19 Mar, 2026

War with Iran clouds rate plans as Fed officials boost inflation forecasts

By Brian Scheid

As the newest US war in the Middle East continues with no clear end in sight, the Federal Reserve's interest rate path also appears to be shrouded in the fog of war.

The Fed's rate-setting Federal Open Market Committee (FOMC) on March 18 kept its benchmark federal funds rate between 3.5% and 3.75%, where it has been since December and where it could remain as long as the US war with Iran continues.

"The longer this disruption continues, the more likely it is that the Fed will not cut rates at all this year," said Kathy Jones, managing director and chief fixed income strategist for the Schwab Center for Financial Research.

With inflation moving away from the Fed's 2% target, the labor market wobbling, and the duration and ultimate consequences of the war still unknown, the course of US monetary policy faces significant ambiguity.

"The implications of developments in the Middle East for the US economy are uncertain," Fed Chairman Jerome Powell told reporters shortly after the FOMC's two-day meeting concluded this week. "We just have to wait and see what happens."

So far, gasoline prices have risen close to 30% since the start of the Iran attacks and inflation expectations are climbing.

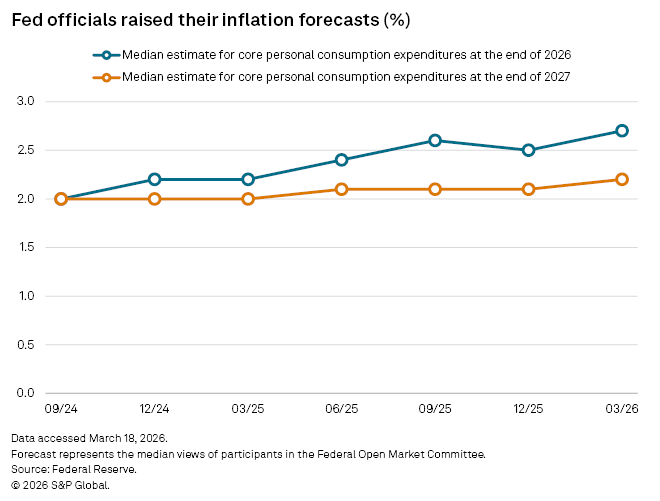

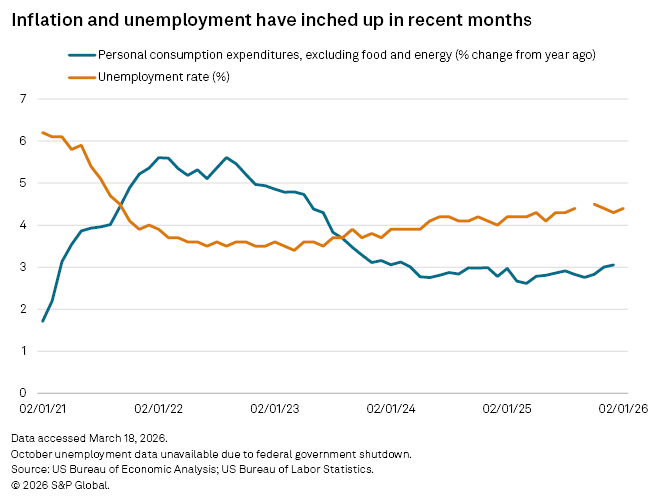

In the FOMC's new quarterly summary of economic projections, the median view among Fed officials is for the annual growth of headline personal consumption expenditures (PCE) and core PCE, which strips out volatile energy and food prices, to both rise to 2.7% by the end of 2026. In its previous projections released in December, FOMC members saw annual growth of PCE at 2.4% and core PCE at 2.5%.

The Fed's next rate cut could happen while the war continues, but that looks unlikely given the recent acceleration in both PCE inflation and the producer price index, which jumped an unexpected 70 basis points from January to February, and rapidly rising energy prices, said George Pearkes, a macro strategist at Bespoke Investment Group.

