25 Feb, 2026

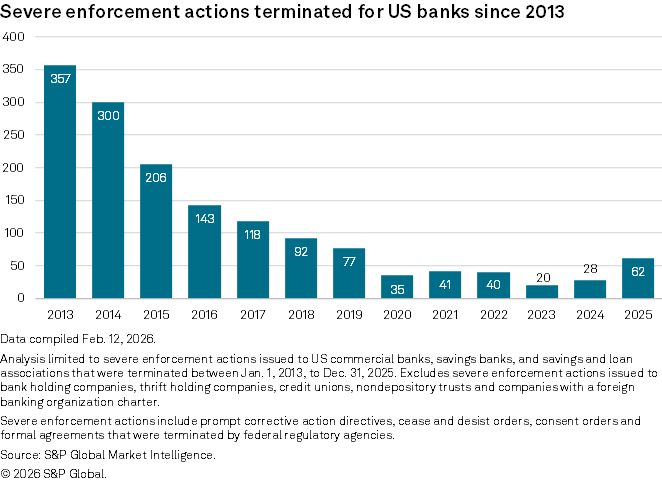

Severe enforcement action terminations reach 6-year high in 2025

By Rica Dela Cruz and Ayesha Shahbaz

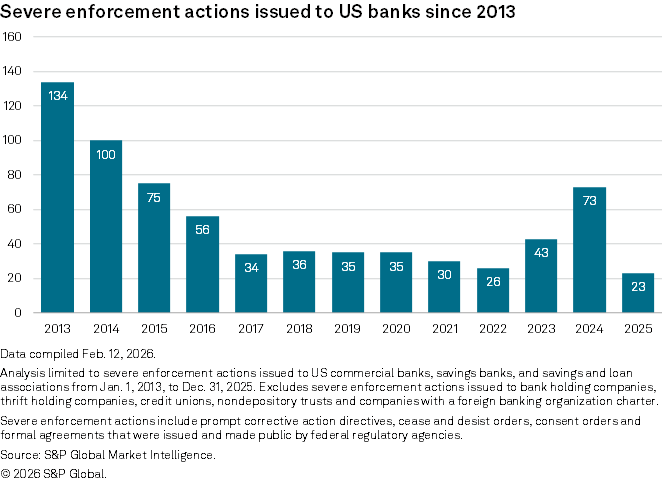

Severe enforcement action issuances plummeted to a record low while terminations surged in 2025 as federal banking regulators shifted supervisory priorities.

US banking regulators ended 62 severe enforcement actions during the first year of Donald Trump's second tenure as president, the highest rate since 77 in 2019, according to S&P Global Market Intelligence data. Terminations also greatly outpaced issuances, which came in at 23 for the year, the lowest annual level since at least 2010.

The large number of terminations happened as bank regulators focused their supervisory priorities on financial risks and de-emphasized more subjective topics like reputation risk, process and management.

"There has been a strong shift to focusing on material financial harm as a reason for bringing enforcement activities and not penalizing people for technical compliance failures or inadvertent immaterial oversight," said Matthew Bisanz, a partner at Mayer Brown LLP.

Industry experts expect enforcement action terminations to continue outpacing issuances in 2026. The uptick in terminations has come as regulators turn their attention to outstanding orders that do not align with their focus on material financial risk, they said.

"Regulators have focused on cleaning up older enforcement actions, especially if these items were not aligned with the current regulatory focus," John Mackerey, Morningstar DBRS' senior vice president and sector lead of North American financial institutions ratings, wrote in an email.

Regulators are also ending more informal actions that do not align with their supervisory priorities. For example, Federal Reserve Vice Chair for Supervision Michelle Bowman in a February memo instructed staff to review all open matters requiring attention (MRAs) and matters requiring immediate attention (MRIAs) and potentially downgrade those that do not meet severity standards to a nonbinding supervisory observation, according to an internal Fed memo viewed by Market Intelligence.

MRAs and MRIAs are confidential agreements between regulators and a bank requiring the bank to remediate an issue. Regulators may opt to use these more than enforcement actions.

"Some of the priorities also shift to, 'Well, instead of doing an enforcement action, we're just going to make the people fix it, or we're going to have them commit to fix it instead of bringing an enforcement action,'" Bisanz said. As a result, the level of bank enforcement action issuances in 2026 could be "flat to about the same as last year," Bisanz said.

However, regulators have introduced rules and guidance that will limit their ability to issue new orders. For example, the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corp. in October 2025 introduced a rule seeking to limit their authority to issue MRAs, MRIAs and enforcement actions by defining "unsafe and unsound practices" as practices or acts that would hurt the bank's financial condition or cost the Deposit Insurance Fund.

Similarly, the Fed's Bowman instructed supervisors in a November 2025 memo to limit the use of MRAs and MRIAs to only addressing "shortcomings" that rise above the level of nonbinding supervisory observations. The agency plans to release more specific guidance on that soon.

It is also working on reviewing its definition of "unsafe and unsound practices" to better limit enforcement action issuances to only material financial risks.

