06 Apr, 2026

Renewable energy companies court buyers to unlock AI demand growth windfall

By Allison Good

|

Renewables firms are increasingly turning to the M&A market to finance projects aiming to serve large-load customers like data centers, above. |

A sector-wide push among North American renewable energy companies to capture soaring power demand by expanding beyond traditional wind, solar and storage projects is fueling a new wave of acquisitions.

The industry has been an attractive target for private equity and infrastructure investors in recent years due to lackluster returns on investment and weaker public market valuations, but the race to serve AI customers is driving an urgent need for deeper pockets of capital, experts told Platts, a part of S&P Global Energy.

"You're seeing more traditionally pure-play renewables companies looking to expand their capabilities outside of their core businesses to capture AI power demand," Brett Castelli, a senior energy and utilities analyst at Morningstar, said in an interview, citing solar tracking system supplier Nextpower Inc.'s move into inverters.

On the developer side, "big and serious" firms are "trying to reposition their business around adding behind-the-meter gas deals and … powered land," Marathon Capital LLC co-founder and CEO Ted Brandt said in an interview, referring to the business of providing large-load customers with generation, land and grid access.

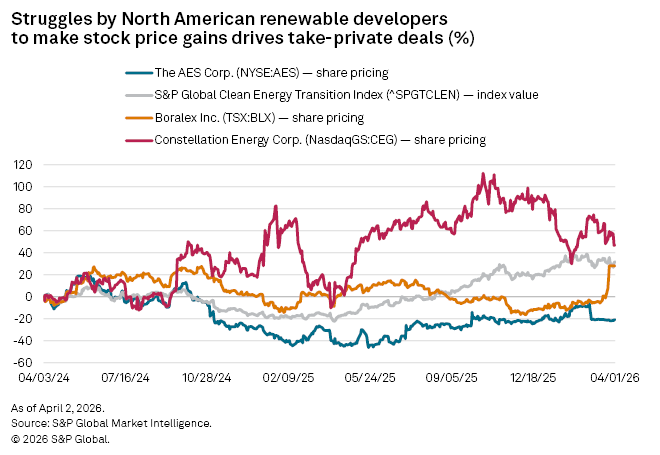

In addition to Brookfield Asset Management Ltd. and La Caisse de dépôt et placement du Québec's recent agreement to take Canadian independent power producer Boralex Inc. private for C$3.8 billion, and the long-awaited acquisition of AES Corp. by a BlackRock Inc.- and EQT AB-led consortium for $10.7 billion announced in March, hyperscalers have also entered the market.

Alphabet Inc. subsidiary Google LLC became the first hyperscaler to buy an IPP, closing a $4.75 billion deal for Intersect Power LLC from global asset manager TPG Inc. in March after announcing the transaction in January.

The buyers of Intersect Power and AES are getting both companies' experience in developing, owning and operating renewable energy projects, Peter Gardett, CEO of market data platform Noreva, said in an interview.

"It's that build knowledge, and they're paying a premium for it," he added.

That means private equity and infrastructure funds are now in direct competition with hyperscalers for similar targets.

"If I was Amazon.com Inc. or someone else looking for speed to power, if I was EQT and I'd just raised a big infrastructure fund, I'd be looking at those portfolio companies that look like they have a build premium attached to it," Gardett said.

Given that data centers account for a significant portion of anticipated load growth through the end of the decade, developers are competing for a limited pool of financing from tech giants investing in AI, whether through corporate buyouts or long-term contracts.

"The dream of every developer is, 'How do I find a hyperscaler and anchor one of their projects?'" Marathon's Brandt noted. "That's a very competitive market. There's only five investment-grade hyperscalers."

Depressed values, returns

Developers have been struggling to capture their value as public companies in an environment characterized by inflation, higher interest rates and market saturation.

AES and Boralex saw their share prices dip 41% and 27%, respectively, from 2022 through 2025.

"If we had the economics we had in 2020 and 2021, where developers were making very strong returns on their businesses — they could build a project at one interest rate, monetize it at a lower interest rate and essentially take out 15 to 30 cents per watt kind of development profits — that would be different," Brandt said. "But for the last four years, what we've seen is inflation driving up capital costs, and developers have just been making very, very narrow returns."

Early-stage solar and energy storage projects in inundated markets like the Electric Reliability Council of Texas Inc. and PJM Interconnection have also become "worthless," according to Prashant Khorana, director of power and renewables consulting at Wood Mackenzie.

"You used to get something like $5 to $15 per kilowatt for early-stage projects … but now it's basically worth zero," Khorana said in an interview.

Public companies are not rushing to snap up distressed developers, either.

Joe Dominguez, president and CEO of gas and nuclear power giant Constellation Energy Corp., affirmed during a March 31 conference call that buying a renewables developer does not make economic sense for the company despite its growing large-load customer base.

"The returns on renewables are often underwhelming when we're looking at some of these deals," Dominguez told investors and analysts. "I don't yet see a platform that is attractive enough and is going to meet our threshold for 10% unlevered [internal rates of return]."

Going public?

Hecate Energy, which develops, owns and operates utility-scale energy parks, has opted for a different path to long-term profitability.

In January, the independent power producer announced that it had agreed to a reverse initial public offering and will merge with EGH Acquisition Corp. to become a public company at a pre-money enterprise value of $1.2 billion. EGH, a special purpose acquisition company (SPAC), will provide up to $155 million for Hecate's development portfolio, which the IPP envisions leveraging into behind-the-meter power solutions for large-load customers.

"Access to the public markets, as you've heard, is an important step in unlocking the value that's in Hecate's substantial backlog, and this transaction offers an attractive entry valuation, solid asset coverage and a clear near-term growth potential, making it a compelling opportunity for investors," EGH Acquisition CEO Drew Lipsher said during a Feb. 6 investor conference.

But Wood Mackenzie's Khorana pointed to solar power developer Altus Power Inc., which went public in 2021 via a CBRE Group Inc.-sponsored special purpose acquisition company but was taken private in 2025 by TPG, as a cautionary example.

Between Dec. 10, 2021, when its stock began trading on the New York Stock Exchange, and the Feb. 6, 2025, deal announcement, Altus Power stock plummeted nearly 63%.

Hecate will likely get taken private again if the reverse merger closes, according to Khorana.

"Choosing to go public through SPAC, I would not personally think about it as a victory lap," Khorana said. "I don't think I've ever seen a pure play renewables-only IPP go public and the stock continue to appreciate because public markets just don't really reward develop and flip-type activity in general."

"SPACs are generally the last resort," he added. "Selling to a private equity or infrastructure fund is generally the best course of action for companies to find relatively disciplined, patient capital."