Research — January 27, 2026

Netflix post earnings review: Q4 2025 and outlook

By Melissa Otto, CFA

Netflix Inc. (NASDAQ: NFLX) reported a solid fourth-quarter meeting or beating expectations in most areas of the business. The ad-supported revenue did fall short of expectations, causing some concern about the overall potential for this new business line. The company plans to spend more in FY 2026 to support the ad business, which may lead to higher growth longer term. On the back of the higher expenses around entertainment and product, the company’s FY 2026 operating profit margin guidance of 31.5% came in 120bps lower than the consensus of 32.7%. Visible Alpha consensus revisions following the results pointed to a more cautious near-term outlook as overall expectations for revenue drivers and profit were reined in.

Shares have drifted lower since the earnings release, reflecting in line revenue but concern over rising costs impacting the year-over-year margin and earnings growth. The streaming giant signaled plans to lift spending in 2026, to support content and commercial capabilities. In addition, the company noted a 50bps drag from M&A expenses. The market is awaiting the final approval and outcome of a potential deal for Warner Brothers Discovery.

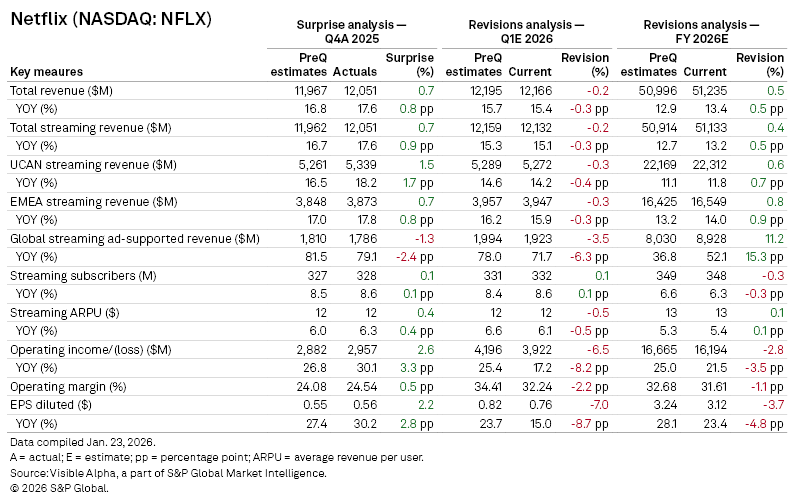

The streaming group reported Q4 revenue of $12.05 billion, slightly ahead of Visible Alpha pre-quarter expectations, with year-on-year growth of 17.6%. UCAN streaming revenue rose 18.2% year-on-year, exceeding Visible Alpha consensus expectations by 1.5%, while EMEA also delivered a modest upside.

Subscriber momentum was steady. Global paid memberships crossed 325 million, broadly in line with consensus expectations, while ARPU growth of 6.3% modestly exceeded pre-quarter forecasts. Global ad-supported streaming revenue, however, missed analyst expectations by 1.3%, with growth of 79.1% falling short of the 81.5% analysts had penciled in. The ad-supported tier, while still growing rapidly, underperformed expectations in the quarter. Overall, ad-supported revenue in the Q4 2025 and Q1 2026 were light of expectations but higher than consensus for FY 2026, suggesting the H1 may be a period of investment in ad segment for the company.

Operating income of $3 billion slightly exceeded Visible Alpha consensus expectations by 2.6%, supporting diluted EPS of $0.56/share, .01/share ahead of consensus. While revenue estimates for full-year 2026 have nudged higher, profit expectations moved in the opposite direction. Operating income estimates for 2026 have been cut by nearly 3%, and EPS forecasts have been revised lower by 3.7%, reflecting lower margin assumptions rather than demand concerns. Visible Alpha consensus shows analysts now expect operating income growth of 21.5% in 2026, down from a pre-quarter view of 25%.

Near-term revisions tell a similar story. First-quarter 2026 revenue estimates have been revised downward marginally, but operating income and EPS forecasts have been cut more sharply, by 6.5% and 7% respectively. Analysts appear to be baking in higher content investment, continued advertising build-out costs, and more measured margin expansion.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment