24 Mar, 2026

Volatility in interest-rate expectations set to persist as Iran war continues

By Brian Scheid

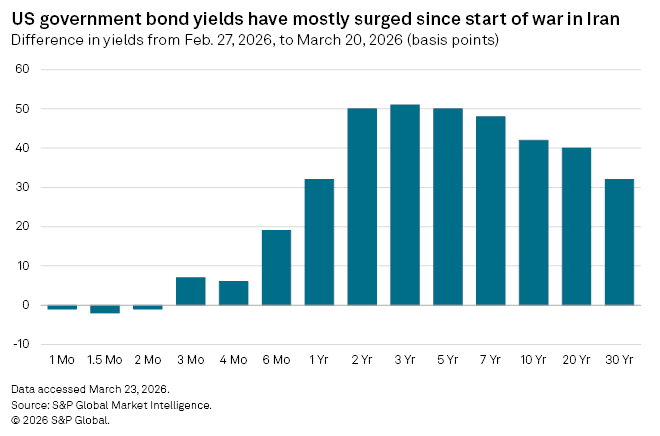

The war with Iran has stoked volatility in US government bond yields and interest rate expectations while boosting concerns about inflation.

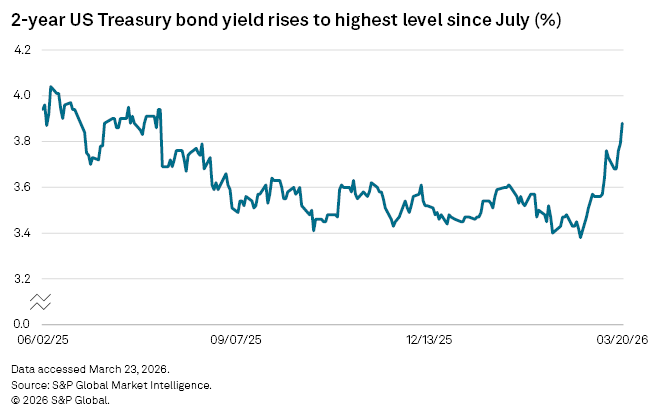

On March 23, the 2-year US Treasury bond yield, which closely tracks Federal Reserve monetary policy and expected interest rate moves, spiked and then fell amid changing political commentary about the potential for US strikes on Iranian energy sites.

The bond yield briefly climbed above 4%, a 62-basis-point increase from when the war began in late February, before falling about 20 bps after President Donald Trump said the US would hold off on energy site strikes.

The futures market's interest rate expectations saw similar whipsaw movement. On March 20, roughly 25% of the market was betting that the Fed would raise rates at least once by the end of 2026, according to CME Group Inc. That marked a significant change from March 13, when no one expected a rate hike, and about 70% of the market was betting on at least one rate cut by the Fed's December meeting. The predicted odds of a rate hike then fell to less than 10% on March 23 amid reduced concern about potential energy site strikes, according to CME FedWatch

"The market is very volatile, and as quickly as it priced out cuts, and then priced in hikes, it has now mostly removed those hikes following today's comments by President Trump," said Esther Sholes, a senior macro analyst for Take Profit Trader, in a March 23 interview. "In light of this uncertainty, I continue to see the Fed on hold until they get clarity on the impact of the war, particularly of oil prices, on inflation, or until a definitive downside risk to growth and employment develops."

The Fed, which has not moved its benchmark interest rate since December 2025, will likely hold rates in its current 3.5% to 3.75% target range, unless "there is more clarity on how the macros impulses will evolve," said Padhraic Garvey, head of global rates and debt strategy at ING.

Even so, bets on rate hikes, once unthinkable a couple of weeks earlier, will spike as views on the war dim and the potential for significant, future energy supply disruptions remain, Garvey said.

"It's still a tad too early to assert that this will indeed happen, as the warpath could look quite different in the next few weeks," Garvey said. "But things have not gone great in the past week or so, when it comes to the impact on global energy prices. Until that is materially negated by events, the rates market seems keen to double down on the rate hike risk."

A rate hike from the Fed still seems unlikely, according to Derek Tang, an economist with Monetary Policy Analytics. He said the futures market could be giving too much weight to the risk of soaring inflation and not enough to the Fed's resistance to recession risk, which would climb if rates were cut.

"The war in Iran certainly adds insult to injury on the inflation front, given poor inflation performance and the trauma of high inflation the last few years," Tang said. "However, markets were already jumpy because other Trump reforms like tariffs and immigration changes also trend in the inflationary direction, so there is a growing question [of] how much inflation the public will tolerate before raising expectations."

In order for bets on rate hikes to diminish, the futures market needs to see "credible evidence" of de-escalation in the Middle East, Tang said.