25 Sep, 2025

Credit union liquidations climb to 7-year high as asset quality slips

By Zoe Sagalow and Gaby Villaluz

Credit quality blips and profitability slips have led to the highest number of credit union liquidations in seven years.

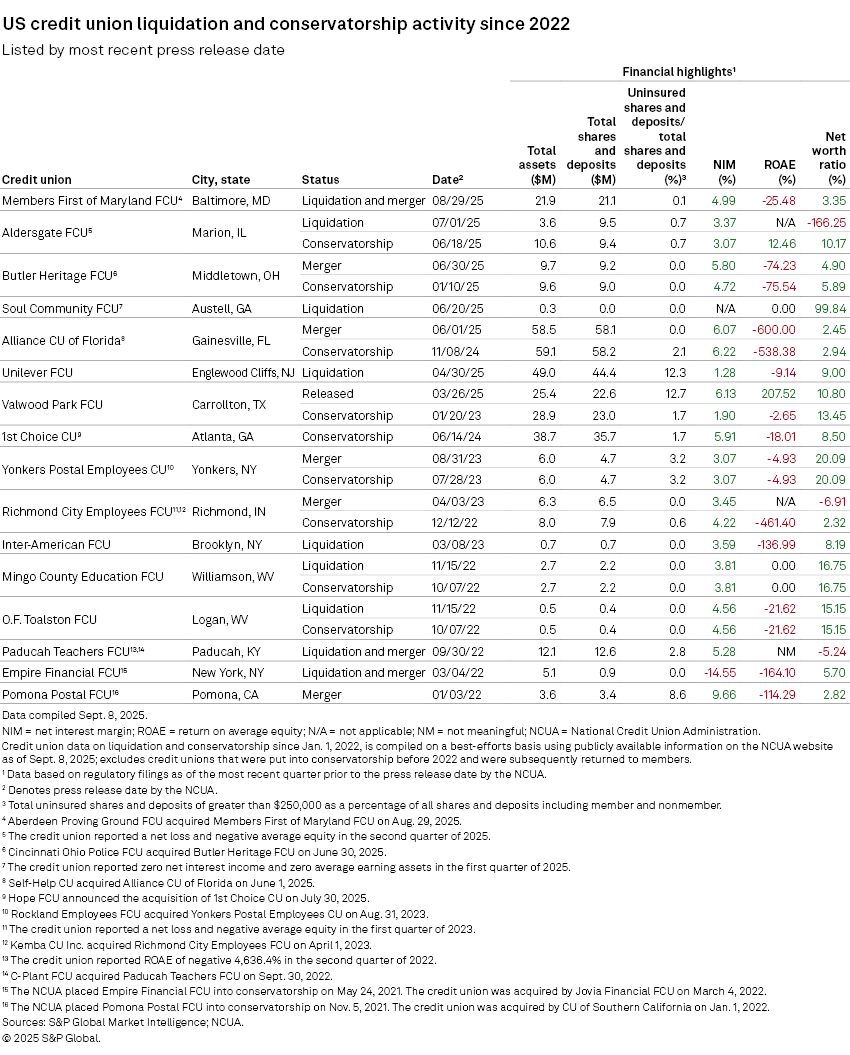

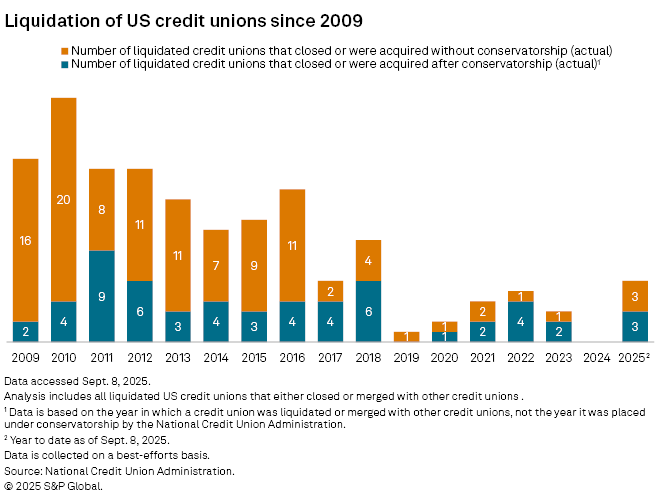

Six credit unions have failed this year, marking a sharp increase from zero failures in 2024 and the most since 2018, when 10 credit unions were liquidated. The uptick came after a quiet first quarter, with all six occurring within the four-month span between April 30 and Aug. 29.

Fraud, mismanagement, and Bank Secrecy Act compliance issues are the most common reasons that credit unions fail, with fraud being the most common, former National Credit Union Administration (NCUA) Chairman Todd Harper told S&P Global Market Intelligence in an interview. While the health of the overall credit union industry remains strong, individual credit quality and profitability struggles led to the demise of most of the credit unions that failed so far this year, an analysis by S&P Global Market Intelligence found.

Credit quality and profitability issues can arise when an institution pushes hard for growth and forsakes some due diligence.

"Sometimes when you're small, you push really hard ... so you get more loans, and you get more earnings," Charley McQueen, president and CEO of McQueen Financial Advisors, said in an interview. "Sometimes you're attracted to making ... poor loan decisions."

