13 Apr, 2026

Higher energy prices complicate monetary policy paths for major central banks

By Nick Lazzaro

| A tanker docked at a port in Japan on April 8, 2026. As one of the world's largest net energy importers, Japan's economy is particularly exposed to energy price shocks stemming from the ongoing Middle East conflict involving the US, Israel and Iran. Source: Yuichi Yamazaki/AFP via Getty Images. |

Soaring oil prices have pushed up inflation expectations in many of the world's largest economies, prompting markets to reassess the expected path of central bank monetary policy.

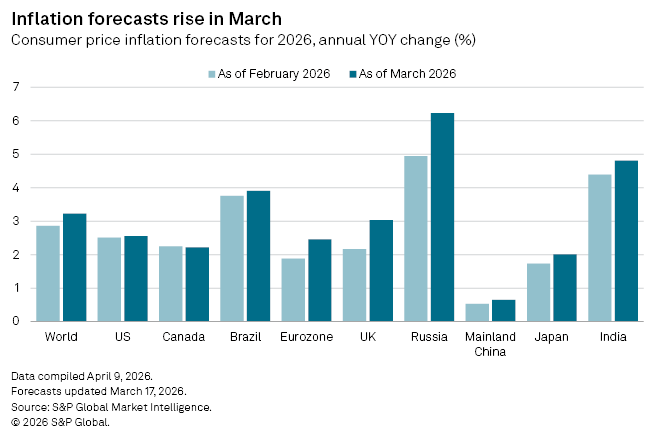

S&P Global Market Intelligence raised its forecast for global annual consumer price inflation to 3.2% in March, up from 2.9% in February. The revision reflected higher inflation expectations in eight of the world's nine-largest economies.

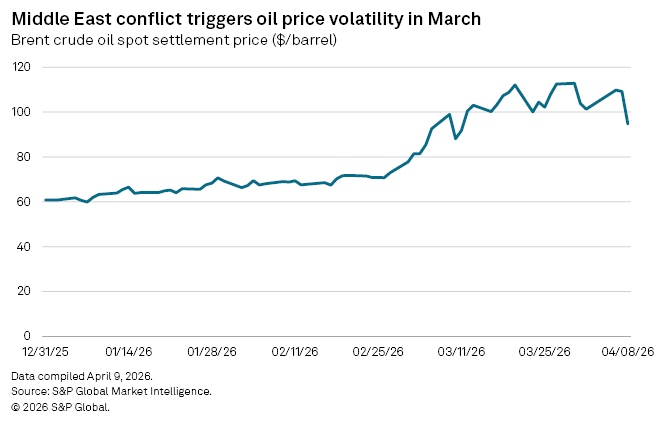

The war in the Middle East, which began in late February, has restricted shipments through the Strait of Hormuz, a major oil shipping route. That, combined with Iranian attacks on neighboring countries' oil production sites and refineries, as well as several pipelines, has pushed prices sharply higher.

For central banks that began the year with interest rate-cut expectations amid easing inflation, markets have increasingly questioned whether an energy-driven resurgence in inflation could pause these easing cycles or prompt a pivot to policy tightening.

"The Middle East conflict and related inflationary pressures are a game changer for monetary policy prospects," Ken Wattret, vice president of global economics at Market Intelligence, said in an email. "At a global level, monetary conditions will be much less accommodative in 2026 than we had expected prior to the conflict."

Brent crude oil prices rose steeply in March as the conflict progressed, reinforcing inflation concerns. Most central banks are likely to look through short-term, energy-driven increases in inflation and avoid abrupt changes to policy, but stances could shift if higher energy prices persist and feed into broader, second-round inflation effects, according to Wattret.

"The collective underestimation of inflationary pressures by major central banks following the COVID-19 pandemic and the subsequent Russia-Ukraine conflict increases the likelihood of a 'stitch in time saves nine' approach this time around should the conflict-related disruptions persist and inflationary pressures broaden," Wattret said.

Energy exposure

The energy price shock in March led markets to price in a higher probability of interest rate hikes in many countries, according to John Canally, head of portfolio strategy at TIAA Wealth Management. Any long-term impact of energy prices on inflation and, subsequently, on interest-rate policy will vary depending on exposure to energy imports.

