12 Jan, 2022

Panjiva 2022 Outlook; Ningbo's COVID-19 lockdown could hit GoPlus, Dollarama

By Eric Oak

The Supply Chain Edge provides a curated weekly overview of Panjiva's research and insights covering global trade policy, the logistics sector and industrial supply chains and draws from global shipping and freight data.

Panjiva 2022 Outlook: At the tipping point

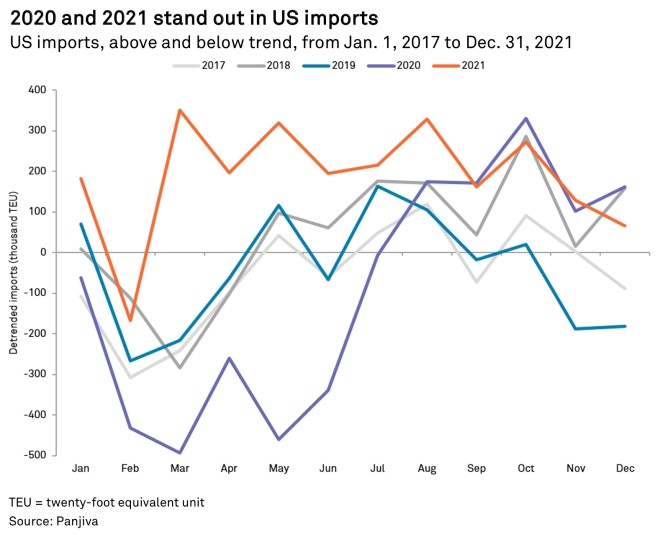

2022 will almost definitely be an eventful year for trade, regardless of how it pans out. One of the first indications of direction of travel may be the Lunar New Year holiday in Asia, traditionally when factories (and thus exports) slow down. In 2022, this may give carriers, ports and other logistics participants time to clear out some of the congestion that has been plaguing supply chains ever since the start of the pandemic. If import levels are similar to early 2019, rather than 2021, it may signal that the worst of the congestion is over.

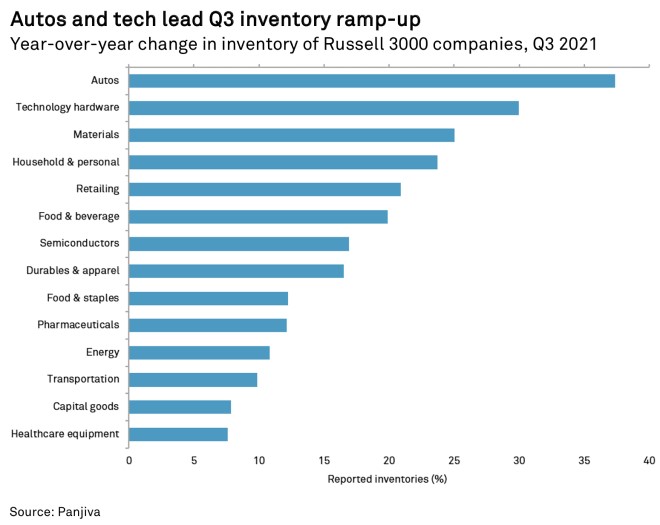

The base case scenario is that the logistics environment is similar to 2021. Built-up congestion, paired with rising inflation, could create a vicious cycle in which companies are incentivized to try to secure supplies at all cost — overordering and paying more. In time, these costs will most probably be passed on to consumers, causing additional wage pressure, and so on. Continued COVID-19 outbreaks, especially those caused by the omicron variant of the coronavirus, will likely hinder efforts by companies and ports to remain operating at elevated levels, as seen in the recent restrictions at the port of Ningbo, Zhejiang Province, China. If the same stories keep repeating, companies are likely to continue to ramp up inventories as well, as many have already done. Of the Russell 3000 companies, automotive firms have led their goods-focused fellows in this regard, having increased inventory 37.4% year over year in the third quarter.

A worse case for shippers is that additional events increase logistics congestion, or even shut down supply chains entirely. A prime candidate for such an event is the historically fraught negotiation of labor contracts at the West Coast ports of Los Angeles and Long Beach, Calif., scheduled this year. A slowdown or strike at the ports, which handled 32.0% of U.S. seaborne imports by volume in 2021, would be devastating to logistics networks, forcing companies to attempt shipping through already-overburdened secondary ports or to try to wait out the disruption. Either way, it could well boost congestion back to unworkable levels.

Meanwhile, trade rhetoric between the United States and China has been intensifying, with actions such as the former's banning of imports from Xinjiang or the latter's application to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership having the potential to escalate into larger grievances between the two countries. China accounted for 40.3% of U.S. imports in 2021, and a resumption of the trade war could put supply chains in a bind.

