31 Mar, 2026

US insurance regulators pulling back the curtain on private credit

By Hailey Ross

US insurance regulators are taking steps to better understand the industry's exposure to private credit as investments in the asset class grow.

Exposure to private credit has sparked investor concern across industries as the asset class experiences rising defaults and heightened investor redemptions. The National Association of Insurance Commissioners has made several changes to how it analyzes investment risk, including the formation of new task groups and changes to reporting requirements, to increase transparency and ensure regulators have the right tools to assess risk.

The changes will allow insurance regulatory oversight to be more "nimble and responsive," according to Carrie Mears, an investment specialist with the Iowa Department of Insurance and Financial Services.

Identifying risk

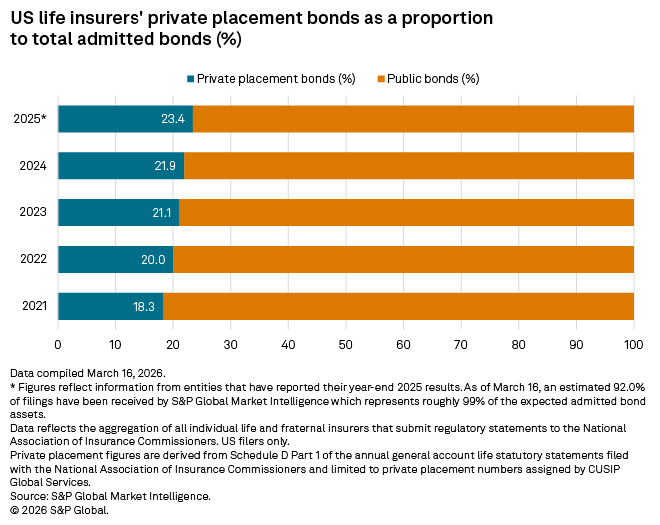

Because NAIC reporting data is categorized by asset class instead of the means of origination, it can be difficult to parse out exactly how much US insurers have invested in private credit. The best way to determine how much exposure underwriters have in private credit is to look at the prevalence of their holdings of loans and securities that have been assigned private placement number identifiers.

US insurers have been steadily increasing their investments in loans and securities with these private placement number identifiers over the past several years. Bonds with private placement numbers made up 23.4% of insurers' total admitted bonds in 2025, up from 18.3% in 2021.

The NAIC's existing system to identify private bonds holdings casts a considerably wider net to incorporate straight-forward investments that are freely tradable among institutional investors. This yields materially higher reported allocations that may not be fully indicative of heightened complex or liquidity risk. Moving forward it should be easier to analyze private credit exposure as the NAIC on March 5 adopted new reporting requirements that will provide more specific classification of the various private investments in an insurer's portfolio.

Transparency about how life insurers in particular manage their investment portfolios is a key priority for regulators this year, NAIC President Scott White told S&P Global Market Intelligence in March. Insurers reallocating assets into more complex, illiquid alternative assets or offshore in jurisdictions with different regulatory frameworks are issues about which US regulators need to be aware, Scott added.

Regulatory action

The specific types of assets that insurers independently classify as private credit vary, but generally include instruments such as asset-based finance, direct loans, certain types of privately placed corporate bonds and structured finance securities, and residential and commercial mortgage loans.

The NAIC in 2025 dramatically restructured its working groups and task forces focused on regulating insurers' investments. The new commissioner-level Invested Assets Task Force is supported by three working groups: the Investment Analysis Working Group, the Investment Designation Analysis Working Group and the Credit Rating Provider Working Group.

During its first meeting in March 2026, the Invested Assets Task Force received reports from its working groups and heard from PricewaterhouseCoopers on its proposed Credit Rating Provider (CRP) Due Diligence Framework, which is intended to establish a process to support the regulatory group's reliance on translating credit ratings to NAIC designations. The group was also given a presentation by Neuberger Berman regarding insurance companies growing investments in residential mortgage loans, which has also been a topic of focus for regulators as of late.

"Clearly that's not a new asset class ... but when we think of new, sometimes it has to do with just the materiality or growth rather than the asset itself," Mears said. "That's not something that we've really reviewed in a lot of detail for some time, and the types of exposures to residential mortgages that are kind of in that category are a little bit more widespread than probably what was initially contemplated there."

Mears said the group plans to start with education and then may review reporting structures associated with it, noting that residential mortgages have "been obviously a growth area for life insurers specifically that we'll investigate."

Also, as of the start of this year, the NAIC has the ability to challenge and override designations that stem from Nationally Recognized Statistical Rating Organization ratings of filing-exempt securities

Allocations continuing to rise

A significant proportion of the insurance industry plans to increase its allocation of private market investments in its portfolio over the next 12 months, according to Goldman Sachs Asset Management's annual global insurance survey published March 25.

The survey, which involved participation of 434 insurance company officers, showed that 35% of insurers expect to raise allocations in investment-grade private placements in the coming year. About a third of insurers intend to grow allocations in senior direct lending, while 25% anticipate increased allocations in private equity and infrastructure equity.

Insurers have the ability to be "opportunistic in credit cycles," Mike Siegel, global head of insurance asset management with Goldman Sachs, said in a release.

"Over the 15 years we have conducted this survey, private credit has continued to evolve into a broad and deep asset class and a core holding for insurers looking to address their yield and duration matching needs," Siegel said.

Theme

Location

Products & Offerings

Segment