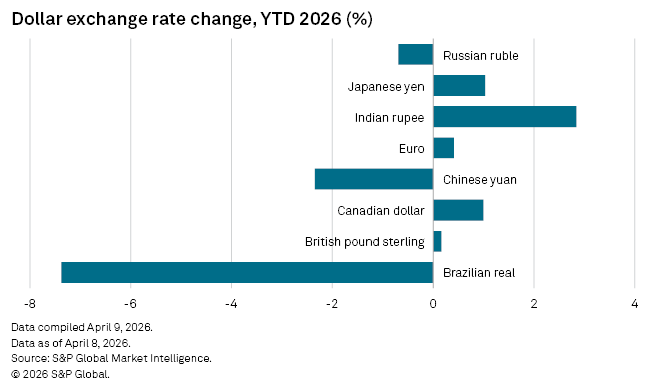

"Because energy prices are set in global markets, no country is truly immune to higher energy prices," Canally told Market Intelligence. "That said, the US is more insulated against higher crude prices, and that has led to a higher US dollar during the conflict in Iran."

Japan, India, the UK and the eurozone are more dependent on energy imports and vulnerable to related inflation, while energy exporters such as the US, Canada and Norway face less relative risk, Canally said.

Energy price volatility in recent weeks has also reflected changing expectations around ceasefires and escalation, with the most recent two-week ceasefire contributing to a pullback in oil prices. The durability of energy price pressures beyond an official end to the Middle East conflict will depend on the length and scope of the conflict, damage to the region's energy infrastructure, and the speed at which energy production and shipping normalize, according to Alexis Crow, partner and chief economist for PwC US.

"Central banks will be wise to wait and see but could prepare for a more protracted landscape of elevated commodity prices," Crow said in an interview.

Developed markets

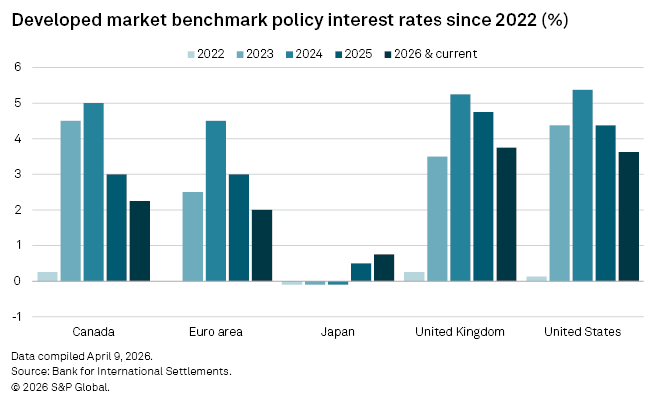

Among the major developed economies, the US Federal Reserve, Bank of England and European Central Bank are likely to be more patient this year.

"Markets were too aggressive in terms of pricing rate cuts, and now it seems that markets are too aggressive in pricing rate hikes, at least with respect to the timing of those rate hikes," said Conrad DeQuadros, head of economics for the Citi Wealth Chief Investment Office.

Even before the war, additional rate cuts from the three banks would have been increasingly difficult to justify given persistent inflation trends, DeQuadros said. The Bank of Japan, by contrast, entered the year having begun a tightening cycle, and its forthcoming decisions may be more responsive to energy prices and upward pressure on headline inflation, he said.

Emerging markets

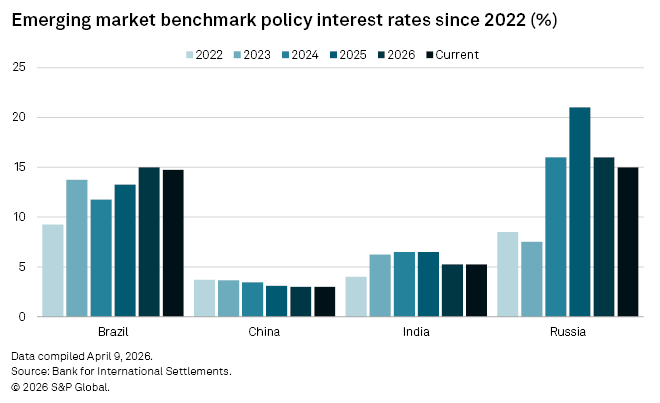

In the world's largest emerging markets, the Reserve Bank of India will likely face pressure from rising energy prices at a time when India is already navigating food price inflation and a weakening currency.

"Everything that India is importing is more expensive because its currency is weaker," DeQuadros said. "That's another issue that the Reserve Bank of India will be thinking about because one of the ways to prevent or try to put a cap on that weakening is through a higher policy rate."

China, with its increased investments in domestic natural gas production, and Brazil, which entered the year with a higher policy rate relative to other major economies, appear better positioned to withstand elevated energy prices.

"As a major commodity exporter with little linkage to the Strait of Hormuz, and with a central bank which had frontloaded its rate hiking cycle, Brazil is well insulated from this present external shock," PwC's Crow said. "China has also been deeply abstemious coming out of the pandemic in terms of using fiscal largesse to be able to support economic activity, so it is in a stronger position here."