26 Mar, 2026

Private credit outlook in Europe tempered by rising global risks

An optimistic forecast for private credit in Europe is tempered by the changing risk environment for global private credit markets.

After collecting a record fundraising haul in 2025, managers of Europe-focused private credit funds are eyeing a healthy pipeline of deployment opportunities as European governments pledge to boost spending on defense and infrastructure. Compared to the US, Europe's more fragmented credit market offers fund managers the chance to earn wider spreads on deals with similar levels of risk.

But clouds are gathering.

Globally, credit funds are facing intensifying scrutiny over their exposure to a software sector threatened by AI. Meanwhile, rattled retail investors are asking for their money back early, and a war in the Middle East is driving energy costs higher. Together, these factors could jeopardize Europe's economy and undermine the ability of private credit borrowers to stay current with loan payments.

"There are going to be losses in private credit. That just comes with the territory," David Scopelliti, global head of private debt at Mercer Inc., said in an interview.

For investors in European private credit, the pressures mounting on credit markets are likely to put more distance between the top-performing funds and the also-rans.

"COVID was a mini test of private debt. I don't think it was a full test of the cycle. I think we're going to see very big dispersion of returns from managers when we do hit an economic cycle or a credit cycle," Scopelliti said.

Fundraising momentum

Fundraising for Europe-focused private credit funds totaled a record $69.62 billion in 2025, up 29% from $53.94 billion in 2024, according to With Intelligence. That outpaced the 11% increase in global private credit fundraising in 2025.

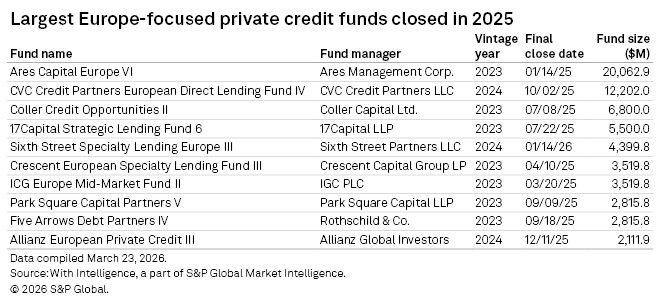

Europe's total was boosted by the closings of two mega funds pursuing direct lending strategies: Ares Capital Europe VI LP and CVC European Direct Lending IV, which closed at $20.01 billion and $12.17 billion, respectively. They represented two of the three largest private credit fund closings of 2025.

"Going into 2026, we're not seeing any slowdown in demand from the institutional [investor] community for private credit. It's been consistent, if not accelerating," Ares Management Corp. CEO Michael Arougheti said at a conference in December 2025.

Deployment opportunity

The State Board of Administration of Florida, the State Of New Jersey Police And Firemen's Retirement System and the Pennsylvania Public School Employees' Retirement System were among the major US-based institutional investors actively building out allocations to European private credit in 2025, according to With Intelligence, seeking both diversification and less-concentrated exposure to the tech sector compared to US private credit funds.

The potential for higher returns on private credit investments in Europe versus North America, the asset class's largest and most-developed market, is also an attraction.

"The thing that really matters in Europe is local origination capacity and being able to have boots on the ground and, to a certain extent, to operate in the same space as some of the local banks. That's why I think you have seen this premium," Emma Bewley, the London-based head of credit for Partners Capital LLP, said in an interview.

The shifting balance between European bank and nonbank lenders is another significant factor in the opportunity emerging for private credit. Banks are expected to cede more lending activity to private credit funds as they implement the post-global financial crisis risk-management reforms of Basel III and Basel IV.

In a report issued by Apollo Global Management Inc. in June 2025, the global alternative asset manager estimated nonbank lending accounted for just 12% of corporate financings in Europe, compared to 75% in the US — an indication of just how far private credit could stretch in Europe in the coming years, according to the report.

"Banks still hold an attractive market share in Europe, but that paradigm is shifting, and private credit is becoming a more reliable source of capital for financing," Nayef Perry, head of direct credit for Hamilton Lane Inc., told S&P Global Market Intelligence.

Private credit fund managers also expect European governments' plans to increase spending on defense and infrastructure to generate significant deal flow.

"We're really seeing it in Europe with defense spending and data and power supply. And so the capital that's required is more than the banking system can provide," Apollo CFO Martin Kelly said in February.

Risk backdrop

While the fundamentals underpinning private credit's growth story in Europe remain in place, heightened risk concerns are curbing expectations for fundraising and deal activity in the near term.

"More risk means more measured investing," Vincent Calcagno, head of US growth at financial services firm Ocorian Ltd., said in an interview.

Patrick Schoennagel, co-head of investment bank Houlihan Lokey Inc.'s capital solutions group in Europe, said much of the "noise" around private credit is emerging from retail funds serving wealthy individual investors, including funds operated by Blue Owl Capital Inc. and Blackstone Inc., which experienced substantial outflows early 2026 as nervous investors asked for their money back early. The failures in 2025 of two companies with ties to the US auto industry, First Brands Group LLC and Tricolor Holdings LLC, sparked broader concerns about credit quality and the potential for more defaults.

Private credit exposure to the software sector is another concern, with recent advances in AI poised to undermine some companies' business models and valuations. A more immediate concern in Europe may be the war in the Middle East raising energy costs, potentially slowing economic growth and the pace of private equity-backed M&A, a significant source of deal activity for private credit, Bewley at Partners Capital said.

Additionally, while it may not loom as large as other factors, the increased competition that comes with accelerating growth poses its own risks for private credit.

"When things get really sporty and competitive, [fund managers] might stretch a little bit on leverage or reduce their price or agree to looser covenants or whatever, there could be erosion of credit quality in some individual lending decisions. But overall, when I read it that private credit is this time bomb waiting to explode and take down the global economy, from my seat here in Europe, I just don't see reckless behavior," Schoennagel said.

Manager selection

Whether or not the cumulative risks translate into higher default rates for European private credit funds, souring sentiment is likely to slow their growth trajectory, said Ishar Sawhney, a senior analyst for hedge fund Ironshield Capital Management LLP.

"There will be less capital raising [for direct lending funds] and more scrutiny on managers going forward," Sawhney said.

The senior analyst predicted a "small credit crunch" as private credit jitters ripple outward from retail funds. Apollo's recently announced plan to update net asset values for its private credit funds on a monthly basis, meant in part to soothe investor concerns, could also draw more attention to markdowns on existing loans.

"As people see markdowns, they'll get more wary on where they're putting their capital," Sawhney said.

Bewley expected a period of relatively free lending to be followed by "higher default rates over a prolonged period," although she said it would not approach the levels seen during the global financial crisis. But for savvy managers, particularly those that have just raised funds, turbulence in credit markets could also create an opportunity to lend at higher spreads.

Uncertainty is likely to produce wider dispersion in fund performance, she said, underlining the importance of manager selection for private credit investors.

"It could be a really attractive vintage in credit. The next two years could provide some really interesting opportunities," Bewley said.

With Intelligence is a part of S&P Global Market Intelligence.

Theme

Location

Products & Offerings

Segment