Light at the end of the tunnel

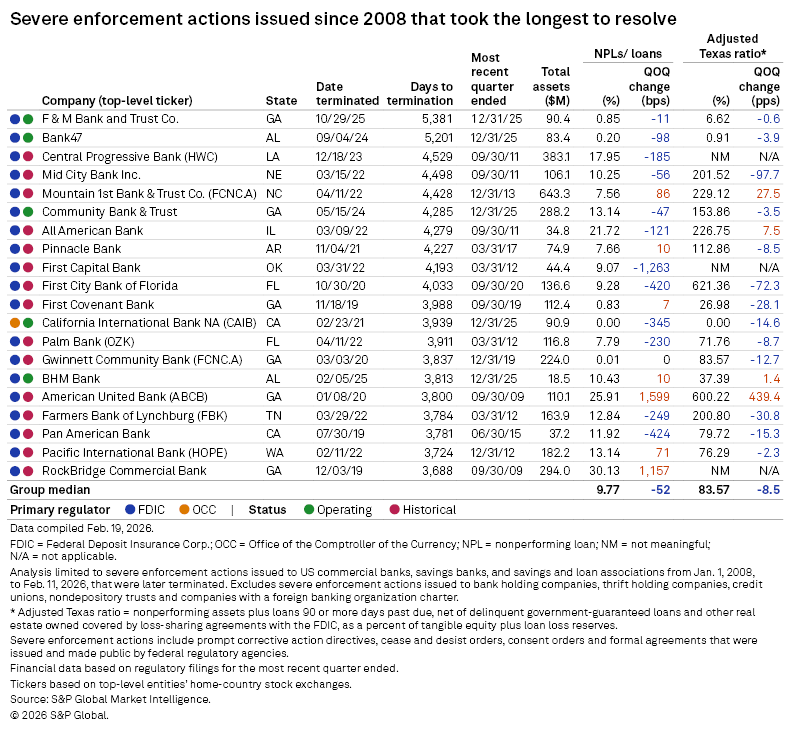

Some of the longest-pending severe enforcement actions came to an end in 2025.

A consent order issued against Manchester, Georgia-based F & M Bank and Trust Co. in 2011 was terminated after 5,381 days, making it the longest-pending severe enforcement action issued since 2008. A consent order handed out to BHM Bank, previously known as Alamerica Bank, in 2014 also ended in 2025 after 3,813 days.

A handful of severe enforcement actions issued to large banks were also resolved in 2025. Regulators terminated four orders against Wells Fargo & Co.'s bank subsidiary and ended one order against Citibank NA. Wells Fargo's $1.95 trillion asset cap was lifted midyear.

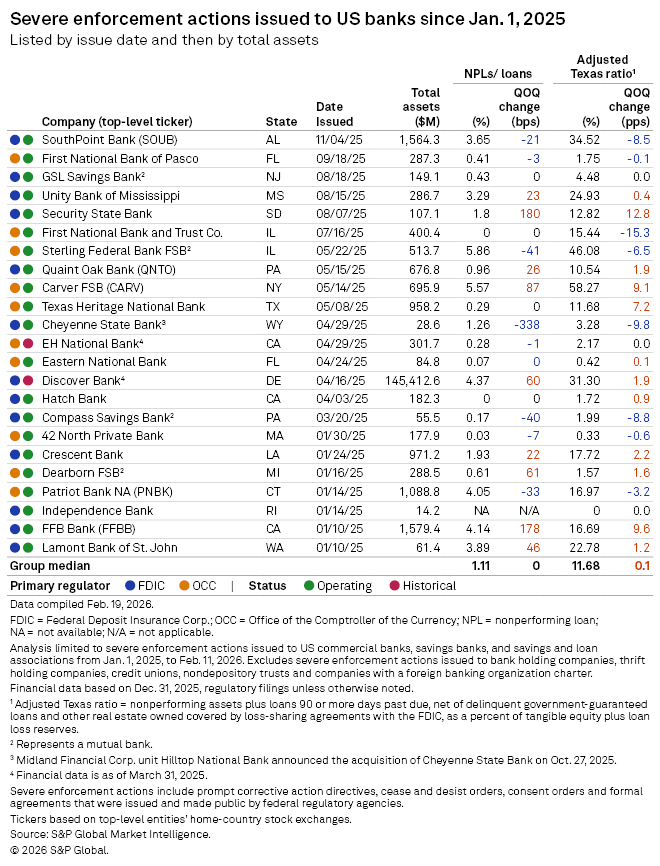

Small banks dominate the list

All but one of the 23 severe enforcement actions issued in 2025 went to community banks. The exception was a consent order issued by the Federal Reserve to Discover Bank before its sale to Capital One Financial Corp. The order required Discover to pay a $100 million fine for overcharging certain interchange fees between 2007 and 2023.

Severe enforcement actions against banking-as-a-service community banks slowed, with just two actions in 2025 versus six in 2024. The banking-as-a-service community banks that received such actions in 2025 were Patriot Bank NA and Quaint Oak Bank.