02 Jul, 2026

Spain's biggest lenders ride wave of growth in corporate and investment banking

By Cathal McElroy and Marissa Ramos

Spain's largest lenders are targeting a significant expansion of their corporate and investment banking businesses in the coming years to boost revenues outside their core retail banks.

Banco Santander SA, Banco Bilbao Vizcaya Argentaria SA and CaixaBank SA have all grown their corporate and investment banking (CIB) businesses in recent years amid favorable operating conditions and strong client demand. The increase in fee-based CIB revenue is particularly welcome as it comes at a time when the benefit the banks enjoyed from higher interest rates has faded.

"They are all playing the CIB business because there is continued business momentum among large corporates in Spain," as well as growing demand for risk management, hedging and advisory services due to increased geopolitical volatility, said Maria Parra, vice president, financial institutions at Morningstar DBRS. "It's a high-fee business, which will compensate for the lower net interest income the banks are generating compared to recent quarters."

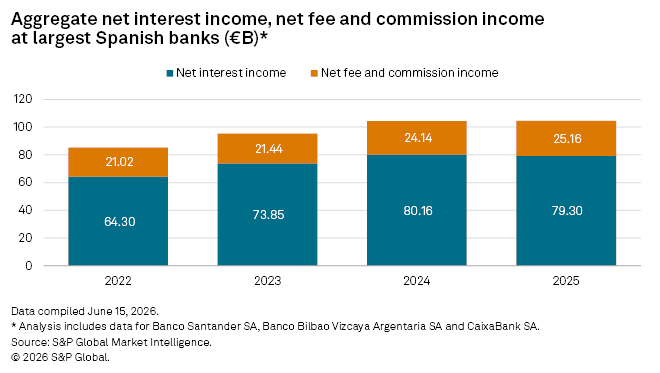

Aggregate fee income grew 4.2% to €25.2 billion in 2025, the data shows. Banks generate fee and commission income from businesses like CIB, insurance and asset management.

The growth of Spanish CIB has delivered some notable achievements in recent quarters.

Both Santander and BBVA have secured roles in seven of the largest IPOs in the world this year, Expansión reported.

In February, CaixaBank beat both Santander and BBVA to win mandates as a bookrunner in three of the four tranches of Goldman Sachs Group Inc.'s €7 billion bond issuance, the largest ever "reverse yankee" bond offering by a US bank.

Santander leads the charge

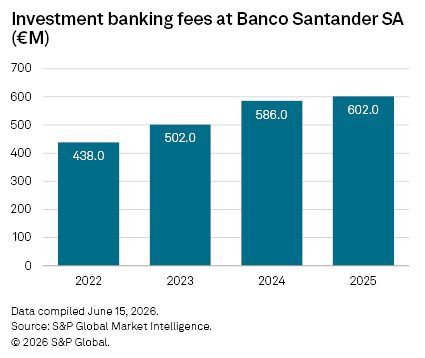

Santander is setting the pace for CIB expansion among Spain's big three banks. The Madrid-based lender, which is the only of the three with a separate and distinct CIB division, has achieved a 4.8% compound annual growth rate in the division's operating income since CEO Héctor Grisi took charge in 2022, Market Intelligence data shows.

CIB pretax profit hit €4.21 billion in 2025, surpassing 2022 levels after investment in the division weighed on returns in the previous two years. Strong year-over-year growth in operating income and pretax profit continued into the first quarter of 2026, the data shows.

Grisi's background — he was head of investment banking for Mexico, Central America and the Caribbean at Credit Suisse Group AG, where he spent 18 years — has helped drive the expansion of the division. The CEO's connections helped secure the talents of around 150 Credit Suisse bankers around the time of its collapse and takeover by UBS Group AG in 2023.

The absorption of a large chunk of Credit Suisse's investment bank in such a short period has turbocharged the performance of Santander's CIB division, which is comprised of global banking, global transaction banking and global markets business lines. The CIB division's growth has surged in the US, where fees grew by more than 30% in the last two years.

"CIB has seen a tremendous growth in fees," Grisi said during the bank's 2028 strategy presentation in February. "We're changing the business completely — before it was a corporate bank, now it's an investment bank."

Santander's recent $12.2 billion acquisition of Webster Financial Corp. will add around $24 billion of commercial and industrial loans and a similar amount of commercial real estate loans to its US lending book. An expected easing of US banking regulation by the Trump administration before the end of the president's term in 2028 could boost Santander's US CIB growth even further.

