9 Mar, 2021

M&T once again expanding its branch network through M&A

By Zach Fox and Ali Shayan Sikander

M&T Bank Corp.'s latest multibillion deal would see it expand into some slower-growth markets, but analysts think the regional bank has the experience to successfully capitalize on its acquisition of People's United Financial Inc.

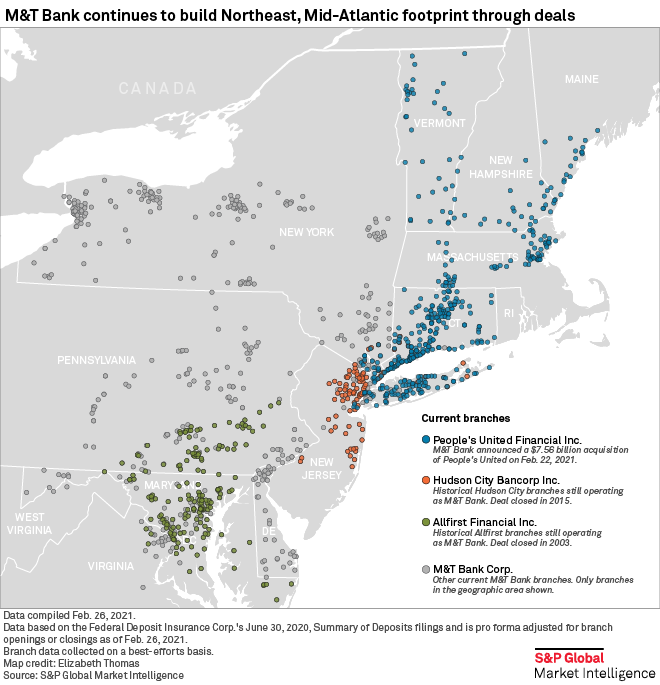

Chairman and CEO René Jones said the $7.56 billion deal shared "many similar characteristics" with M&T Bank's 2003 acquisition of Baltimore-based Allfirst Financial Inc., a $2.98 billion deal that expanded the bank's retail presence in the Baltimore and Washington, D.C., metro areas. This time, M&T is expanding to the northeast with the People's deal and entering another top metro in Boston, where People's is the No. 8 bank by deposit market share.

"It was important for them to get into Boston," Frank Schiraldi, managing director of equity research for Piper Sandler & Co., said in an interview. "I'm not sure it would have made as much sense without that toehold in Boston."

In addition to the Allfirst deal that opened the D.C. market, M&T in 2015 closed a $5.32 billion deal for Paramus, N.J.-based Hudson City Bancorp Inc. that expanded the company's presence in New Jersey.

While the company has not done another deal since the Hudson City saga — which was announced in 2012 and took more than three years to close due to Bank Secrecy Act issues — analysts said the company's history of expanding into new markets through multibillion-dollar deals will serve it well as it integrates the People's United deal.

Gerard Cassidy, a managing director and analyst for RBC Capital Markets, said most of the management has been with the bank for nearly their entire careers, meaning the experience from prior deals should come into play in the People's United acquisition.

Both Cassidy and Schiraldi said they do not expect any hold-ups similar to the Hudson City acquisition since the bank has addressed regulators' BSA/AML concerns.

Geographically, analysts and investors have been predicting more deals more to the south, especially the Southeast region, due to stronger demographic trends. People's United's footprint in New England has seen weaker demographic trends. Its home state of Connecticut saw a drop in population from 2010 through 2021 while Southeast states such as Florida, Georgia and North Carolina posted double-digit percentage-point growth, according to S&P Global Market Intelligence demographic data. But Cassidy said it made sense for M&T to stick to the Northeast and expand its footprint in adjacent states rather than look to leapfrog to the south.

"It's our view that intramarket deals — or deals that extend your market contiguously — are the better deals to do," Cassidy said in an interview. "There are only a select group of names that would make sense, and People's was certainly one of them, especially because it was sizable."

With M&T's size of $142.60 billion in assets, excluding the pending People's deal, a whole-bank acquisition for a company with less than $5 billion in assets would not make sense given the amount of work and effort needed to successfully complete a deal, Cassidy said.

New England's weaker demographic trends came up during M&T's deal call. Wells Fargo Securities analyst Michael Mayo asked how the bank's leadership reconciled the trade-off between increasing branch density in its existing footprint versus reaching for more growth to the south. Mayo noted that M&T has a history of success despite a long-existing focus on slower growth markets given its Buffalo, N.Y., headquarters. M&T's Jones said the bank's history has proven its ability to deliver above-market returns in markets with softer demographic trends.

"What tends to get missed is that by having dominant local share, it produces outsized ability to be close to your customer. It increases the value proposition between the bank and the customer, and it obviously results in excess rents or higher returns," Jones said.

The CEO also said slow-growth markets still tend to have significant financing needs and noted that the bank's Buffalo markets were "rock solid" through the 2008 financial crisis.

Cassidy said there can be some credit quality benefits from focusing on smaller markets. High-growth markets tend to attract significant competition, forcing banks to get aggressive on pricing or loan structure to win deals. By contrast, if a lender is the only bank in town, it can have pricing power.

"We have seen, quite often, the banks in the faster-growing markets run into more credit issues through the cycle because they let their guard down during the growth," Cassidy said. "You can't let your guard down when you're lending into Schenectady, N.Y., for a new hotel."