13 Jun, 2025

US banks' loss allowance levels hold steady amid ongoing uncertainty

By Harry Terris and Gaby Villaluz

Loss reserve levels for US banks remained stable despite tariff policies creating uncertainty in the economic outlook.

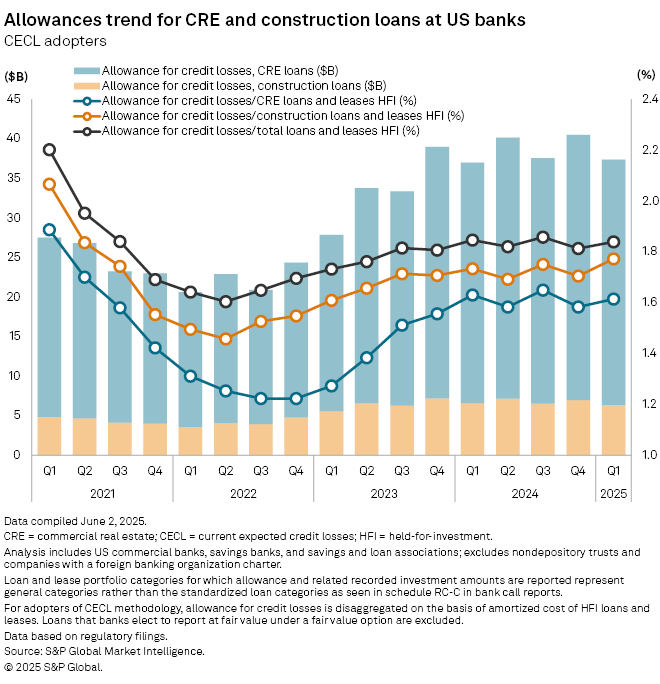

Credit loss allowances as a percentage of loans across banks moved up 3 basis points sequentially to 1.84% in the first quarter, partially reversing a decline the quarter before, according to S&P Global Market Intelligence data. The ratio of 1.86% in the third quarter of 2024 remains a recent peak.

The pattern was similar for commercial real estate (CRE) loans. An increase of 3 basis points to 1.61% in the first quarter of 2025 left the ratio below a recent peak of 1.65% in the third quarter of 2024.

Weekly data from the Federal Reserve on domestically chartered banks showed allowance ratios ranging from 1.73% to 1.77% so far this year through May 28, after seasonal adjustment.

In mid-quarter updates, some bank executives said that the outlook has recovered after President Donald Trump's April tariff announcements. However, JPMorgan Chase & Co. Chairman and CEO Jamie Dimon forecast that implemented tariffs would translate into lower employment and higher inflation in the coming months.

Wells Fargo & Co. does not expect much loan growth for the rest of the year. "The uncertainty that's been there has caused people to pause a little bit on investment, on inventory build, to being really thoughtful about sort of borrowing, particularly given how expensive it can be," CFO Michael Santomassimo said June 10.

Fifth Third Bancorp said deterioration in the macroeconomic outlook that it has used for credit provisioning since March could prompt an allowance build in the second quarter.

|

|

– Set email alerts for future data dispatch articles. – Download a template to generate a bank's regulatory profile. – Download a template to compare a bank's financials to industry aggregate totals. |