"That will be supportive," Carola Saldias, senior director, financial institutions at Scope Ratings, said in an interview. "It's better for Santander to be [in the US], awake and ready for what will happen."

BBVA emphasizes caution

BBVA is similarly confident of further strong growth in its CIB business after it posted a record €6.56 billion in revenue in 2025 and a 24% year-over-year revenue increase in the first three months of this year, according to a company press release.

Operating income and pretax profit at BBVA's rest of business division — which includes the bank's CIB operations beyond its core footprint of Spain, Mexico, Turkey and South America, and its digital banking business — have surged in recent years, Market Intelligence data shows. Operating income from the division more than doubled to €1.8 billion between 2022 and 2025, while pretax profit almost tripled to €772 million during the same period.

"We think we can create value by increasing our size in the CIB business in a very cautious way, in a risk-conscious way, in a way which is cross-border focused, sustainability focused, banking on our clients in their business outside our core geographies," CEO Onur Genç said during the bank's first-quarter earnings call in April.

The bank's current strategy aims to double CIB revenue by 2028 from 2025 levels. "BBVA's target for growth in CIB is pretty strong," said Parra.

CaixaBank rides economic growth

The performance of Spain's economy in recent years has been a key driver of CIB growth for all three banks. Spain was the fastest-growing among Europe's six largest economies in each of the last four years, Market Intelligence data shows. The country's economy grew by 2.82% in 2025, more than 1 percentage point higher than the next-fastest, the Netherlands.

A shift in Spain's economy toward high-value services and major investment in the green transition has helped fuel the growth,

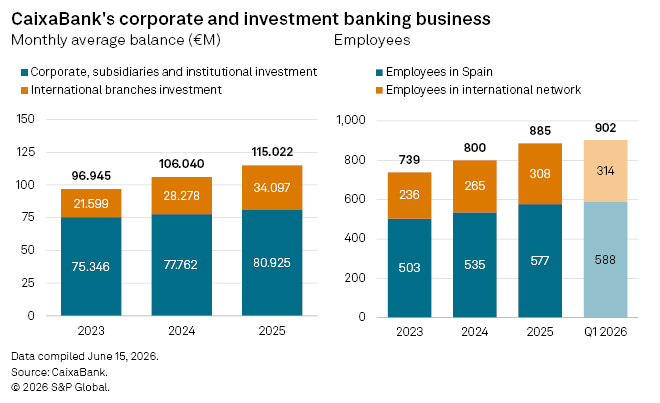

CaixaBank, the country's largest domestic lender, generates almost all its business from the Iberian Peninsula and

CaixaBank's corporate clients with operations beyond Iberia are increasingly providing the bank's CIB division with opportunities to complement its domestic growth. These relationships have allowed the bank to gradually grow CIB branches in France, Germany, Italy, Poland and the UK, and delivered growth of more than 50% in its international CIB loan book to €34.1 billion in the two years to the end of 2025, the bank's data shows.

"We see clear value in being a corporate bank in the eurozone given our size and our opportunities," CaixaBank CEO Gonzalo Gortázar said during the bank's first-quarter earnings call in April. CaixaBank will continue to expand CIB organically through new products and services, instead of chasing growth through acquisitions, Gortázar added.

– View divisional and geographic financials for Santander.

– Access Visible Alpha estimates data for BBVA. (May require additional subscription)

– View transcripts and investor presentations for CaixaBank.

Complementary business

Still, the big ambitions of the Spanish lenders are unlikely to trouble the giants of global investment banking. The three Spanish CIB businesses are dwarfed by US and European investment banking titans like JPMorgan Chase & Co. and UBS, and are unlikely to ever replicate the range and complexity of the products and services the giants of the industry offer, Marisa Fajardo, deputy head of research at Spanish investment manager GVC Gaesco, said in an interview.

Spanish CIB is "really corporate banking," Fajardo added. "CIB is market risk, it's not lending risk — the Spanish banks have kind of decaffeinated CIBs."

The Spanish lenders "are retail banks and they want to stay retail banks," said Nuria Álvarez, bank equity analyst at Madrid-based investment firm Renta4Banco, in an interview. Even so, the work done in recent quarters to build out their CIB should provide them with a reliable and steady stream of fee income that will cushion the impact of a lower interest rate environment, said Álvarez.

"I think the outlooks [for these businesses] are sustainable," said Álvarez.