27 Feb, 2026

Market dispersion widens as mega-caps stumble, equal-weight index takes lead

By Brian Scheid

Investor unease around the likelihood of an AI bubble has weakened mega-cap technology stocks' long hold on the S&P 500.

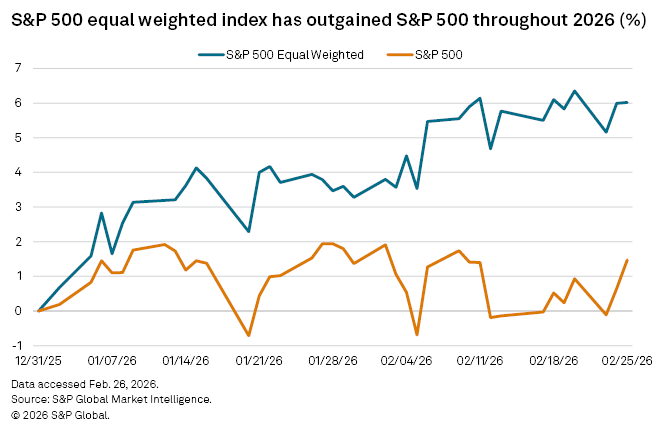

By a more than 4-to-1 margin, the S&P 500 Equal Weighted index has out-earned the S&P 500 in 2026 so far. The equal-weight index, where companies are allocated an equal fixed weight, is up more than 6% since the end of 2025 compared to a 1.5% rise in the S&P 500, where stocks are weighted by market capitalization.

This outperformance is a sign of a more encompassing rise in stocks beyond the mega-cap tech sector following a period where the S&P 500's performance was largely reliant on the Magnificent Seven stocks.

"The trades, particularly in large-cap tech, became very crowded and disproportionately dictated market direction," O'Connor said. "And at times, the underlying market-cap weighted index performance belies what is really going on under the surface."

This recent trend is a reversal. The S&P 500 has significantly outgained its equal-weight counterpart for the past three years, rising 24.2% in 2023 to the S&P 500 Equal Weight's 11.6%, for example. The equal-weight index last outgained the S&P 500 in 2022 when it lost about 13.1% through the year, compared to the 19.4% decline for the S&P 500.

The equal-weight index is outperforming the S&P 500 as "mega-cap leadership has been fading," said Bret Kenwell, an investment and options analyst at eToro.

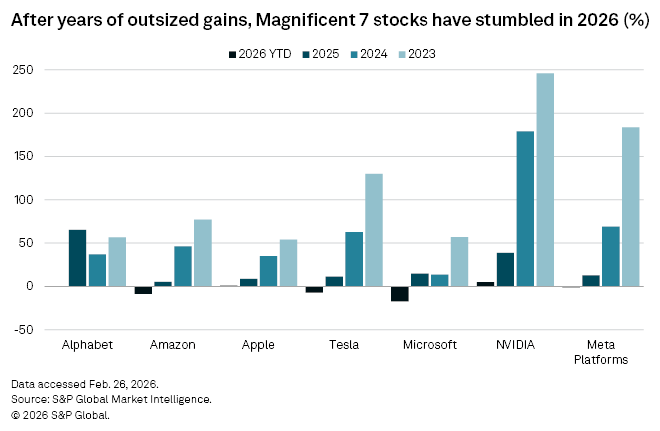

The Magnificent Seven — Google LLC, Amazon.com Inc., Apple Inc., Tesla Inc., Microsoft Corp., NVIDIA Corp. and Meta Platforms Inc. — have significantly outperformed the broader S&P 500 during its current bull run, but have lagged for much of 2026. On average, these seven stocks have declined more than 4% on the year, led by Microsoft, which is down more than 17% after rising more than 14.7% in 2025.

These stocks have been weighed down in recent months by AI-related concerns, including soaring capital expenditures without matching revenue growth, potentially inflated valuations, cash flow concerns and regulatory and political pressure.

"AI ebbs and flows between being a headwind and a tailwind for the [Magnificent Seven]," said Kenwell with eToro. "At times, investors bid these stocks higher in hopes that AI will fuel the next wave of growth. At other times, the enormous capex required for the buildout gives investors pause."

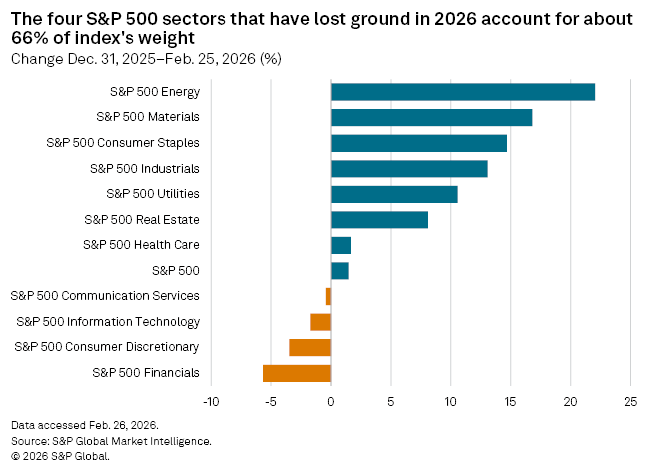

The decline in Magnificent Seven stocks, which make up roughly one-third of the S&P 500's overall weight, has caused the S&P 500 to lag the equal-weight index. In addition, declines in the index's communication services, information technology, consumer discretionary and financials sectors have caused additional lags as those sectors account for about 66% of the S&P 500's weight.

Investors now are seeking returns in underinvested areas, a healthy shift in market behavior, O'Connor with Liquidnet said.

"A reversion to the mean is in order, and appears to be playing out in equal-weight outperformance," O'Connor said.

The broadening of the rally is an overall positive as long as overall participation does not weaken, said Paul Schatz, founder and president of Heritage Capital. Still, it is unlikely that a rally in equities is sustainable if mega-cap and other tech stocks continue to decline.

"The bull market cannot survive without technology," Schatz said. "Tech does not have to lead, but it can't be bringing up the rear as the caboose. It needs to at least be in the middle of the hit parade."