1 Oct, 2024

FinReg Europe: UK eases Basel rules; EU warns banks of systemic risks

–

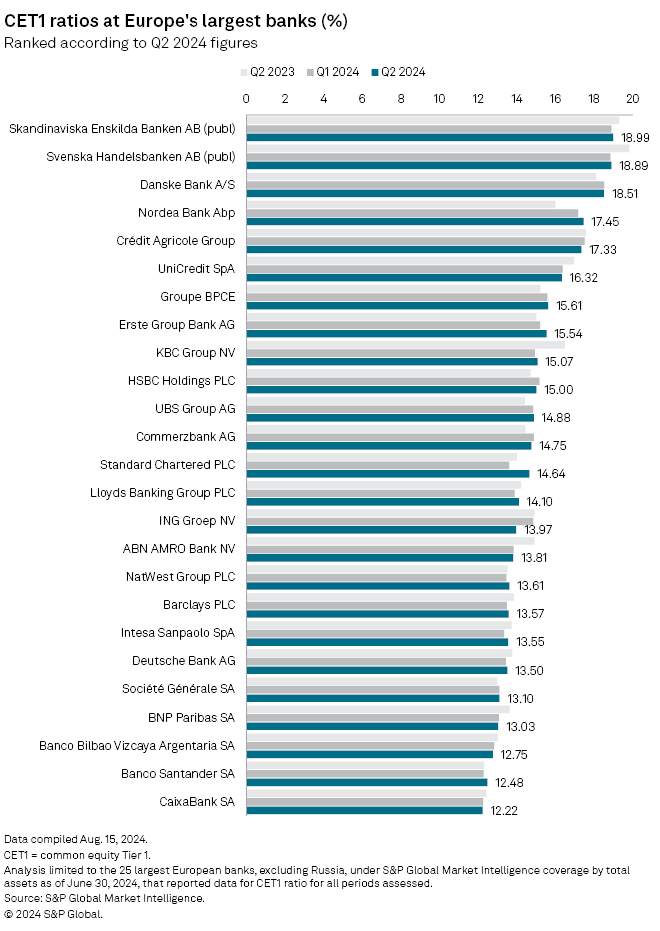

The PRA lowered capital requirements for banks' exposures to small- and medium-sized enterprises (SMEs) and infrastructure projects, as well as for their trade finance-related activities. The watchdog has also simplified how residential properties would be valued under the new framework to improve risk sensitivity in banks' mortgage valuations. Higher risk sensitivity could reduce the risk-weighted assets attached to the mortgage book and, with that, reduce the capital the bank would be required to hold against that book.

The adjusted rules will have a smaller impact on major UK banks, resulting in a less-than 1% aggregate increase in Tier 1 capital requirements as of the end of the phase-in period in January 2030, versus a 3.2% aggregate increase the PRA previously estimated.

The impact is also smaller compared to other jurisdictions. Under the US Basel III endgame reproposal announced on Sept. 10, global systemically important banks (G-SIBs) would face a 9% increase in Tier 1 capital requirements at full Basel III implementation and other large banks would face a 3% to 4% increase. In the EU, the increase is estimated at 16% for G-SIBs and 10% for other large and internationally active banks, according to the European Banking Authority (EBA).

–

"Amid ongoing geopolitical developments, such as the Russian aggression against Ukraine, the war in the Middle East and elections in the European Union and the United States, there is potential for sudden shifts in the economic outlook and market expectations," the authorities said. The materialization of credit risk remains a concern in this environment, which underscores the need for financial institutions to maintain "adequate provisioning levels" and "prudent and up-to-date collateral valuation," they said.

➤ A long-awaited update on Basel III endgame provides a bit of capital clarity

The revamped set of capital rules in the Federal Reserve's planned Basel III endgame reproposal should be more palatable for the banking industry.

➤ US, UK Basel III revisions pose implementation challenges for big banks

Lenders now face less stringent capital requirements than initially proposed but various revisions to the rules and adoption timelines may pose challenges for banks operating across major jurisdictions.

➤

The European Central Bank raised concerns about how banks are valuing their commercial real estate loans, noting that many reported inaccurate figures due to misapplication of market value definitions.

➤

The Swiss National Bank is reducing the threshold factor for remunerating sight deposits of banks, effectively reducing the amount of money it pays to lenders for parking cash with it.

Regulatory action

– UK

– The Bank of England will soon release a consultation paper detailing the circumstances under which UK

– The European Central Bank (ECB) plans to review counterparty credit risks arising from EU

– The UK

– The UK

Fines & cautions

– The ECB has started issuing fines to EU

– In a soon-to-be published report, the ECB is set to reveal data showing that EU

– The UK

– Swiss

– Belgium

– Germany

– The UK

01 Oct, 2024

FinReg Europe: UK eases Basel rules; EU warns banks of systemic risks

➤

The PRA lowered capital requirements for banks' exposures to small- and medium-sized enterprises (SMEs) and infrastructure projects, as well as for their trade finance-related activities. The watchdog has also simplified how residential properties would be valued under the new framework to improve risk sensitivity in banks' mortgage valuations. Higher risk sensitivity could reduce the risk-weighted assets attached to the mortgage book and, with that, reduce the capital the bank would be required to hold against that book.

The adjusted rules will have a smaller impact on major UK banks, resulting in a less-than 1% aggregate increase in Tier 1 capital requirements as of the end of the phase-in period in January 2030, versus a 3.2% aggregate increase the PRA previously estimated.

The impact is also smaller compared to other jurisdictions. Under the US Basel III endgame reproposal announced on Sept. 10, global systemically important banks (G-SIBs) would face a 9% increase in Tier 1 capital requirements at full Basel III implementation and other large banks would face a 3% to 4% increase. In the EU, the increase is estimated at 16% for G-SIBs and 10% for other large and internationally active banks, according to the European Banking Authority (EBA).

➤

"Amid ongoing geopolitical developments, such as the Russian aggression against Ukraine, the war in the Middle East and elections in the European Union and the United States, there is potential for sudden shifts in the economic outlook and market expectations," the authorities said. The materialization of credit risk remains a concern in this environment, which underscores the need for financial institutions to maintain "adequate provisioning levels" and "prudent and up-to-date collateral valuation," they said.

➤ A long-awaited update on Basel III endgame provides a bit of capital clarity

The revamped set of capital rules in the Federal Reserve's planned Basel III endgame reproposal should be more palatable for the banking industry.

➤ US, UK Basel III revisions pose implementation challenges for big banks

Lenders now face less stringent capital requirements than initially proposed but various revisions to the rules and adoption timelines may pose challenges for banks operating across major jurisdictions.

➤ ECB warns of flaws in banks' commercial real estate valuations

The European Central Bank raised concerns about how banks are valuing their commercial real estate loans, noting that many reported inaccurate figures due to misapplication of market value definitions.

➤ Swiss central bank makes changes on remuneration of sight deposits

The Swiss National Bank is reducing the threshold factor for remunerating sight deposits of banks, effectively reducing the amount of money it pays to lenders for parking cash with it.

Regulatory action

– UK

– The Bank of England will soon release a consultation paper detailing the circumstances under which UK

– The European Central Bank (ECB) plans to review counterparty credit risks arising from EU

– The UK

– The UK

Fines & cautions

– The ECB has started issuing fines to EU

– In a soon-to-be published report, the ECB is set to reveal data showing that EU

– The UK

– Swiss

– Belgium

– Germany

– The UK