24 Mar, 2026

US utilities turn to private credit to fund unprecedented growth

By Allison Good

Private credit providers are fielding increasing inquiries from US investor-owned electric utilities as the industry prepares to spend record amounts of capital, according to sector experts.

But while those lenders describe a rising demand for more tailored and flexible terms, not all types of utility assets may be well-suited for private markets.

Utilities' "rising external financing needs are often overlooked as growth remains the focus," analysts at Jefferies wrote in a Feb. 18 report, noting that the capacity to raise funds "has become a key financial differentiator beyond just capex and [earnings per share] growth."

While electricity demand remained "relatively flat" for almost 20 years, according to the US Energy Information Administration, consulting firm Grid Strategies expects the artificial intelligence sector's data center development boom to fuel annual load growth of 5.7% from 2026 through 2030.

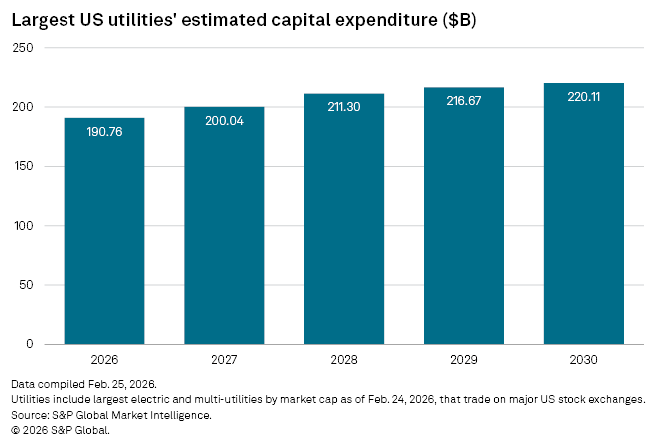

Utilities expect to increase spending over the next five years to facilitate the infrastructure build-out required to power data centers, industrial demand and other projected load growth. Combined capex plans for the 20 largest US electric utility holding companies will grow from $190.76 billion in 2026 to $220.11 billion in 2030, according to S&P Global Market Intelligence data.

Utilities have historically tapped the public markets to fund expenditures, but executives at Duke Energy Corp. and Xcel Energy Inc. said during interviews at a November 2025 conference that their companies are in talks with private debt lenders to finance portions of their long-term infrastructure investment programs.

Private credit involves directly originated loans that are not broadly syndicated, typically provided by nonbank lenders and structured as bespoke solutions.

"Finding partners to fund capex is a critical part of portfolio optimization, and private capital is stepping in as a key financing solution," Brent Canada, infrastructure debt partner at Ares Management Corp., said in an email.

While there is no shortage of public credit available for utilities, the kind of transformational spending projected through the end of the decade is driving management teams to consider alternative financing.

"When you have a market that goes through an inflection point like what we're seeing across the power and utilities landscape today, there is a combination of both curiosity and reality to test the boundaries by which access to flexible capital solutions and access to opportunities to refinance can bolster one's arsenal of capital for growth," Harlan Cherniak, head of infrastructure debt at Macquarie Group Ltd. subsidiary Macquarie Asset Management Inc., said in an interview with Platts, part of S&P Global Energy.

Financial flexibility

Cherniak and other private credit professionals said in interviews that they have noticed the utility industry's sudden interest in their products, noting that those companies are "natural" counterparties given their high-quality assets.

While private credit is more expensive than public debt, it is also significantly more flexible when it comes to duration, interest rates, credit ratings and collateral required.

"There's not that many limitations on how you write the underwriting agreements that underpin a private credit loan," Peter Gardett, CEO of market data platform Noreva, said in an interview.

Don Dimitrievich, senior managing director at Nuveen LLC and portfolio manager for energy infrastructure credit, said the asset management firm has "had discussions with some of the utilities" to create special purpose vehicles for planned infrastructure that can be funded as separate entities on balance sheets and insulated from the rate base.

"It meets the timeline that the hyperscalers are looking for," Dimitrievich said. "Two, it allows the utilities to effectively provide that power generation, particularly in places where … there are multiple incentives to support the build-out."

Andy DeVries, CreditSights co-head of investment-grade credit, pointed to NiSource Inc.'s NIPSCO Generation LLC as a model for the rest of the sector. NiSource received regulatory approval in 2025 for the entity created to construct new generation for skyrocketing large-load demand growth.

"NIPSCO is the blueprint for all of these utilities," DeVries said in an interview. "You ring-fence it so ratepayers aren't paying any extra, and then you have the data center customer pay even more money to credit ratepayers."

That kind of "highly-tailored" structure insulating ratepayers from ballooning bills is "where private credit lives," DeVries continued.

Private credit can also help utility companies fund their capex plans by providing alternatives to selling existing assets, now that many in the sector have divested whole or partial stakes in noncore holdings, by providing a "less permanent solution," according to Blackstone Inc. Managing Director of Credit Zach Rubenstein.

"Once the capex needs have stabilized, the utility can look to refinance or continue to optimize the manner in which they own the asset," Rubenstein said in an interview.

While private credit initially emerged to serve non-investment-grade rated entities, it has expanded to compete with banks for more traditional, high credit quality loans.

"Private credit is always going to look to finance the highest-quality assets," Rubenstein said.

Affordability issues

While Rubenstein and Nuveen's Dimitrievich expect private credit deals across the power value chain, CreditSights' DeVries is skeptical that utilities will pursue that market for transmission projects.

"Long-haul transmission is the safest business around," he said. "Why, if you own a transmission line, would you ever go pay the high rate private credit wants?"

Customer bills are also a concern.

"Under no situation out there should a regulated ratepayer be funding rates that private credit charges to loan money," DeVries added. "If you're a management team, you have to protect your ratepayer."

Utility companies are laser-focused on affordability as opposition to data centers grows and rising bills attract the scrutiny of state regulators.

"The bar seems to have shifted" from no customer bill impacts to lower customer bills when it comes to added costs from data center development, Jefferies Managing Director Paul Zimbardo said in a January interview.