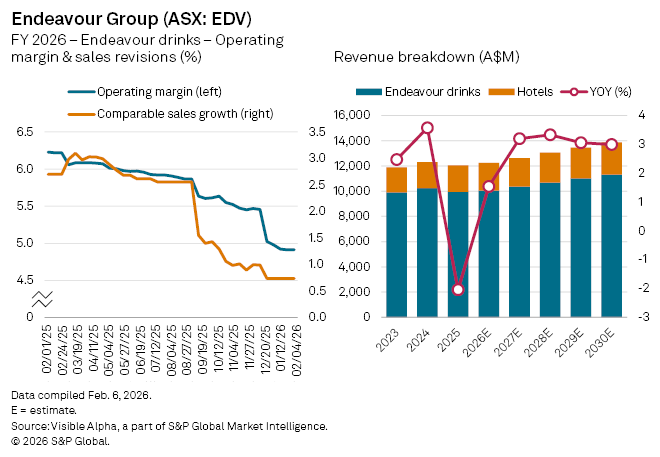

Visible Alpha consensus forecasts show analysts have materially revised expectations for Endeavour Drinks ahead of the group’s H1 FY 2026 results in March. Operating margin estimates for the segment have been cut to 4.91%, down from 5.66% last year and below the 5.63% analysts had penciled in prior to the last earnings.

Comparable sales growth expectations have also been tempered. Analysts now forecast growth of 0.74% in 2026, an improvement from the 1.5% decline seen last year, but weaker than the 1.26% preQ projections.

The outlook is brighter on the revenue line. Consensus estimates suggest Endeavour’s overall revenue will return to growth in fiscal 2026, rising 1.5% to A$12.2 billion after a 2% decline last year. The drinks division is expected to expand sales by 1% to A$10.0 billion, reversing a 2.9% fall in 2025.

Meanwhile, the group’s hotels business is forecast to deliver stronger growth, with revenue projected to climb 4.3% to A$2.2 billion. Analysts point to resilient holiday trading and the benefits of refurbished venues as key drivers.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment