30 Apr, 2026

Singapore's DBS expects earnings to stay flat in 2026 amid stagnant rates

By Yuvraj Singh

DBS Group Holdings Ltd. expects income growth in 2026 to stay muted as global interest rates are likely to stay at current levels.

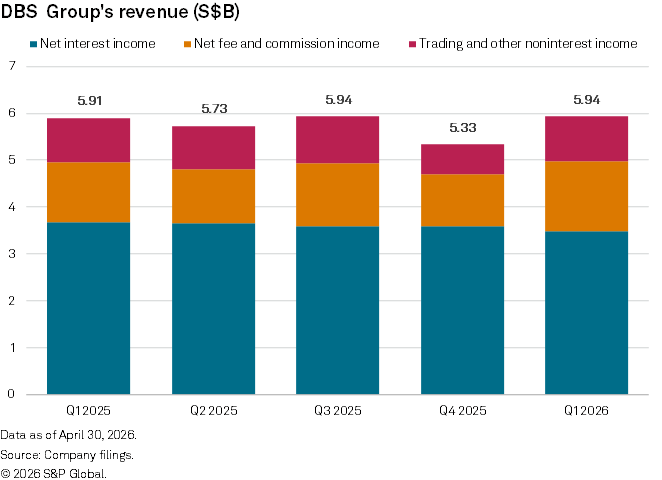

DBS, Southeast Asia's largest bank by assets, reported a 1% year-over-year rise in net profit to S$2.93 billion for the January-to-March quarter, largely due to a pickup in fee income. Net fee and commission income climbed 16% to S$1.48 billion, offsetting pressure on net interest income. Net interest income declined 5% to S$3.49 billion, the bank reported on April 30.

"Although profit rose only 1%, DBS Group achieved record wealth management fees, highlighting strong growth in fee-based income," said Paul Lee, senior analyst at Westpac Singapore, in a social media post. "This matters because such income is less tied to interest rate cycles, making earnings more stable and diversified compared to traditional lending, which depends heavily on interest margins and rate movements."

Evolving income mix

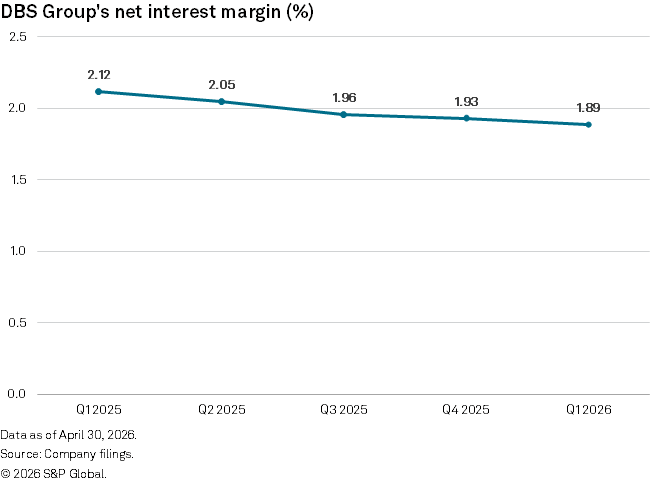

The bank's net interest margin (NIM) fell to 1.89% in the first quarter, from 2.12% a year ago due to the decline in the Singapore Overnight Rate Average (SORA), a proxy benchmark interest rate used by Singapore banks for pricing loans.

Interest rates began trending lower in 2025 after the US Federal Reserve started easing its monetary policy. Falling interest rates reflect more quickly in banks' lending, squeezing their NIMs.

"Singapore interest rates represented by SORA fell from 2.54% in the first quarter of 2025 to 1.07% in the first quarter of 2026," said CFO Chng Sok Hui. "SORA is now less than half of what it was a year ago."

Interest rate drag

DBS expects the drag from interest rates to be "largely mitigated" as rates may stabilize at current levels in the near future. "We're not expecting any rate cuts from the US because of the high price of oil caused by the war," CEO Tan Su Shan said during an April 30 earnings call.

The Monetary Authority of Singapore on April 14 tightened its monetary policy by setting the local currency on a steeper appreciation path against currencies of the nation's key trading partners. Central banks in Australia and the Philippines have raised rates in recent weeks as inflationary pressures build. However, the US Federal Reserve is widely expected to adopt a more dovish stance under its incoming chair Kevin Warsh.

Singapore banks may face loan growth in the mid-single-digits range, lagging deposit growth projected at high single digits. This imbalance could weigh further on margins, as excess liquidity is deployed into lower-yielding assets.

"[Loan growth] depends on how businesses feel about their own growth opportunities. And obviously, if the war prolonged, and businesses don't feel confident our business or credit starts to be looking bad, then loan growth will not be as strong as GDP growth, or it will be just at GDP growth," Tan said. "So mid-single digit [outlook for loan growth], I think, is fair."

Middle East risks

DBS flagged minimal direct exposure to the ongoing Middle East conflict, noting that its regional portfolio is largely linked to high-quality sovereign and state-owned entities. However, management remains cautious about second-order effects, particularly through inflation and supply chains.

"The second-order impact is what we are more focused on because, obviously, if inflation remains high, price of oil remains high," Tan said. "But more importantly, it's not just the high inflation, it's the lack of supply ... That's a problem."

Supply disruptions could take time to ease, and tighter monetary policy offers limited relief in such a scenario. "We're going to have to live through potentially one or two quarters of supply chain breakages," Tan added.