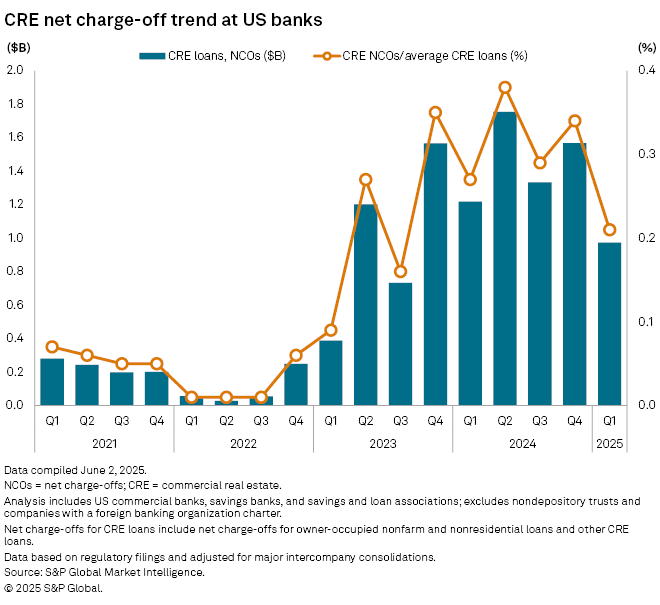

CRE net charge-offs

Net charge-off (NCO) ratios, or the annualized amount of loans banks conclude are uncollectible as a percentage of loans, dropped 13 basis points sequentially to 0.21% for CRE in the first quarter. The move continued a jagged series of ups and downs since the ratio came off minimal levels in 2022.

CRE — the office segment in particular — has been the focus of credit concerns for some time, though many banks have expressed confidence in reserve levels and some have pointed to emerging opportunities for lending in the sector.

"Real estate pipelines are beginning to pick up as multifamily developers look out and see opportunities to begin thinking about development," Regions Financial Corp. President, CEO and Chairman John Turner Jr. said June 10, despite an overall "wait and see" posture among borrowers.

"You'll continue to see office decline a bit, but there's opportunities in other parts of" the CRE book, Wells Fargo's Santomassimo said.

CRE stress is unlikely to worsen unless the job market worsens, analysts at BofA Global Research said in a June 4 note. "We note that banks have taken significant actions to build loan loss reserves for expected losses primarily tied to office CRE that we expect to play out over the next several quarters/few years."

|

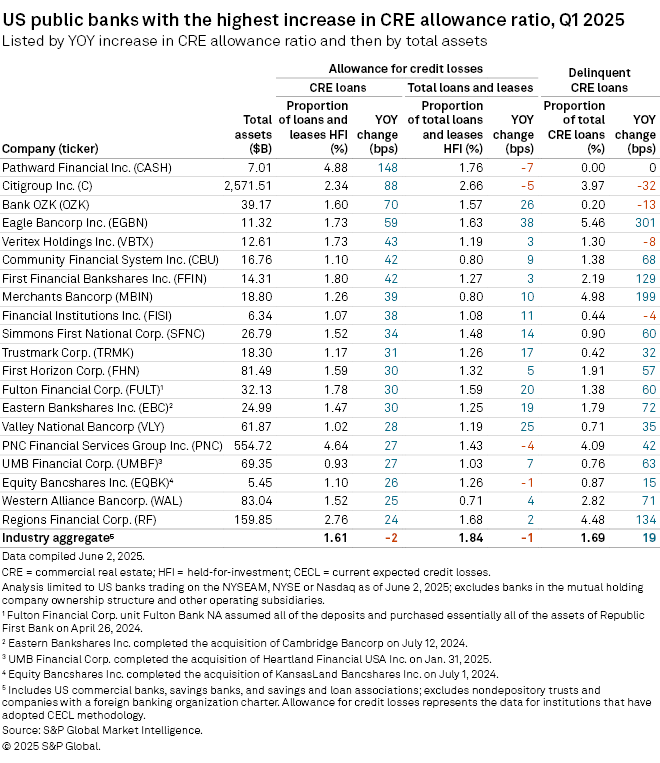

Biggest CRE builds

Among the 20 banks with the biggest year-over-year increases in CRE allowance ratios, delinquencies as a percentage of loans increased the most at Eagle Bancorp Inc. The bank's delinquency rate for CRE loans rose 301 basis points year over year in the first quarter to 5.46%.

Eagle Bancorp reported office loan downgrades and reserve builds in the first quarter, driving its shares lower.

|