20 Apr, 2026

War, inflation likely to restrain US interest rates regardless of Fed shakeup

By Brian Scheid

The war in the Middle East, and the volatile oil prices and inflation expectations that have accompanied it, will likely force interest rates to stay where they are even if a new Federal Reserve chairman pushes for rapid cuts, according to economists and market strategists.

Unless the domestic market collapses or inflation suddenly moves down to the central bank's persistently elusive 2% target, outcomes seen as highly unlikely, Fed officials will hold rates steady.

"It's going to take clear signs of labor market weakness and/or clear evidence the brunt of the inflation shock is behind us to get Fed officials to cut again," said Oren Klachkin, a financial market economist with Nationwide. "We see them waiting until the brunt of the Iran shock fades and then easing as policymakers seek to support the labor market. The timing [of a rate cut] could be delayed depending how the conflict evolves."

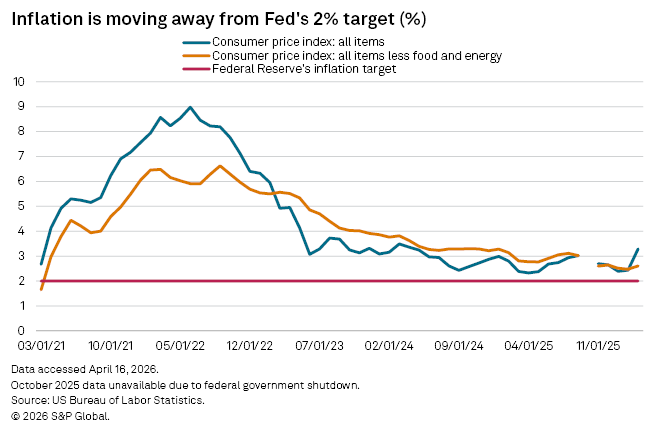

The Fed's dual mandate — to control inflation and keep the labor market at maximum employment — will be tested as the war persists, energy prices remain elevated and inflation continues to drift higher.

"The Fed is closely paying attention to the war," said Satyam Panday, chief economist with S&P Global Ratings. "The Fed is walking a tight rope. A rate cut while the war is still underway is totally possible if the labor market and/or financial conditions deteriorate sharply from here on."

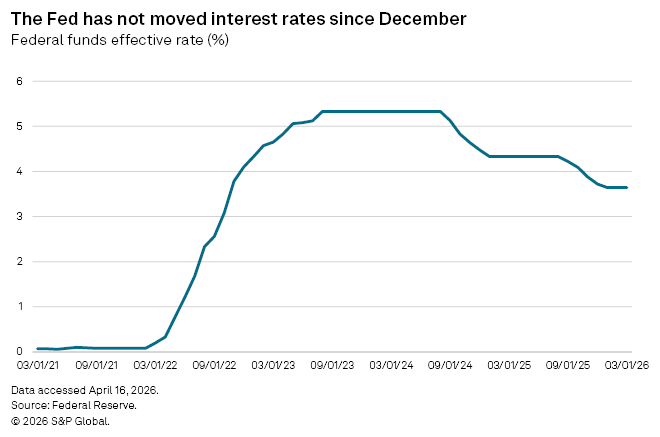

More than half of the futures market April 17 was betting that the Fed would keep its benchmark federal funds rate at its current target of 3.5% to 3.75% through the end of this year, according to CME FedWatch. A month earlier, close to 70% of the market was betting on at least one 25-basis-point cut by December.

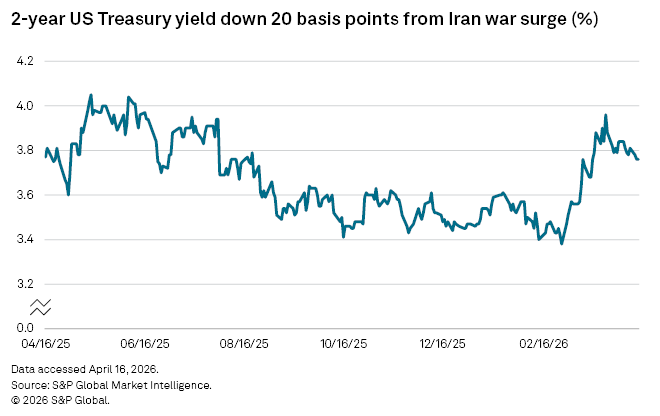

The 2-year US Treasury bond yield, which mirrors the market's view of what the Fed will do on rates, has jumped roughly 60 basis points since the war began at the end of February as expectations for multiple rate cuts shifted to the possibility of a rate hike.

