18 Feb, 2026

Zurich's Beazley approach marks latest move in rush to enter Lloyd's of London

By Ben Dyson

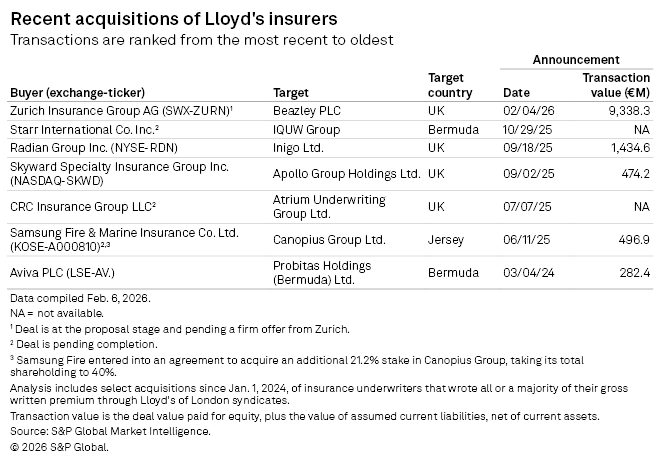

Zurich Insurance Group AG's £8 billion plan to buy specialty insurer Beazley PLC is the latest example of insurers' and investors' growing interest in entering Lloyd's of London.

Buying Beazley would make Zurich, which lacks a Lloyd's presence, the biggest player in the market. Beazley's Lloyd's managing agent, Beazley Furlonge Ltd., is the largest in the market by gross written premium. Business written at Lloyd's accounted for 77.7% of Beazley's total insurance revenue in 2024, according to the insurer's annual report.

Zurich is not alone in seeing the allure of Lloyd's. A flurry of Lloyd's insurer acquisitions was announced in 2025, and the vast majority of the buyers were US-based. The most recent of these was Starr International Co. Inc.'s planned acquisition of IQUW Bermuda Holdings Ltd. Excluding Zurich's attempt to buy Beazley, acquirers have spent at least €2.69 billion on Lloyd's insurers over the past two years.

Through the front door

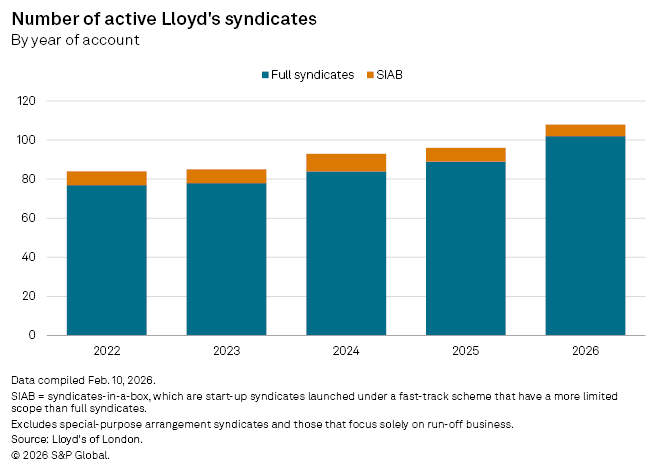

At the same time, there has been a jump in the number of new syndicates being established at Lloyd's. The market started 2026 with 108 active syndicates, 12 more than at the beginning of 2025. This was the biggest annual increase in syndicate numbers in at least five years.

Some of these launches were companies expanding an existing Lloyd's presence, such as Ariel Re Ltd.'s Syndicate 2006 and Mosaic Insurance Holdings Ltd.'s Syndicate 2610.

But many were from companies new to Lloyd's. Specialty insurer and reinsurer Convex Group Ltd., which launched in 2019, now has a Lloyd's presence with Syndicate 1984, which started underwriting in April 2025.

A new class of trade credit syndicates has emerged, triggered by S&P Global Ratings' upgrading its financial strength rating of Lloyd's to AA- in December 2023. Syndicates from two of the big three trade credit insurers, Atradius NV and COFACE SA, were among the newcomers.

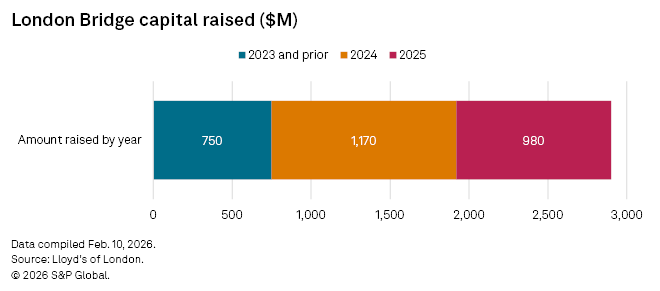

There has also been continued growth in the Lloyd's London Bridge investment platform. This allows institutional investors to gain exposure to Lloyd's in a similar way to how they back insurance-linked securities such as catastrophe bonds and sidecars.

London Bridge had raised $2.9 billion as of the end of 2025, Rachel Turk, chief of market performance at Lloyd's, said at a Fitch Ratings insurance conference in January 2026. The platform had raised $1.92 billion as of the end of 2024.

Turk said she does not envisage a slowdown in money coming into London Bridge. "The appetite from institutional capital is absolutely immense right now," she said. "There is a lot of capital knocking on the door wanting to come in and match to the risk that's there."

Attractions new and old

The traditional attractions of Lloyd's, such as its financial strength and network of global licenses, are combining with recent trends to lure acquirers and investors.

Lloyd's reported returns on capital above 20% for both 2023 and 2024. The 2025 number, while not yet released, is likely to be similar to the previous two years, Turk said at the Fitch event.

Lloyd's syndicates have consistently reported a collective combined ratio below 100% for the past four years and look set to deliver a fifth in 2025. Almost all Lloyd's managing agents, which act as holding companies for one or more syndicates, made an underwriting profit in 2024.

While softening prices could erode future profitability, Turk said the market "could turn on a knife edge" if there are sufficient large losses. Also, while return on capital has improved, the current long-term average of below 10% "is not particularly enticing at this moment in time," according to Turk. She added: "I think the return on capital is partly what's driving the fact that it is not inevitable that we move into a completely soft market."

Lloyd's return on capital of 25.3% in 2023 and 21.0% in 2024 took the seven-year average to 7.6%, according to the insurance and reinsurance marketplace's annual report.

Softening prices in specialty insurance and reinsurance lines are curtailing organic growth prospects while also freeing up excess capital that could be used for M&A. Specialty insurance, along with insurance intermediation, is a focal point for acquirers and investors.

While specialty prices are falling, trends such as geopolitical tensions, cyberattacks and data center construction for AI indicate more demand for specialty cover.

"The inherent value of the distribution models as well as specialty underwriting models remain compelling, which is probably why Zurich's approach for Beazley may not be the only situation we see in 2026," Bhaven Pathak, partner and head of UK and Europe at specialist investment bank Insurance Advisory Partners, said on a Market Intelligence webinar Feb. 2.