"It's hard to imagine a cut unless the FOMC is convinced we are tilting into recession," Pearkes said.

More likely, the Fed could restart rate cuts if there is a "material worsening" of the domestic labor market, said Pearkes.

The labor market has shown some cracks. US payrolls fell by 92,000 jobs in February, according to the latest government data, and after some downward revisions, just 156,000 jobs have been added since February 2025. By comparison, more than 1.07 million jobs were added from February 2024 to February 2025.

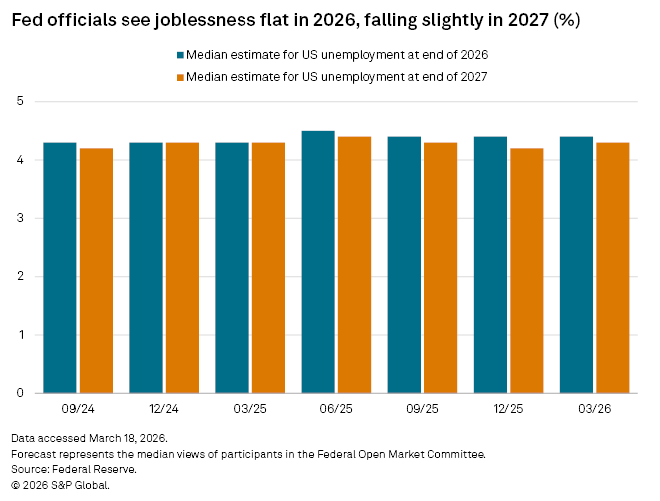

Still, unemployment has shown no signs of significantly increasing. The US unemployment rate was 4.4% in November, up slightly from a year earlier when it was 4.2%.

Uncertainty rises

If the labor market weakens more quickly than expected, the Fed is likely to respond with a rate cut, but that outcome is increasingly uncertain, said Esther Sholes, a senior macro analyst for Take Profit Trader.

"What has clearly shifted at this meeting is the current level of uncertainty, made evident by Powell's responses being peppered with this phrase, that spans the war, labor market, and tariff impacts," Sholes said. "Against this backdrop, holding rates steady is the right move."

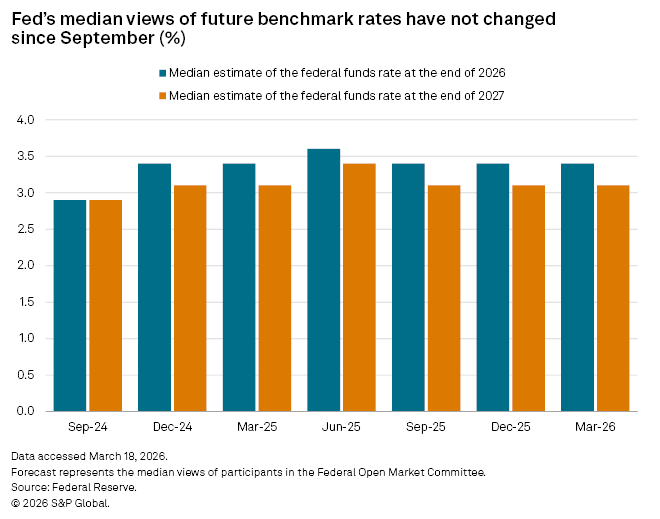

While inflation heats up, Fed officials still forecast just one 25 bps rate cut in 2026, as they have since September. Fed officials are not changing their outlooks on the pace of cuts at least partly due to signs of well-anchored longer-date inflation expectations in the swaps market, said Daniel Siluk, head of global short duration and liquidity at Janus Henderson Investors. Five and 10-year breakeven expectations have barely budged since the war began at the end of February, Siluk said.

"That pattern suggests markets still view the inflation impact of the oil shock as temporary, and the potential demand hit from higher energy prices carries a disinflationary impulse over time," Siluk said. "Until officials see evidence that inflation expectations are drifting higher in a persistent way, they are unlikely to rethink the broader rate‑cut trajectory."