"For the moment the Fed can play a game of wait and see, with the labor market holding up reasonably well for now," said Michael Hewson, a senior market analyst with iFOREX.

The Fed's biggest concern at the moment will be the primary and secondary impact of the sharp increase of oil, gasoline and other energy prices from war-related disruptions in the Strait of Hormuz, Hewson said.

The Fed could cut this year, but only if there was a "sharp deterioration" in the US labor market and central bank officials were confident that any rise in inflation would be limited in timing and scope, Hewson said.

"At the moment we have little evidence of either, which means that a rate cut remains a long way off," Hewson added.

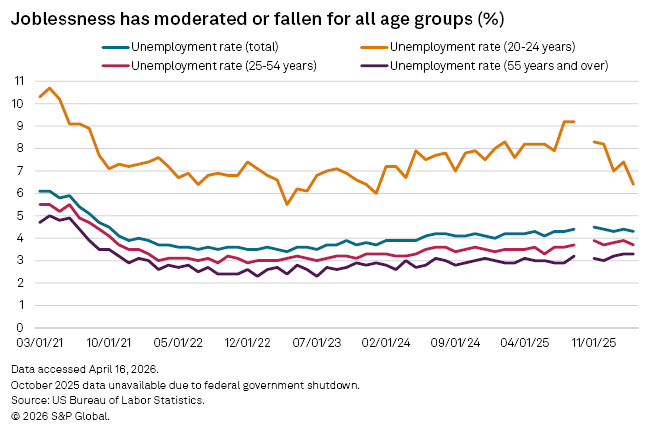

The US unemployment rate was 4.3% in March and has increased modestly over the past two years from a low point of 3.9%. The jobless rate for prime age workers, those between 25 and 54 years old, rose from 3.2% to 3.7% over that stretch.

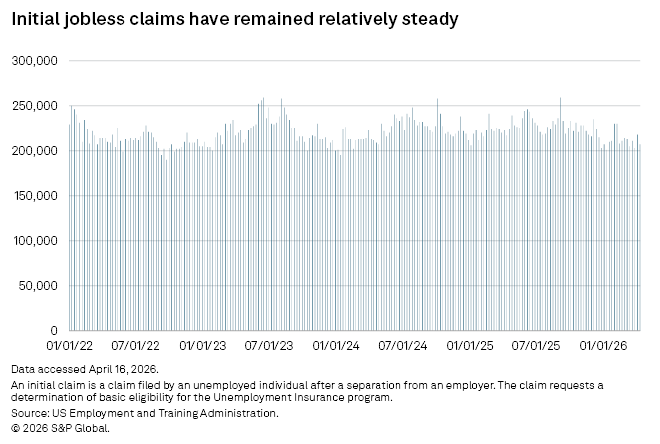

"Given that we have not seen a material rise in the unemployment rate or in initial jobless claims, labor markets look to be more evenly balanced and less volatile than they were a few years ago," said Jose Rasco, HSBC's chief investment officer for the Americas. "Unless we see a material rise in initial unemployment claims and the unemployment rate, it is doubtful the federal reserve will lower policy rates anytime soon."

With the labor market bending but not breaking and inflation unlikely to decline meaningfully for the time being, Rasco does not expect rate cuts in 2026 or 2027. That said, the US economy remains resilient, and secular drivers of the current tech revolution, led by AI, appear to be sufficient to keep the economy growing, Rasco said.

"We do not see the need for Fed easing anytime soon," Rasco said. "Clearly, if the war were to drag on more than four to six months, the possibility of an economic slowdown or outright recession would rise, but that is not our base case at the current moment."

Even if joblessness does increase substantially, a continued rise in inflation may keep the Fed from cutting rates, said Derek Tang, an economist with Monetary Policy Analytics.

"Crucially, inflation expectations may un-anchor and alarm [Fed officials] enough that even labor market weakening won't be enough to start easing," Tang said.

Warsh is scheduled to appear at a confirmation hearing before the Senate Banking Committee on April 21. Even if he is confirmed by the time Powell's term as chair ends May 15, Trump's push for immediate rate cuts probably will not be successful.

"We do not see nomination process of the new chair materially impacting future rate moves," said Panday with S&P Global Ratings. "The Fed makes policy by committee; the chair has the power to sway but the final decision depends on majority vote."