06 Mar, 2026

US mortgage rates may have hit bottom as war with Iran pushes up bond yields

By Brian Scheid

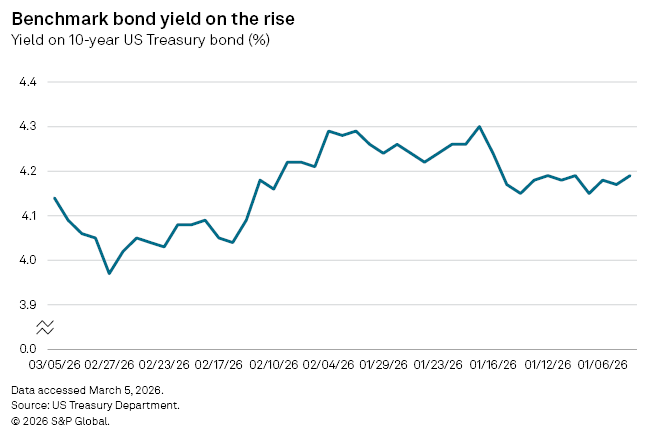

The benchmark US mortgage rate's dip below 6% was short-lived as the war with Iran pushed up US government bond yields, boosted economic uncertainty, and further muddled the Federal Reserve's path towards interest rate cuts.

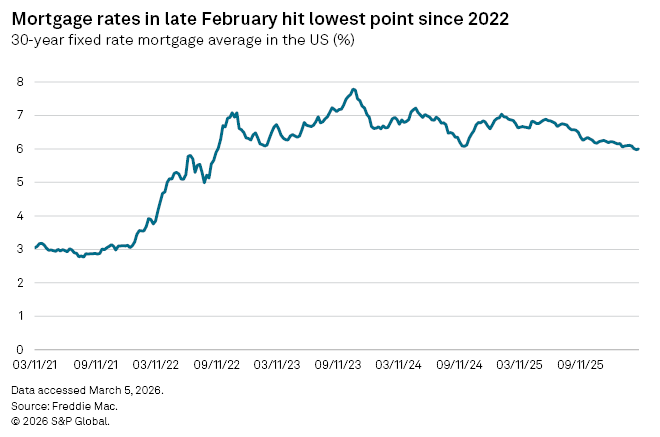

At the end of February, the 30-year fixed rate mortgage average fell to 5.98%, down from its most recent peak of 7.76% in November 2023 and the first time the rate was below 6% since September 2022. Mortgage rates are driven by a variety of factors, including: the direction of the 10-year US Treasury yield, economic conditions, monetary policy and market volatility.

Ongoing military conflict and the potential for higher inflation have upended the downward momentum in mortgage rates, and February could mark the low point for those rates as long as the Middle East war persists, market strategists said.

"Just as it appeared the spring selling season was going to get some much-needed help from lower rates, the conflict in Iran broke out, taking oil prices higher and with it, higher rates on the 10-year," said Steve Wyett, chief investment strategist at BOK Financial. "From here, the breadth and duration of the conflict will tell us if rates are going higher or can decline back to pre-conflict levels."

Since Feb. 28, when the US and Israel began joint strikes on Iran, the 10-year US Treasury yield has increased about 16 basis points. The 10-year yield settled at 3.97% on Feb. 27, its lowest level since October 2025.

While the launch of the US and Israeli military campaign against Iran has triggered higher oil prices and a rise in near-term inflation expectations, the reaction in the government bond market has been so far "tolerably benign," said Padhraic Garvey, head of global rates and debt strategy at ING.

The yield could rise another 16 basis points in the coming days, as inflation is expected to drift higher in the second quarter of this year, Garvey said.

Along with heightened inflation expectations, which could put the Fed's rate-cut plans on hold, the military conflict will further push up government deficits and pressure bond yields, which move in the opposite direction of prices, up further, said Molly Brooks, a US rates strategist with TD Securities.

"The length of this [war] really determines where everything is going," Brooks said.

The longer the war and the more disruptive it proves, the more oil prices will rise, pushing up inflation and, ultimately, government bond yields, as investors demand higher compensation for inflation risks, said Wyett with BOK Financial.

"At the same time, other factors such as higher defense spending, tariffs and deficits could also drive yields higher due to additional bond issuance," Wyett said. "This combination will keep yields elevated or push them higher, even if growth slows somewhat."

Near a floor

Notably, while geopolitical conflict can drive near-term volatility in bond yields, it does not guarantee a lasting shift in inflation expectations, and such shocks tend to be temporary, said Sam Williamson, senior economist at First American.

"While higher energy prices bear watching, it is still too early to know whether they will persist long enough to materially affect underlying inflation," Williamson said. "As a result, mortgage rates may be near a floor for now, given today's geopolitical climate."

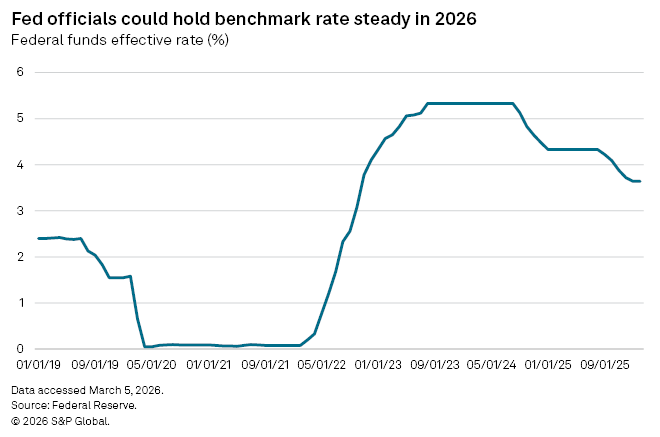

For now, the economic fundamentals do not support a significant decline in longer-term interest rates as the labor market has softened, but not meaningfully weakened, while inflation remains above the Fed's 2% annual growth target.

"

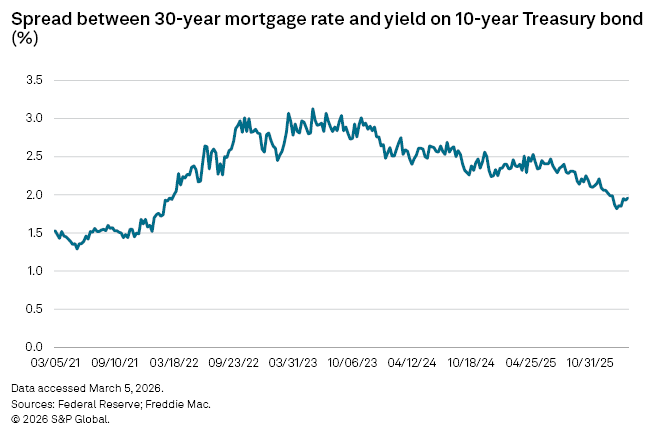

Mortgage rates could drift somewhat lower in the near term without Fed rate cuts due to the ongoing normalization in the mortgage spread, the difference between the 30-year mortgage rate and the 10-year bond yield, Williamson said.

That spread narrowed to about 1.8% in February, a four-year low.

"