17 Feb, 2022

Heartland Financial eyes bigger M&A as it consolidates charters

By Lauren Seay

Heartland Financial USA Inc., which recently rebranded as HTLF, is set for a busy year as it eyes larger M&A deals and begins to consolidate its 11 banking charters.

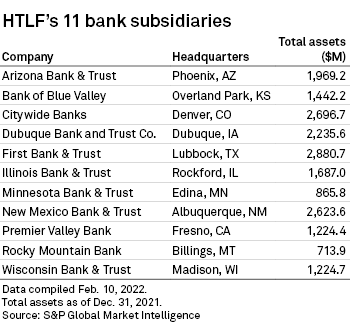

Dubuque, Iowa-based HTLF, the parent company to 11 bank subsidiaries in states across the U.S. with total assets ranging between $713.9 million and $2.88 billion, will soon combine its 11 charters into one Colorado-based charter. The company is open to M&A throughout its 12-state footprint, especially in states in the western and southwestern part of the country, President and CEO Bruce Lee said in an interview.

The serial acquirer has announced 10 whole-bank deals since 2015 — eight of which involved targets with less than $1 billion in assets — but as it approaches $20 billion in total assets, its minimum size target has increased to between $1 billion and $3 billion, Lee said.

HTLF is particularly interested in targets that have fee-income generating lines of business in areas such as payments, leasing, retirement planning services and wealth management, he said. The company is also open to nonbank M&A in those same lines of business.

Expense savings

The charter consolidation, which the company announced on its fourth-quarter 2021 earnings conference call, will improve efficiency, reduce expenses and drive scale, but the move does not mark a shift to the company's legacy strategy, Lee said. The 11 bank subsidiaries will still operate under their individual brands with local leadership and decision-making.

"We won't have to do things 11 times," he said. "The real key is the efficiency and the agility to be able to make a decision and implement it immediately, as opposed to implementing it 11 different times."

|

HTLF began studying the impact of consolidating the charters about six months ago, and the decision was partly driven by intensifying pressure to operate more efficiently in the current environment, Lee said.

"There is pressure on margins so the way that you continue to grow your earnings per share is you have to be more efficient. You have to do more with less," he said.

The consolidation will reduce annual expenses by about $20 million, once approved by regulators and completed in 2023. It will also improve the company's efficiency by freeing up time and resources as redundant tasks, such as completing 11 call reports each quarter and managing 11 separate investment portfolios, are eliminated, Lee said.

HTLF plans to reallocate the time and resources it is saving to improving customer experience, from speeding up the time it takes to open a deposit account to closing loans, he said. Customers will be able to make transactions at branches across all the 11 banks once they are under one charter.

"It's all about the customer experience. That's where we want to reallocate those resources, whether it's personnel or whether it's technology, that's what our focus is," Lee said. "How do we go faster, how do we improve the customer experience and what are the products that the customers now and in the future will want to use?"

Analysts a

Equity analysts are bullish on HTLF's future, with most recommending the stock for investors with "overweight" or "buy" ratings.

The company is poised for efficiency gains ahead as the upcoming charter consolidation, ongoing branch optimization and past technology investments work in concert to improve expenses, D.A. Davidson analyst Jeff Rulis wrote in a Feb. 1 note. HTLF consolidated roughly 8% of its branches in 2021 and it announced plans to close another 10% of its footprint in 2022 on its fourth-quarter 2021 earnings call.

Besides driving efficiency, consolidating the 11 charters into one will simplify regulatory and financial reporting for the company, according to Piper Sandler analyst Andrew Liesch.

Keefe Bruyette & Woods analyst Damon DelMonte also touted a positive outlook for HTLF, but said the company trades at an "unwarranted" and "notable" discount to Midwest and community bank peers. The company's shares were trading around 1.48x price to tangible book value as of Feb. 17.

Stephens analyst Terry McEvoy recommended in a Feb. 1 note that investors "take advantage of any price weakness over the near term."