05 Feb, 2026

NAV monitor: US REITs end January at median 16.2% discount to net asset value

By Arpita Banerjee and Ronamil Portes

This Data Dispatch is updated monthly and was last published Jan. 8. The analysis includes equity real estate investment trusts that trade on the Nasdaq, NYSE or NYSE American with market capitalizations of at least $200 million and can offer insight into how the Street is valuing different property sectors. While valuations within the portfolio of publicly traded REITs might not match all privately owned properties, the public markets can often be a leading indicator for potential future property pricing. That insight is particularly helpful when there is little price discovery in the market due to a lack of transactions.

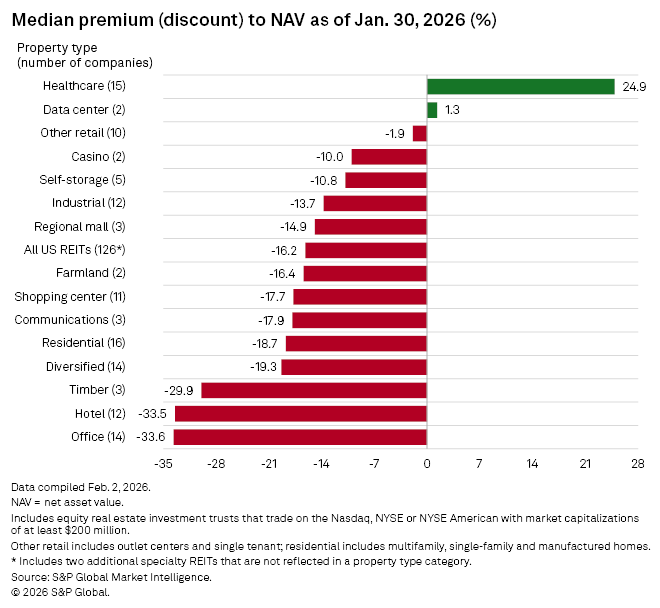

Publicly listed US equity real estate investment trusts with market capitalizations of at least $200 million closed January trading at a median 16.2% discount to consensus estimates for net asset value per share, 2.1 percentage points down from a median 18.3% discount Dec. 31, 2025, according to S&P Global Market Intelligence data.

The office sector recorded the steepest median discount to net asset value (NAV) at 33.6%, followed by the hotel sector at 33.5%. The timber sector, which traded at the steepest discount for the past two months, ended January with a median discount to NAV of 29.9%.

Healthcare REITs posted a median 24.9% premium, compared with a 26.4% premium as of Dec. 31, 2025.

The data center sector's valuation increased, closing Jan. 30 at a median 1.3% premium to NAV, compared with a median 5.5% discount to NAV on Dec. 31, 2025.

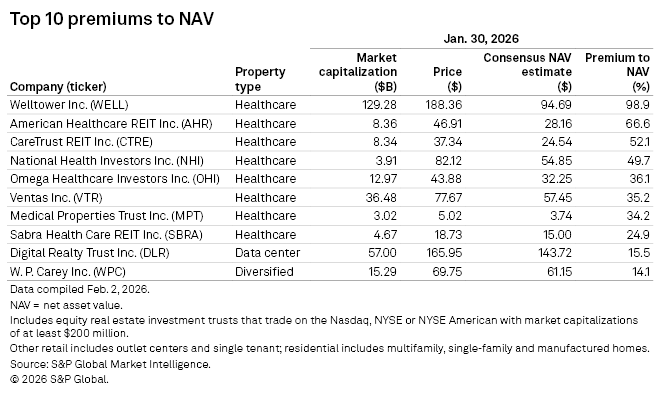

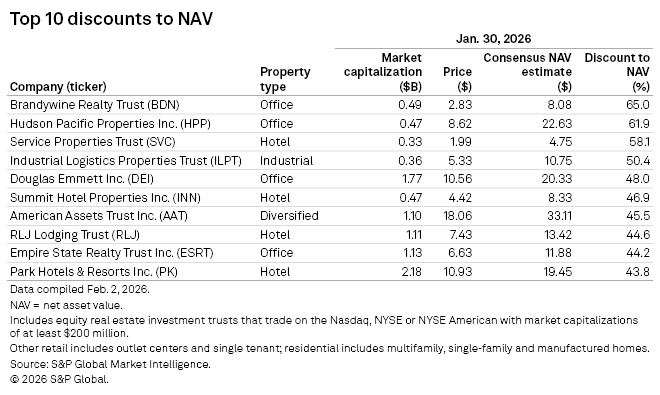

Largest discounts

Of the 10 US REITs in the analysis trading at the largest discounts to NAV, four were office REITs and four were hotel REITs.

Office REIT Brandywine Realty Trust logged the largest discount to NAV, closing Jan. 30 at $2.83 per share, 65.0% below the consensus NAV estimate of $8.08 per share. Hudson Pacific Properties Inc., also an office REIT, claimed the second position, trading at 61.9% discount to NAV as of Jan. 30.

The other office-focused REITs on the list were Douglas Emmett Inc. and Empire State Realty Trust Inc., trading at discounts of 48.0% and 44.2%, respectively.

Hotel REIT Service Properties Trust was third, trading at $1.99 per share Jan. 30, 58.1% below the consensus NAV estimate of $4.75 per share. Other hotel REITs Summit Hotel Properties Inc., RLJ Lodging Trust and Park Hotels & Resorts Inc. closed January at discounts to NAV of 46.9%, 44.6% and 43.8%, respectively.

– Download an Excel template with data featured in this story.

– Set email alerts for future Data Dispatch articles.

– Read some of the day's top real estate news and insights from S&P Global Market Intelligence.

Largest premiums

Healthcare REITs continued to dominate the list of the 10 REITs trading at the highest premiums to NAV, with eight of them belonging to the sector.

Welltower Inc. led the group, closing Jan. 30 at $188.36 per share, 98.9% above the consensus NAV estimate of $94.69 per share. American Healthcare REIT Inc. came in second with a 66.6% premium to NAV, followed by CareTrust REIT Inc., at a 52.1% premium to NAV.

Other healthcare REITs on the 10 list were National Health Investors Inc., Omega Healthcare Investors Inc., Ventas Inc., Medical Properties Trust Inc. and Sabra Health Care REIT Inc.

The highest premiums list included a single data center REIT: Digital Realty Trust Inc., which traded at a 15.5% premium to NAV.