12 May, 2026

Tesla's insurance premiums jump over 40% to $1.37B in 2025

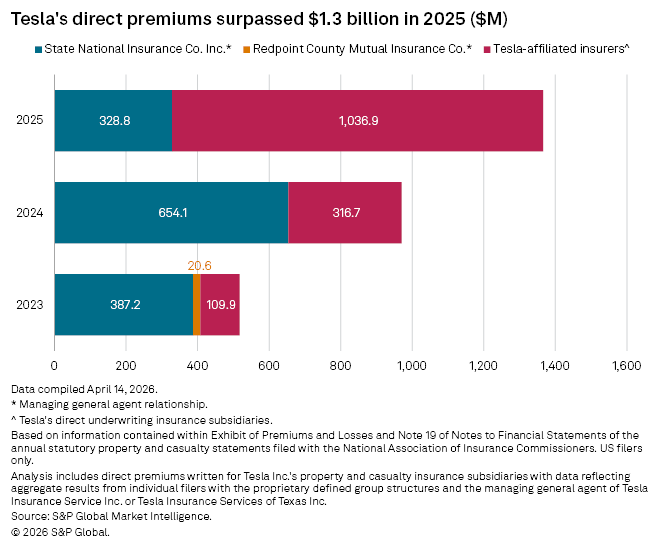

Tesla Inc.'s insurance business grew sharply in 2025, with total direct premiums written increasing by 40.7% to $1.37 billion, up from $970.8 million in 2024. The surge was driven by Tesla's aggressive shift to direct underwriting and substantial growth in California.

Tesla-affiliated insurance underwriting grew significantly, from $316.7 million to $1.036 billion, an increase of 227.4%. Tesla in 2025 directly underwrote 75.9% of all total premiums compared to 32.6% in 2024 and 21.2% in 2022.

Meanwhile, premiums written by managing general agents fell by 49.7% from $654.1 million to $328.8 million. A managing general agent is a specialized insurance intermediary granted certain powers and performing functions generally handled by an insurance company. State National Insurance Co. Inc., a subsidiary of Markel Group Inc., previously wrote a significant portion of Tesla's insurance business.

One reason behind Tesla's growth was due to the company underwriting policies directly that were previously written by State National Insurance Co. Inc. Following its one-time 5% discount in 2023 for customers to switch from State National to Tesla Insurance Co., the total share of business written by State National has fallen. In 2022, 85% of all business was written by State National, falling to roughly 75% in 2023, 67% in 2024 and 24% in 2025.

|

– Read about P&C industry results in 2025 |

California leads all other states

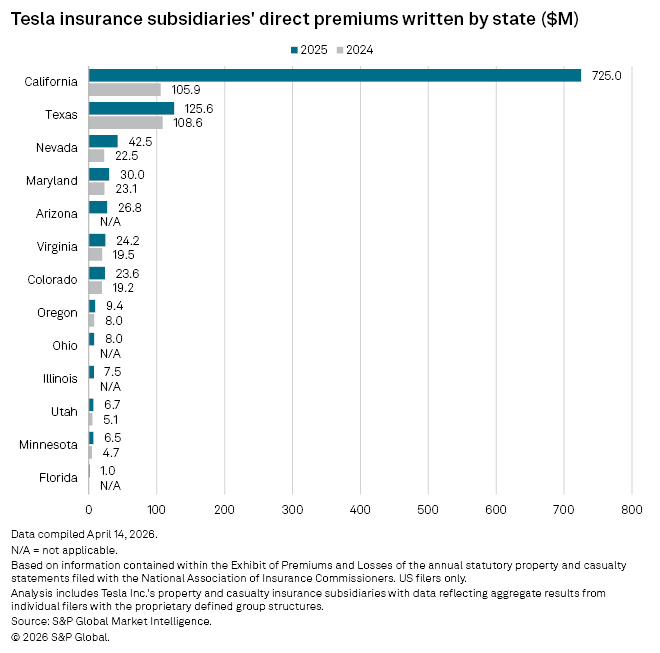

In addition, Tesla's direct premiums written in California grew by 584.5% from $105.9 million to $725 million. This was the largest year-over-year increase for any state. California represented almost 70% of all premiums written by Tesla in 2025, compared to 33.4% in 2024.

Texas fell to second place, writing $125.6 million of direct premiums, up 15.7% from 2024. The Lone Star state accounted for 34.3% of Tesla's premiums written in 2024, falling to 12.1% in 2025.

Nevada saw the second-largest growth in direct premiums, growing 89.2% from $22.5 million to $42.5 million in 2025. Arizona, Ohio, Illinois and Florida were new states where Tesla started writing business in 2025, with direct premiums written of $26.8 million, $8 million, $7.5 million and $1 million, respectively.

Loss ratio improves

Tesla has seen its direct loss ratio improve over the last three years, hitting 100.4% in 2025. This was an improvement of 2.9 percentage points from 2024. As a whole, the US private auto industry improved by 4.6 percentage points to a direct loss ratio of 61.5% from 66.1% in 2024.

Tesla writes business in the US through three different subsidiaries. The largest direct loss ratio was reported by Tesla Insurance Co., which writes business in California and Illinois, of 115.6%. This was a decrease of 1.2 percentage points over 2024's 116.8% direct loss ratio. Tesla Property & Casualty Inc. reported the largest decrease in direct loss ratio, from 98.6% to 66.7%, a decrease of 32 percentage points. Tesla Property & Casualty writes business in Texas, Colorado, Florida, Maryland, Minnesota, Ohio and Utah. Tesla General Insurance Inc. writes business in Arizona, Nevada, Oregon and Virginia and reported a decrease in direct loss ratio of 28.7 percentage points, from 105.1% to 76.4%.

Tesla reported a net loss of $182.7 million in 2025, attributing this larger loss than in 2024 to a "higher-than-expected loss ratio on the private passenger auto line of business, immediate expensing of commissions and higher underwriting expenses as a result of business growth."