There are some events that could bode well for supply chains in 2022, including continued efforts by ports to clear congestion using financial incentives. The Port of Los Angeles implemented one such fee in late 2021, which generated enough response that it delayed the actual assignment of charges. Increased digitization of logistics networks could also add additional capacity to systems through increased efficiencies such as the reduction of downtime. If a large nearshoring trend utilizing U.S. trade partners in Mexico and Canada fully materializes, it could also help to alleviate seaborne congestion (although putting more pressure on trucking). Any improvement in metrics such as reliability and transit time would likely be bittersweet for carriers, however, which have enjoyed high profits over the past year. Those of Matson Inc., for example, increased 282.7% year over year, an almost definitely unsustainable growth rate if rates return to 2019 levels.

Read full article here.

Ningbo's heightened COVID-19 restrictions could hit GoPlus, Dollarama

China has increased restrictions around the port of Ningbo, Zhejiang Province, as a response to outbreaks of COVID-19 in the surrounding city. Carrier A.P. Møller - Mærsk A/S also issued an advisory outlining that three of the five terminals faced restrictions on entry and exit, but that loading and unloading operations were continuing as normal. This could impact companies that ship through the port, which has increased its share of U.S. seaborne imports relative to other major Chinese ports since the start of the pandemic. In the third quarter of 2021, its volumes to the U.S. were 40.0% above the equivalent quarter in 2019. Growth in October and November combined was 2.6% year over year, meaning Ningbo handled 7.6% of U.S. seaborne imports in the first 11 months of 2021. The volumes of the ports of Shanghai and Yantian (which handled 10.4% and 10.7% of U.S. seaborne imports, respectively, in the same 11-month period) fell 0.1% and 3.9% year over year, respectively, in October and November combined.

Panjiva data shows which North American companies received goods from the affected area. Imports from a 50-kilometer circle centered on the Beilun District in Ningbo that are associated with retailers Goplus Corp. and Dollarama Inc. and auto parts importer Advanced Innovative Manufacturing Inc. totaled 2,226, 6,037 and 4,609 twenty-foot equivalent units, respectively, in the first 11 months of 2021. The imports of GoPlus and Dollarama from the region declined 53.7% and 6.6% year over year, respectively, in October and November combined. If the firms were already shifting sourcing they may be less impacted by the restrictions. The data shows the opposite for Advanced Innovative Manufacturing, the imports of which increased 50.3% year over year in the same period. The new restrictions may become headwinds on that growth.

Read full article here.

Food availability on the menu for 2022

The resiliency of food supply chains is likely to be in focus in 2022, with companies such as Conagra Brands Inc. warning that the omicron variant of the coronavirus will impact operations. Conagra listed demand increases, supply chains and inflation as other factors combining to impact production. The company also noted higher inventory write-offs, part of the elevated costs that come from increased "just-in-case" inventories. The prices of commoditized foods have remained high as well, likely contributing to inflation, after extreme weather events in 2021 caused shortages. An expected La Niña weather pattern, which changes the annual rainfall distribution, is also expected to impact food production in the upcoming year, likely keeping producers wary of any future disruptions.

(The Wall Street Journal; Financial Times)

Consumer durable stocks face low charge, high prices

Consumer durables will not escape supply chain pressures, either. Booming demand for electric cars, coupled with automakers' increased anxiety about supplies, have led to companies rushing to secure goods. Sources in China were also hampered by restrictions in power usage, and prices are expected to remain high. Electric vehicles may see additional inflation in 2022, against the backdrop of an already tight car market. Consumers are also being impacted at home, with supplies of building materials falling short for homebuilders. Everything from windows to paint seems to be at risk, even though prices of raw materials such as lumber have fallen from their highs of last year. Additional costs will likely be passed on to homebuyers, increasing prices in an area that already has seen prices rise from demand alone.

(Nikkei Asia; The Wall Street Journal)

Port of Los Angeles announces dwell fees for empty containers

The Port of Los Angeles in planning to implement a fee for empty containers that remain at terminals for nine days. The fee will increase each day the container remains and is targeted directly at the mountains of empty boxes that are clogging up the port. The new fee is set to launch Jan. 30 but may never actually be implemented. A previous fee, for containers delayed in transit, was postponed by the port after its announcement led to a 53% decrease in volumes. "Just like the import dwell fee, the objective with this empty container program is not to collect fees but to free up valuable space on our docks, clearing the way for more ships and improving fluidity," Executive Director Gene Seroka said in a statement.

Eric Oak is a researcher at Panjiva, a business line of S&P Global Market Intelligence, a division of S&P Global Inc. This content does not constitute investment advice, and the views and opinions expressed in this piece are those of the author and do not necessarily represent the views of S&P Global Market Intelligence.

The Supply Chain Edge has an editorial deadline of Wednesdays at 8:00 a.m. ET. Some external links may require a subscription. Links are current at the time of publication. S&P Global Market Intelligence and S&P Capital IQ Pro are not responsible if those links are unavailable later.