Among the six credit unions liquidated this year, the largest had only $58.5 million in assets. The liquidation trend could continue as the competitive environment intensifies.

"To me, it's a bit more remarkable that it's not more," Peter Duffy, managing director at SRM Inc., said in an interview. "Going forward, there may be more of a story than there is now because the operating environment is not going to get easier. It's only going to get more competitive."

Increasing industry headwinds — such as intense competition, regulatory requirements and the rising cost of technology — are driving consolidation and "those drivers are all accelerating," Duffy added.

Aside from the uptick in failures, the overall health of the credit union industry appears strong.

The number of credit unions with 4 and 5 CAMELS ratings, the lowest score, dropped by 13 in the six months between the fourth quarter of 2024 and June 30. This was the largest reported drop since the total declined by 30 between the fourth quarter of 2020 and the fourth quarter of 2021, according to the NCUA.

Credit problems

The latest liquidation came after facing deteriorating credit quality for several years. Baltimore-based Members First of Maryland FCU, which was liquidated Aug. 29 without first going into conservatorship, had a delinquent loan to total loan ratio of 1.43% in the second quarter, its last quarter of operations, compared to the industry median of 0.90% during that period.

The credit union's other asset quality measures, including delinquent loans to net worth and delinquent loans to reserves, were also elevated in the second quarter, at 19.26% and 97.92% respectively, and for several years prior.

Loans and lines of credit secured by first lien 1- to 4-family real estate made up the biggest portion of Members First of Maryland's loans at June 30 at 58.24%, up from 51.31% in the linked quarter and 36.72% year over year.

The second-largest lending segment was used vehicle loans, making up 28.33% at the end of the second quarter, down from 33.93% at the end of the first quarter and 44.84% at the end of the second quarter of 2024.

Its return on average equity (ROAE) was negative 25.48% at the end of the second quarter, down from negative 16.98% as of the end of the first quarter. This was much weaker than the industry median ROAE of 6.58% in the second quarter.

Members First of Maryland's net worth ratio was 3.35% at the end of the second quarter, down from 3.47% at the first quarter. The NCUA considers below 6% to be undercapitalized.

Marion, Illinois-based Aldersgate FCU, which was liquidated July 1 after being in conservatorship, failed after signs of credit quality trouble suddenly appeared. Its delinquent loans to total loans ratio jumped to 28.98% in the second quarter, its last quarter of operations, after having zero delinquencies for at least three years prior. Most of Aldersgate's loans were in the category of other unsecured loans, which are personal loans without collateral.

Its net worth ratio also deteriorated in the second quarter to negative 166.25%, a sharp drop from above 9% in the four prior quarters.

Alliance CU of Florida, which was liquidated June 1 after being put into conservatorship in November 2024, also had a higher-than-average delinquent loans to total loans ratio at 3.27% in the first quarter, its last quarter of operations. That asset quality measure has remained above 2% since the second quarter of 2023.

The majority of Alliance's loan portfolio consisted of used vehicle loans, 33.54%, and new vehicle loans, 18.93%.

The credit union also had weak profitability, with an ROAE of negative 600% in the first quarter. Its ROAE and ROAA had been in negative territory since the third quarter of 2023.

Profitability problems

Middletown, Ohio-based Butler Heritage FCU was liquidated June 30. It had weak income compared with its average equity, with an ROAE of negative 74.23% as of the first quarter of 2025. Its ROAE and ROAA were both negative since the first quarter of 2024.

In addition, it was undercapitalized, with a net worth ratio of 4.90%.

After being in conservatorship since January, Butler Heritage was liquidated and merged with Cincinnati Ohio Police FCU in June. Before the conservatorship, a group of Butler Heritage members battled with the board of the credit union over alleged management problems and a planned merger that a judge eventually stopped.

The first credit union that was liquidated this year, Unilever FCU, ended an almost two-year streak of no liquidations. Englewood Cliffs, New Jersey-based Unilever, which was liquidated April 30 without going into conservatorship, had weak profitability metrics with a net interest margin of 1.28% at the end of the first quarter, prior to its liquidation in April, well below the median of 4.26% for all credit unions in that quarter.

Unilever's efficiency ratio was 154.8% in the first quarter, more than twice as high as the industry median for the quarter of 79.76%.

Its ROAE and ROAA were also negative since the second quarter of 2023.

Soul Community FCU

An outlier was Austell, Georgia-based Soul Community FCU, which was liquidated June 20 without going into conservatorship about six months after opening its doors in December 2024. The fledgling credit union was found to be "insolvent and ... operating in an unsafe and unsound manner," the NCUA said in its announcement. As of March 31, it had $309,000 in assets and a net worth ratio of 99.84%, substantially above the NCUA's minimum of 6% to be considered "adequately capitalized."

Sometimes young credit unions fail because they do not follow their business plans or have management issues, former NCUA head Harper said in an interview. Sometimes new credit unions's business plans can be overly optimistic, and their actual results do not end up meeting expectations, he added.

"My experience is that small credit unions can and do fail and are more likely to fail because there are greater risks there," Harper said.